- Attractive discount on sponge worries scrap suppliers

- Finished steel prices decrease by INR 1,200/t m-o-m

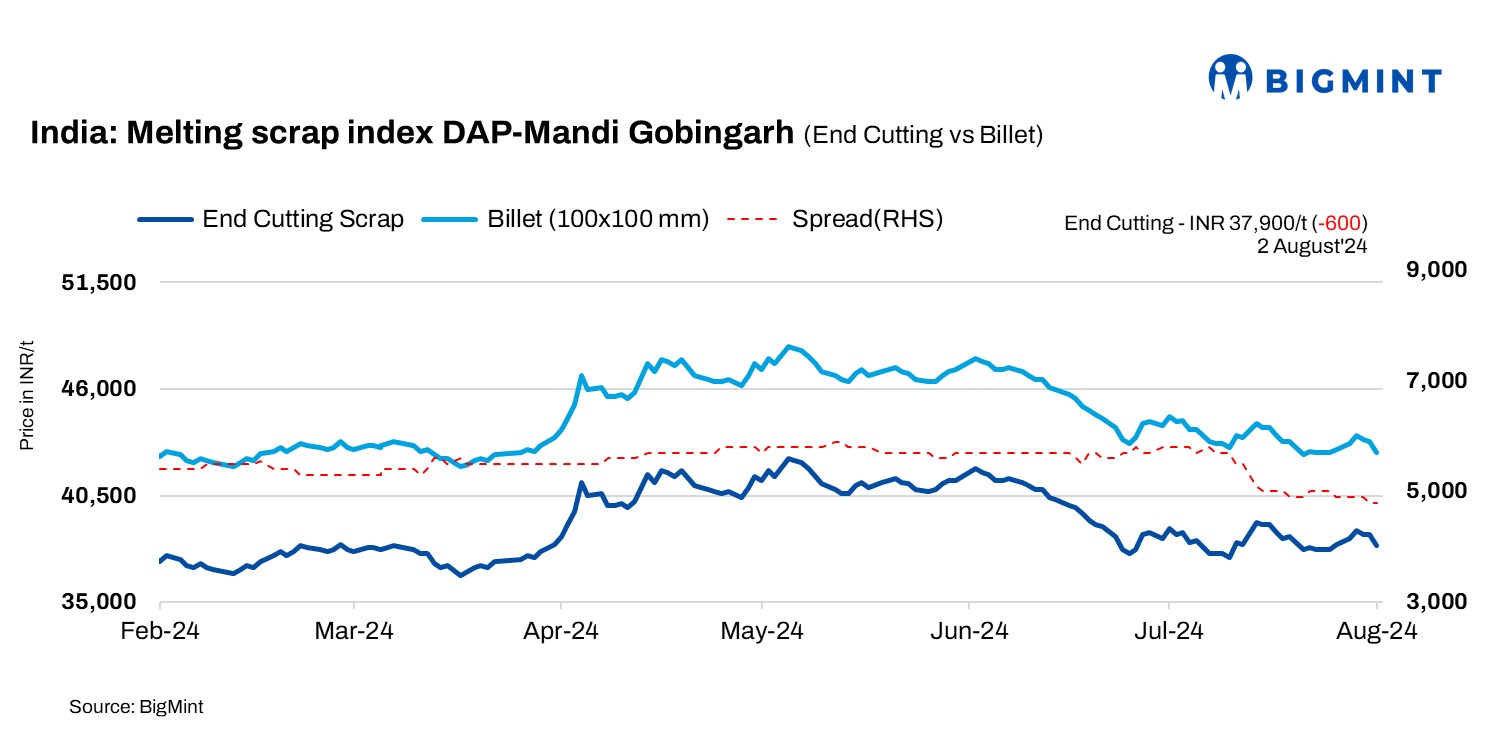

BigMint’s domestic end-cutting scrap index tracking the Mandi Gobindgarh market fell by INR 600/t to INR 37900/t DAP on 2 August, 2024.

Scrap suppliers are currently staring at an uncertain market because of the continuous decline in semi-finished and finished steel prices, a scenario that is making it challenging for mills to operate smoothly. Mills have increased their sponge iron consumption in the steel-making, while production cuts are pressuring scrap suppliers to accept deals that are of average volume. Furthermore, mills are reluctant to buy scrap at higher prices because of the attractive discount offers on sponge iron, forcing scrap suppliers to lower their prices.

Raw materials overview

Sponge iron (CDRI) prices declined by INR 200/t to INR 30,300/t today. In Ludhiana, pig iron (steel grade) prices remained unchanged d-o-d at INR 40,500/t DAP.

Steel market trends

In the Mandi region, steel ingot prices decreased significantly by INR 600/t to INR 43,650/t today during the price reporting and normalisation phase. Meanwhile, prices in other key markets fell by INR 250/t to INR 600/t. The Mandi Gobindgarh, Muzaffarnagar, and Mumbai markets saw a decrease of INR 600/t in semi-finished prices d-o-d, reflecting the subdued steel demand.

Rebar (Fe500) prices moved down by INR 200/t to INR 47,800/t exw in Mandi d-o-d and by INR 1,200/t m-o-m, driven by lacklustre demand in the finished steel market.

Overview of other markets

The Chennai market in southern India has seen stable prices in billets, rebar, and HMS 80:20, which were assessed at INR 43,000/t, INR 47,500/t, and INR 31,800/t, respectively. Market sources indicate that demand for semi-finished and finished steel is limited, while the supply of domestic scrap remains at a moderate level. Major mills are currently running at only 50-70% production capacity.

Price highlights

End-cutting-billets spread: In Mandi, the end-cutting scrap and billet spread was at INR 4,800-5,000/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were at around $390-$395/t, which equates to approximately INR 35,281/t (including freight), while local scrap, HMS (80:20), prices in Mumbai remained constant INR 33,000/t today. In India, indicative prices of shredded scrap from Europe stood at $410-$420/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The current conversion spread (margin) from pellet-based DRI (P-DRI) to steel billets in Raipur stood at INR 13,850/t.

To see BigMint’s melting scrap assessment, pricing methodology and specification documents, Click here

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – support@bigmint.co

Leave a Reply