- Sponge iron gains traction amid absence of imported scrap

- Logistics headwinds, scrap shortage tighten sentiment in Mandi

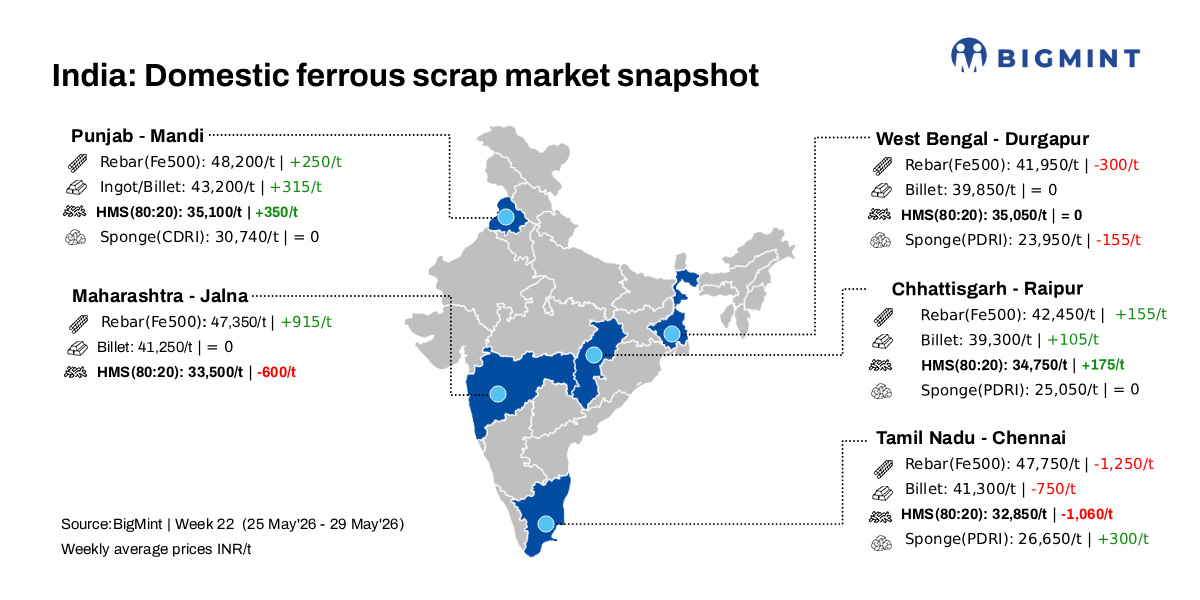

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, rose by INR 200/tonne (t) d-o-d to INR 38,400/t DAP on 29 May. On a weekly basis, prices surged by INR 350-400/t, supported by tightening scrap availability and improved demand across semi-finished and finished steel segments.

Mandi’s steel market is facing a persistent scrap shortfall as mills increasingly turn to sponge iron. Imported scrap remains largely absent due to poor price viability and ongoing geopolitical tensions. Logistics bottlenecks and labour shortages are adding strain: higher diesel prices have pushed up freight costs across the region, directly increasing raw‑to‑finished steel conversion expenses and squeezing margins. Additionally, extreme heat waves have reduced daily working hours by about three to four hours, further slowing operations across the market

A patra manufacturer informed BigMint: “In Mandi, demand at HR strip (patra) mills improved this week, while TMT makers are seeing good end‑user demand and expect pre-monsoon bookings to strengthen next month. Patra prices increased by INR 2,100/t w-o-w.”

Raw-material, steel market trends

Sponge iron prices in Mandi rose by INR 300/t d-o-d to INR 30,900/t DAP, and remained firm w-o-w. Pig iron prices in Ludhiana increased by INR 100/t to INR 43,000/t DAP, and were up INR 700/t w-o-w amid active buying and a slight regional shortage.

In the steel segment, ingot prices in Mandi gained INR 200/t d-o-d to INR 43,500/t, up INR 315/t w-o-w. Rebar ex‑works prices inched up INR 100/t to INR 48,500/t, an improvement of INR 265/t on the week.

Overview of Mumbai market

Rebar (Fe 500) prices on the Mumbai IF route declined by INR 400/t d-o-d to around INR 46,400/t ex-works. Sellers reduced their offer prices amid persistently weak buying activity over the past few sessions and subdued market sentiment. Trading activity remained slow during the day, with enquiries reported at low to moderate levels and procurement largely restricted to immediate requirements. Buyers continued to place bids at lower levels, maintaining a cautious wait-and-watch approach on expectations of further price corrections in the near term.

Mill inventory levels continued to rise on subdued demand conditions and limited buying interest in the market, with current inventory levels estimated at around 10-12 days. No major bulk bookings were reported during the day.

On the raw material side, HMS (80:20) scrap was assessed at INR 34,800/t DAP, with the scrap–billet conversion spread hovering around INR 7,650/t.

Upcoming scrap auctions

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 4,900-5,300/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $372/t, approximately INR 37,600/t (inclusive of freight). Today, HMS (80:20) prices in Mumbai remained stable at INR 34,800/t DAP. Indicative prices of shredded from Europe stood at $398/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 14,200/t.

To see BigMint’s melting scrap assessment, pricing methodology and specification documents, click here

To provide feedback on this index or if you would like to contribute by becoming a data partner, please contact – support@bigmint.co

Leave a Reply