- Firm MCX trends support India’s P1020 aluminium market

- Asian aluminium premiums remain stable amid muted trading

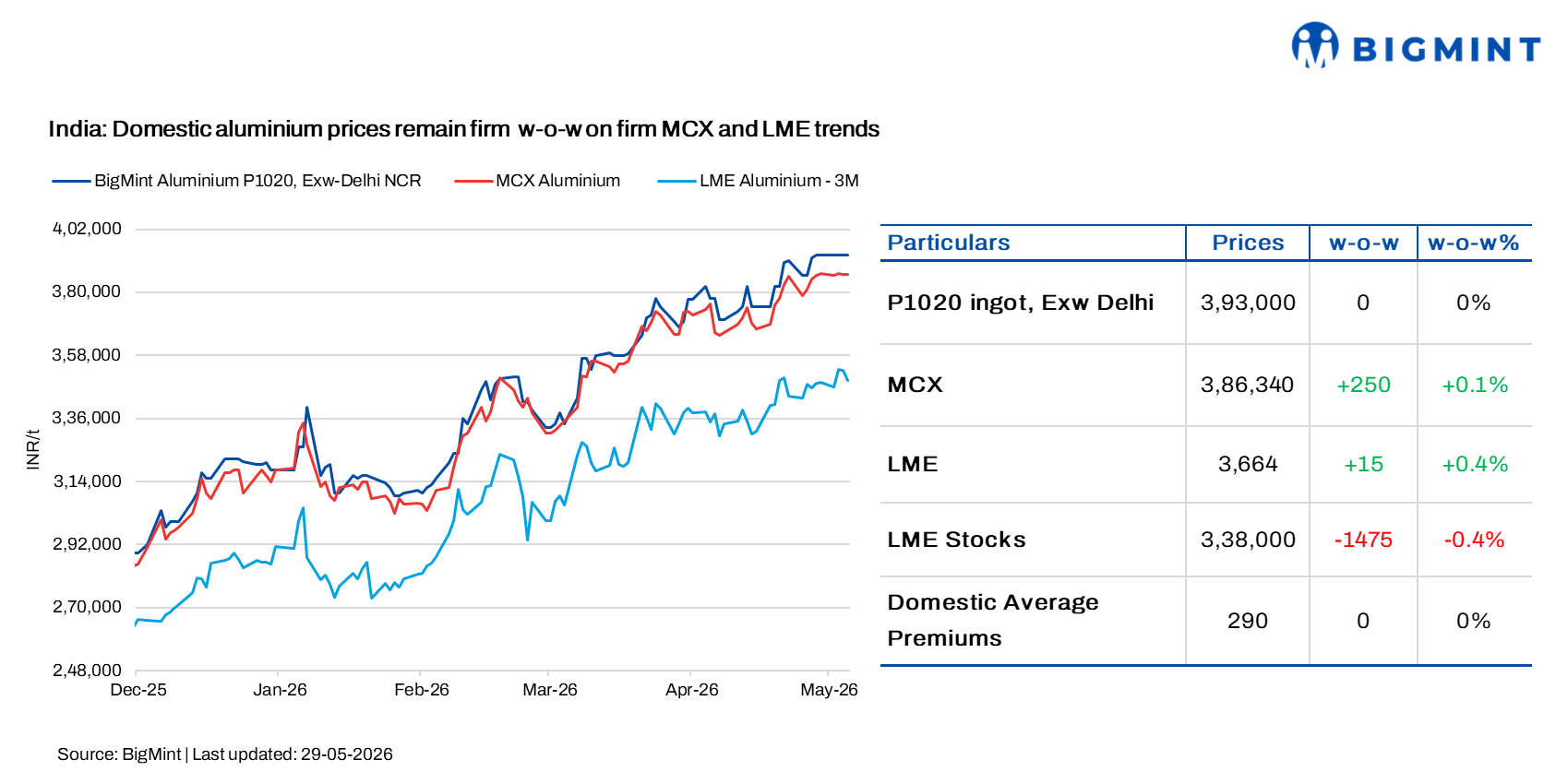

Domestic aluminium prices in India remained firm w-o-w as of 28 May’26, supported by firm trends on the Multi Commodity Exchange (MCX) and firmer sentiment on the London Metal Exchange (LME).

According to market assessments, P1020 ingot prices in Delhi NCR remained steady w-o-w at INR 393,000/t on 21 May. Meanwhile, Ex-Mumbai Aluminium Ingot P1020 prices increased by INR 5,000/t w-o-w to INR 396,000/t on 28 May from INR 391,000/t on 21 May.

How did Indian and global exchanges perform?

Domestic aluminium futures on the MCX remained largely stable w-o-w, increasing marginally by INR 250/t, or 0.1%, to INR 386,340/t on 28 May from INR 386,090/t on 21 May.

In comparison, three-month aluminium prices on the LME increased by $15/t, or 0.4%, to $3,664/t on 27 May’ from $3,649/t on 21 May. Meanwhile, LME aluminium stocks declined by 225 t to 339,250 t from 339,475 t during the same period.

LME aluminium prices moved higher after the holiday break, supported by tight near-term supply conditions, falling exchange inventories, and stronger global benchmark trends. Meanwhile, stable stock levels indicated relatively unchanged physical availability in the market.

Market updates

A major primary producer reported that domestic P1020 aluminium premiums remained firm at $290-300/t due to the sharp recovery in global benchmark prices and continued tightness in near-term supply conditions. Market participants indicated that buying activity remained relatively cautious at elevated price levels; however, stronger LME prices and declining exchange inventories continued supporting domestic offers. While material availability remained largely stable, higher replacement costs increasingly influenced market pricing dynamics.

NALCO’s primary aluminium ingot (P1020, 99.7%) prices increased by INR 6,100/t, or around 1.5%, to INR 411,000/t on 27 May from INR 404,900/t on 20 May, following the company’s latest price revision, reflecting firm domestic producer pricing amid firmer global aluminium market trends.

Meanwhile, BALCO recorded a 0.4% w-o-w increase, with average prices rising to INR 422,900/t from INR 421,083/t, while Hindalco prices increased by 1.2% to INR 423,083/t from INR 418,250/t during the same period.

Asian aluminium spot premiums remain stable

Asian aluminium spot premiums remained largely stable amid unchanged market fundamentals and subdued spot trading activity, as market participants awaited clearer pricing direction from ongoing Q3 MJP negotiations. Tradable spot levels in Korea were heard at $300-320/t FCA, equivalent to nearly $290-300/t CIF Korea, while expectations for Q3 MJP settlements were indicated around the $400/t CIF Japan range. The first Q3 MJP offer was reported at $480/t CIF Japan, which, if accepted, would mark the highest quarterly settlement level recorded for Japan.

Meanwhile, tight availability of good Western aluminium units in South Korea continued supporting regional premiums despite sufficient supply availability from Chinese and Russian-origin material. Market participants also noted that the wide LME backwardation could continue weighing on spot premiums and widening the gap between spot and quarterly contract levels. Low-carbon aluminium premiums also moved higher during the session amid continued demand for low-emission material across Asian markets.

Outlook

Domestic P1020 aluminium prices in India are expected to remain firm in the near term, supported by elevated global aluminium prices, stronger producer pricing sentiment, and continued tightness in near-term supply conditions. Declining LME inventories, firm MCX trends, and higher replacement costs are likely to keep domestic offers supported despite relatively cautious buying activity at higher price levels.

Leave a Reply