- Raw materials, steel tags decline by INR 450-620/t w-o-w

- Outlook in Mandi Gobindgarh remains bearish

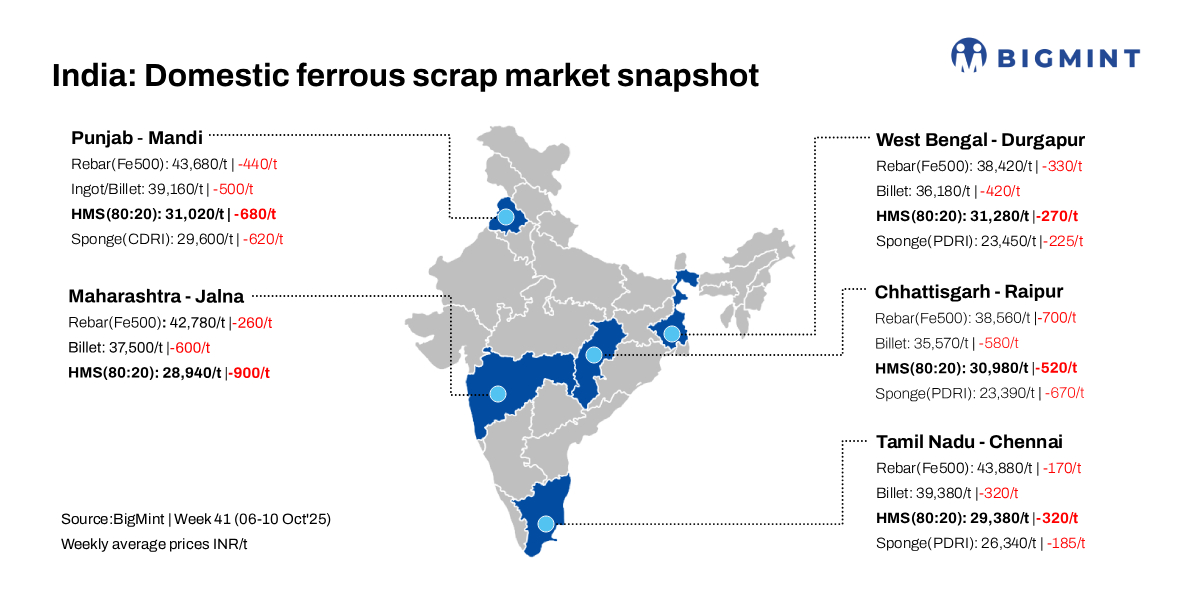

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, increased by INR 200/t to INR 34,000/t DAP on 10 October 2025. Scrap sellers raised their offers in today’s session following a slight uptick in the semi-finished steel market. However, both trading sessions remained quiet, with only short-term positive sentiment observed in the market.

Mandi Gobindgarh, a leading secondary steel hub, experienced a further price decline in the second week of October. Scrap prices dropped sharply by INR 550-700/t as mills slowed their purchases amidst tepid trade and persistent inventory pressure in finished steel. This weak buying activity has led to sale-driven liquidity challenges, prompting mills to consider production cuts, including shorter weekly operational runs.

Imported scrap buying also remained subdued due to a $10-$12/t mismatch between domestic and imported price level. As a result, most buyers are now opting for domestic scrap, further supported by improved local scrap arrivals following GST check relaxations.

According to a mill owner, “Steel mills are under severe pressure. With weak buying and falling finished steel prices across regions, the immediate outlook remains bearish, with expectations of further corrections ahead.”

Raw materials

In the raw material segment, sponge iron (CDRI) prices in Mandi Gobindgarh rose by INR 100/t day-on-day, reaching INR 29,600/t DAP. Despite this minor uptick, prices were down INR 620/t for the week, reflecting limited buying interest.

Meanwhile, steel-grade pig iron prices in Ludhiana held steady at INR 34,700/t DAP, but still registered a weekly decline of INR 300/t. The market remained cautious in both locations as buying remained generally subdued.

Steel market

Semi-finished steel (ingot) prices in Mandi Gobindgarh saw a slight increase of INR 100/t, settling at INR 39,200/t DAP. Other major production centers also recorded gains of INR 100-200/t during today’s trading.

Meanwhile, rebar (Fe500) prices in Mandi rose by INR 300/t to INR 43,800/t ex-works, despite input cost pressures. However, on a weekly basis, rebar prices fell by INR 450/t.

Auction highlights

Major auto-manufacturer’s CR busheling scrap auctions in late September 2025 saw a significant price decline, with prices dropping by INR 1,500-2,000/t. The market dynamics remain weak, causing buyers to stay cautious with their bid prices amid a dull secondary steel market.

Upcoming scrap auctions

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 4,900-5,200/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $325-326/t, approximately INR 31,100/t (inclusive of freight). HMS (80:20) prices in Mumbai decreased by INR 100/t to INR 30,000/t DAP today. Indicative prices of shredded from Europe stood at $355-356/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 12,100/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply