- Wide bid-offer disparities keep trades under pressure

- Domestic market more attractive due to higher sponge tags

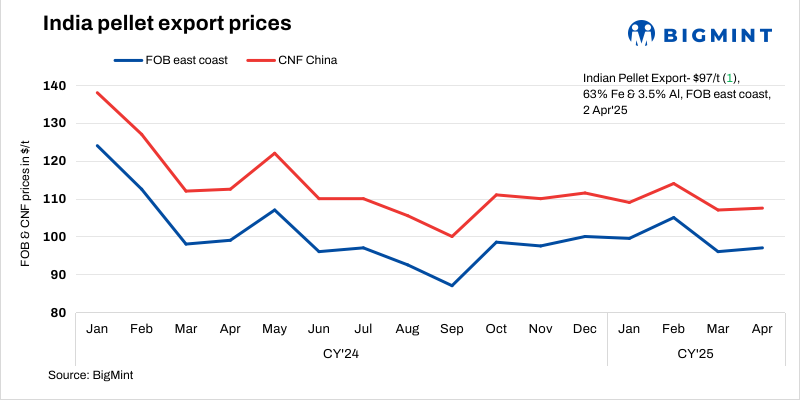

Indian pellet export prices increased marginally w-o-w, supported by a slight uptick in global fines tags. However, demand in the seaborne market remained weak, as buyers in China refrained from purchasing Indian pellets to optimise their production costs and import margins.

BigMint’s India pellet (Fe 63%, 3% Al) export index (FOB east coast) rose by $1/tonne (t) w-o-w to $97/t on 2 April 2025 against the previous assessment on 26 March. No trades were recorded this week from the east coast. However, a few unconfirmed deals of multiple supramax cargos were heard from the east coast.

A market participant noted, “Buyers are reluctant to procure Indian pellets at current prices, as they find domestic material more economical. Some Indian cargo is yet to be sold in the Chinese market, indicating that buyers may be cautious about procuring material at the asking prices.”

Despite Indian exporters’ higher price expectations, bids remained low, making it difficult for deals to materialise. Additionally, even port-based plants struggled to secure competitive bids, further weighing on the export market.

Meanwhile, the domestic pellet market has been performing well due to rising sponge iron prices. Increased demand led pellet manufacturers to focus on the domestic market, where they are securing better prices. A trader informed BigMint, “With the recent surge in sponge iron prices, pellet sales in the domestic market have been strong, making it a more viable option for manufacturers.”

Domestic prices exceeded export offers by INR 1,700/t ($20/t), remaining largely stable w-o-w. Pellet (Fe63%) prices in Odisha’s Barbil were recorded at INR 8,150/t ($95/t) exw, firm w-o-w. Meanwhile, ex-plant realisation in exports from Barbil stood at INR 6,450/t ($75/t) exw.

Exporters adopted a cautious approach, opting to withhold material from the Indian Ocean market. An Odisha based producer stated, “We are getting better inquiries from domestic buyers at firm prices against export. No deals have been concluded this week from the east coast amid poor market sentiments.”

Rationale

- No confirmed deals from India’s east coast were recorded in this publishing window for T1 trade. Thus, this category was not taken into consideration for today’s price calculations and accorded 0% weightage in the index calculation. Click here for the detailed methodology.

- Ten (10) indicative prices were received, and seven (7) were considered for calculation of the index and given 100% weightage.

Factors impacting pellet exports

- Chinese iron ore fines prices up w-o-w: The benchmark iron ore fines index inched up by $1/t w-o-w to $104/t CFR China on 1 April. Prices inched up amid expectations of a Q2 2025 demand recovery. However, concerns about the availability of low-priced material limited gains. Seaborne activity was muted, with a focus on higher-grade fines, while low- to mid-grade cargoes faced negative margins. Reportedly, some northern mills resumed using cheaper post-screened high-grade Brazilian fines instead of concentrate.

- DCE iron ore futures rise w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2025 contract increased w-o-w by RMB 11.5 ($1.5/t) to RMB 791.5/t ($109/t) on 2 April. On a d-o-d basis, futures remained stable.

Outlook

As per BigMint’s analysis, prices are expected to remain range-bound in the near term amid moderate market sentiment and cautious buying from Chinese mills.

Leave a Reply