- Mills under significant stress amid falling steel prices

- Steelmakers hopeful of demand recovery next month

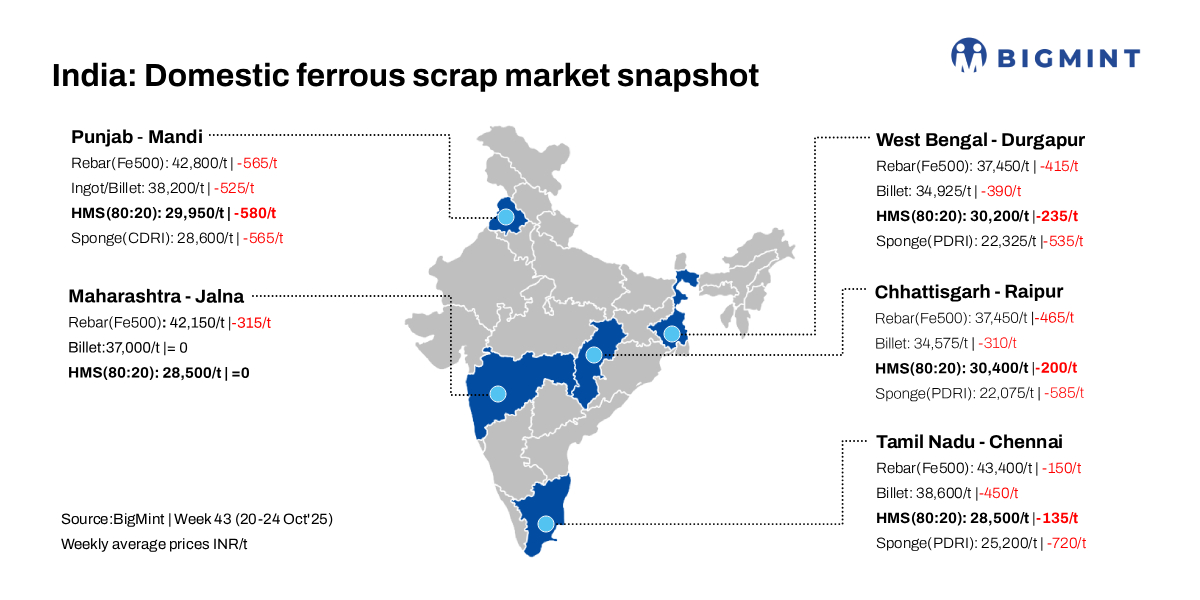

BigMint’s domestic end-cutting scrap index, tracking the Mandi Gobindgarh market, declined by INR 100/tonne (t) d-o-d to INR 32,900/t DAP on 24 October 2025. Scrap prices in Mandi Gobindgarh slid by approximately INR 500-600/t w-o-w, as festive-week disruptions slowed logistics and nearly halted trading activity. Additionally, very weak demand for finished steel led to subdued scrap procurement by mills, compounded by significant inventory pressure in both semi-finished and finished steel segments in Mandi.

Scrap supply in Mandi slowed compared to last week, as suppliers held back material amid renewed strict inspections at the Mandi borders.

A mill owner informed BigMint, “Steel prices are at a five-year low, and narrowing steelmaking conversion margins are adding to the pressure. As a result, secondary steel makers are cutting production, but overall, mills continue to incur losses. The steel market in Mandi remains under significant stress due to these factors, along with a slowdown in imported scrap arrivals in the region. Currently, there are no signs of positive movement in the steel market, but steelmakers remain hopeful that demand will improve next month.”

Alternative raw material prices

Sponge iron (CDRI) prices in Mandi dropped by INR 200/t d-o-d to INR 28,500/t (DAP). On a w-o-w basis, prices declined by around INR 570/t.

Similarly, steel-grade pig iron prices in Ludhiana fell by INR 100/t d-o-d but remained largely stable on a w-o-w basis.

Steel market

Semi-finished steel (ingot/billet) prices in Mandi Gobindgarh slipped by INR 100/t d-o-d to INR 38,100/t (DAP), weighed down by weak demand and narrowing conversion margins. Ingot prices across key production centres also softened further, by INR 100-400/t w-o-w. W-o-w, ingot prices in Mandi dropped by INR 530/t.

Rebar (Fe 500) prices in Mandi edged down by INR 200/t d-o-d and around INR 570/t w-o-w to INR 42,700/t ex-works.

Meanwhile, HR strip prices fell by INR 200/t d-o-d and approximately INR 720/t w-o-w to INR 39,300/t ex-works.

Overview of Mumbai market

Rebar (Fe 500) prices on the Mumbai IF route decreased by INR 300/t d-o-d to INR 41,500/t ex-works amid muted trading during the Diwali holidays. Limited demand, weak liquidity, and cash flow constraints kept buying restricted to immediate needs. On the raw material side, HMS (80:20) was assessed at INR 29,600/t DAP, with the scrap-billet conversion spread at around INR 7,300/t.

Upcoming scrap auctions

Price highlights

End-cutting to billet spread: In Mandi, the spread between end-cutting scrap and billets stood in the range of INR 4,900-5,200/t.

Domestic vs imported scrap: Imported melting scrap prices at Nhava Sheva Port were assessed at $324/t, approximately INR 30,645/t (inclusive of freight). HMS (80:20) prices in Mumbai fell by INR 300/t d-o-d to INR 29,600/t DAP today. Indicative prices of shredded from Europe stood at $354/t CFR Nhava Sheva.

Raipur sponge iron-billet spread: The conversion spread (margin) between pellet-based DRI (P-DRI) and steel billets in Raipur stood at INR 12,450/t.

To check BigMint’s melting scrap assessment, pricing methodology, and specification documents, click here.

Leave a Reply