- Fixtures closed at higher levels in Pacific, Atlantic basins

- Rising FFAs, bunker prices provide further suppport

Dry bulk iron ore freight markets recorded gains across major routes — India-China, Australia-China, South Africa-China, and Brazil-China — amid an improvement in overall market sentiment. Supportive Baltic index levels for larger vessel classes, notably Capesize, combined with a rebound in crude oil futures and a steady flow of fixtures, lent strength to freights. Increased chartering activity, particularly from miners and traders looking to secure tonnage ahead of upcoming maintenance schedules, added to the upward momentum. Market participants noted that while fundamentals remained relatively stable, firmer sentiment and active trading in both basins provided the primary lift to rates throughout the week.

The market saw a notable boost this week, driven by a surge in aggressive fixtures concluded at higher levels on both the Australia-China and Brazil-China routes. Strong chartering interest from key miners and traders, coupled with tightening vessel availability in the Pacific and Atlantic basins, helped push rates higher across major routes. Early-week activity, particularly for Capesize vessels, was marked by competitive bidding and prompt requirements, which lifted market averages.

However, while sentiment improved on the back of these firmer fixtures, some participants cautioned that the rally could face headwinds if cargo volumes ease in the coming sessions. Sustained momentum will likely depend on continued miner demand and steady chartering flows to maintain the current rate levels across basins.

Meanwhile, FFA rates and bunker prices also rose this week, supported by active fixtures and tighter tonnage, adding upward pressure on voyage costs while maintaining overall market optimism.

While underlying freight fundamentals remained firm this week, market sentiment was pressured by escalating geopolitical tensions after China imposed new port fees on US-linked vessels in retaliation for similar US measures. However, the market received some relief when the Chinese Ministry of Transport subsequently exempted Chinese-built and US-flagged ships from these fees, easing immediate concerns and helping restore a degree of confidence among industry participants.

The India-China Supramax freight market for iron ore remained subdued this week, influenced by several regional factors. While the Atlantic basin experienced increased activity, particularly from the Continent, where scrap demand lent support, the Indian Ocean region faced subdued trading conditions. The long holiday period in Asia contributed to a slowdown in trading, with the tonnage list weighing on rates across regional and Indian Ocean markets.

Despite these challenges, the market remains balanced, with steady tonnage-to-cargo ratios supporting rates. However, the outlook remains cautious, with industry participants monitoring the situation closely.

Route-wise updates

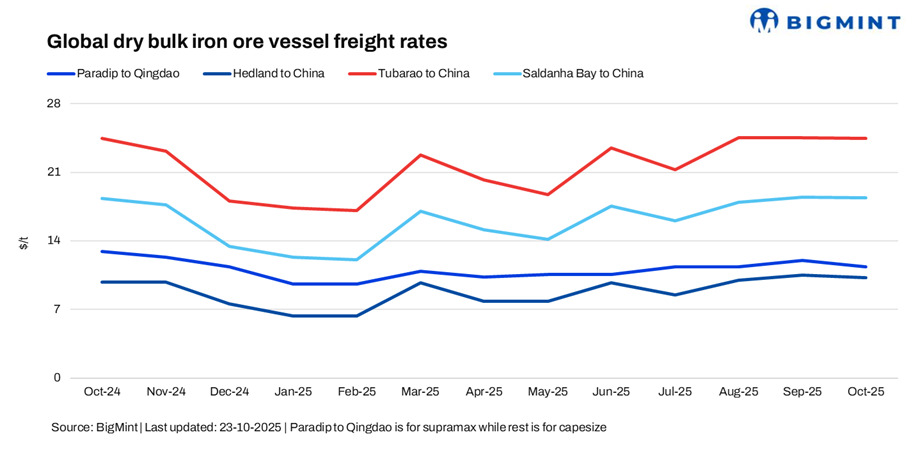

- India (Paradip)-China (Qingdao), Supramax: Freights for Supramax vessels from the Indian Ocean to China witnessed a w-o-w increase of $0.85/dry metric tonne (dmt) to $11.90/dmt.

- Australia (Port Hedland)-China (Qingdao), Capesize: Capesize freights for iron ore shipments from Western Australia to China rose by $0.42/dmt w-o-w to $10.70/dmt.

- Brazil (Tubarao)-China (Qingdao), Capesize: Capesize freights for Brazil to China shipments witnessed an increase of $0.58/dmt w-o-w, settling at $24.40/dmt.

- South Africa (Saldanha Bay)-China (Qingdao), Capesize: Capesize freights from Saldanha Bay to Qingdao edged higher by $0.25/dmt w-o-w, settling at $18.30/dmt.

Market highlights

- Baltic index edges higher on supportive sentiment: The Baltic Exchange’s main dry bulk sea freight index posted a modest w-o-w gain as market sentiment remained broadly supportive. As of 23 October 2025, the overall index rose by about 11 points to 2,057. The Capesize segment remained largely steady, adding just 1 point to reach 3,059. In contrast, the Supramax index continued to slide, by 44 points to 1,378, reflecting weaker demand and subdued fixtures across key Asian routes. Overall, the market stayed cautiously optimistic, supported mainly by sentiment-driven gains in larger vessel classes.

- DCE iron ore futures ease: Iron ore futures on the Dalian Commodity Exchange (DCE) for the January 2026 contract slipped by around RMB 5.5/t ($0.7/t) to RMB 771/t ($108.19/t) on 24 October 2025, compared with 15 October levels. The decline reflected subdued trading sentiment as market participants turned cautious amid signs of weak steel demand and steady portside inventories in China. Softer mill margins and limited restocking activity ahead of the year-end further weighed on prices, with seaborne supply remaining relatively stable.

- Brent crude futures strengthen on supply concerns: Brent crude oil futures climbed by about $3.43/barrel (bbl) w-o-w to $65.51/bbl on 24 October 2025 compared with 15 October. Prices were supported by signs of tighter output from key producers and ongoing geopolitical tensions that stoked fears of potential disruptions. Additionally, expectations of firmer demand from major consuming nations, coupled with a softer US dollar, lent further support to the rally. Overall, market sentiment remained cautiously bullish.

Outlook

The near-term outlook for the dry bulk iron ore freight market remains cautiously positive, supported by steady demand on key routes from Australia and Brazil to China. Active fixtures and tightening Capesize tonnage have helped sustain rates, although geopolitical tensions and regional disruptions, such as port fee issues, could create short-term volatility. Overall, market participants expect balanced fundamentals to keep freight levels relatively stable in the coming weeks.

Leave a Reply