- Steel prices face pressure, weigh on coking coal tags

- Australian coking coal offers decline by $5/t w-o-w

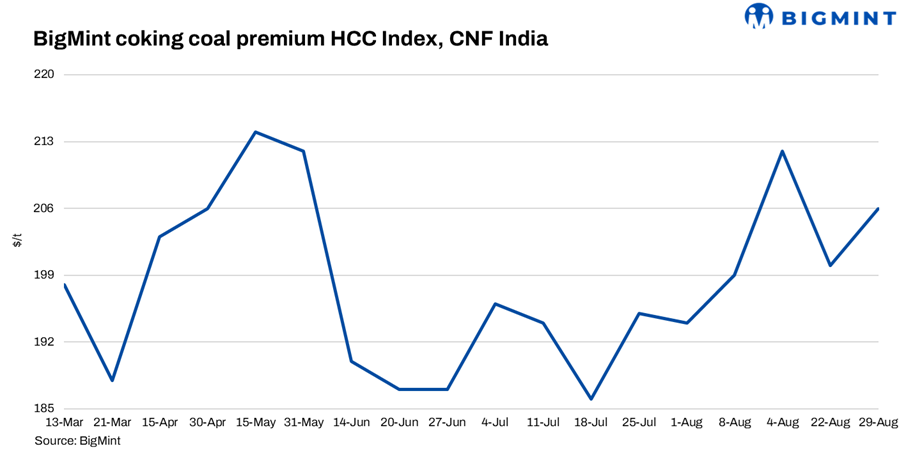

BigMint’s premium hard coking coal (PHCC) index was assessed at $206/tonne (t) CNF Paradip, India, on 29 August 2025, up by $6/t against the previous assessment on 22 August. Australian coking coal offers were down by about $5/t w-o-w.

Trad remained limited amid a wide bid-offer disparity. Market chatter suggests offers were at around $215-218/t CFR India, while $200-205/t CFR appeared to be a more workable range. Yesterday, an Australian miner reportedly sold 75,000 t of GYC (5-14 October laycan) at $189/t FOB Australia, though Indian buyers viewed the deal as being unrepresentative of prevailing prices, with tradable levels estimated closer to $185-186/t FOB.

Sentiment remained weak, with global markets under pressure, stated an Indian steel mill source.

Rationale

BigMint’s coking coal index is derived using data points, i.e., trades, offers, bids, and indicative prices.

No deal was recorded during the publishing window. Hence, it was considered for index computation and given a weightage of 0%.

Thirteen (13) firm offers, bids, and indicative prices were heard. Out of these, twelve (12) were considered for price calculation and given 100% weightage.

BigMint has consolidated its Prime Hard Coking Coal (PHCC) CFR India Index to include material of all origins, including US, Canada, Mozambique, Australia – normalised for quality and freight. With India steadily reducing its reliance on Australian PHCC and increasing imports from alternative sources, this update ensures the index accurately reflects evolving market dynamics and trade flows.

Factors impacting imported coking coal prices –

1. Indian met coke prices hold steady w-o-w amid tight supply: The Indian metallurgical coke (met coke) market was stable during the week ending 28 August 2025, underpinned by limited domestic supply and delayed import arrivals. BF-grade (25-90 mm) coke was assessed at INR 29,000/t ex-Jajpur in eastern India, while prices in the western region stood at INR 30,000/t ex-works Gandhidham.

2. China’s market split by regional policies: China’s met coke market displayed resilience, though demand trends varied by region. In Hebei and nearby provinces, strict environmental curbs and transport restrictions ahead of the 3 September parade reduced output and deliveries, forcing mills to cut production amid thinning inventories.

3. Indian steel prices remain under pressure: Trade-level BF rebar prices decreased by INR 600/t ($7/t) w-o-w to INR 47,300/t ($538/t) exy-Mumbai, as per BigMint’s assessment on 29 August 2025. Prices are exclusive of GST at 18%.

In the projects segment, prices dropped w-o-w to INR 46,000-47,000/t ($523-535/t) FOR Mumbai. Market activity was muted, as buyers stayed cautious during the monsoon season and the festive week. Construction momentum was further dampened by logistical challenges, leading to project delays and subdued procurement.

Leave a Reply