- Mills largely covered for Aug loading shipments

- Declining steel prices pressure coking coal bid

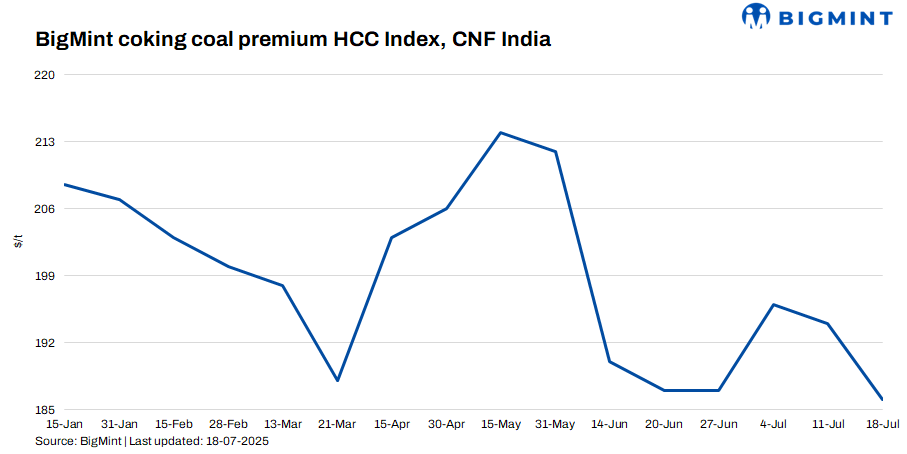

BigMint’s premium hard coking coal (PHCC) index was assessed at $186/tonne (t) CNF Paradip, India, on 18 July 2025, down by $8/t against the previous assessment on 11 July.

“Indian mills are largely covered for August loading shipments. Hence, just a couple of Panamax cargo bookings may be seen for the rest of July. Additionally, a weaker finished steel market in India and sufficient offers for coking coal from Australia resulted in lower bids,” said a trader.

An eastern India-based mill booked 40,000 t of PHCC from Australia at around $188/t CFR India for August loading. Another deal by a West Bengal-based mill was heard concluded from Australia at $183-184/t CFR India this week.

Canadian coking coal offers were on the lower side, at $175-180/t CNF India. However, no deals for the same were heard this week, said sources.

Rationale

BigMint’s coking coal index is derived using data points, i.e., trades, offers, bids, and indicative prices. One deal was recorded during the publishing window. Hence, this category was considered for index computation and given a weightage of 50%.

Ten (10) firm offers, bids, and indicative prices were heard. Out of these, nine (9) were considered for price calculation and given 50% weightage.

BigMint has consolidated its Prime Hard Coking Coal (PHCC) CFR India Index to include material of all origins, including US, Canada, Mozambique, Australia – normalised for quality and freight. With India steadily reducing its reliance on Australian PHCC and increasing imports from alternative sources, this update ensures the index accurately reflects evolving market dynamics and trade flows.

Factors impacting imported coking coal prices

1. Indian met coke prices edge up w-o-w: As of 16 July, BF-grade (25-90 mm) metallurgical coke (met coke) prices in India saw a modest upward movement. BigMint assessed prices at INR 29,000/t ex-Jajpur, reflecting a w-o-w increase of INR 500/t. In western India, Gandhidham witnessed a marginal rise of INR 100/t, with prices reaching INR 29,100/t exw. These movements indicate a slightly firming domestic market amid stable steel sector demand.

2. Chinese met coke market sees price hike: China’s metallurgical coke market witnessed its first price hike in nearly three weeks, driven by tightening supply, firm demand from steel mills, rising raw material costs, and speculative buying. Some steel mills were said to have accepted hikes of RMB 50-55/t earlier this week, though it was heard that coke producers had been planning to raise prices by a larger RMB 70-95/t. Inventories at coking plants have declined by nearly 25%, while environmental restrictions continued to cap output.

3. Indian steel prices fall further w-o-w: Trade-level prices of hot-rolled coils (HRCs) in India declined by up to INR 500/tonne (t) w-o-w to INR 49,200-51,400/t ($574-599/t) across markets. Moreover, cold-rolled coil (CRC) prices dropped by INR 800/t w-o-w to INR 55,000-59,500/t ($641-694/t).

BigMint’s benchmark assessment (bi-weekly) for HRCs (IS2062, Gr E250, 2.5-8 mm/CTL) dropped by INR 700/t ($8/t) w-o-w to INR 49,200/t ($574/t) on 15 July 2025 against INR 49,900/t ($582/t) a week ago.

Market sentiment remains subdued as demand continues to be lacklustre, with no visible signs of recovery. Inventory levels at the distributor end also remain elevated, reflecting slow offtake.

Leave a Reply