- ADC12 prices expected to remain range-bound

- GST cut triggers surge in PV demand

India’s secondary aluminium market saw a modest decline in September 2025, following a similar dip in August, after continuous gains in alloy ingot prices during the first half of the year. The drop in prices came as a result of a slight drop in domestic scrap prices amid improved availability.

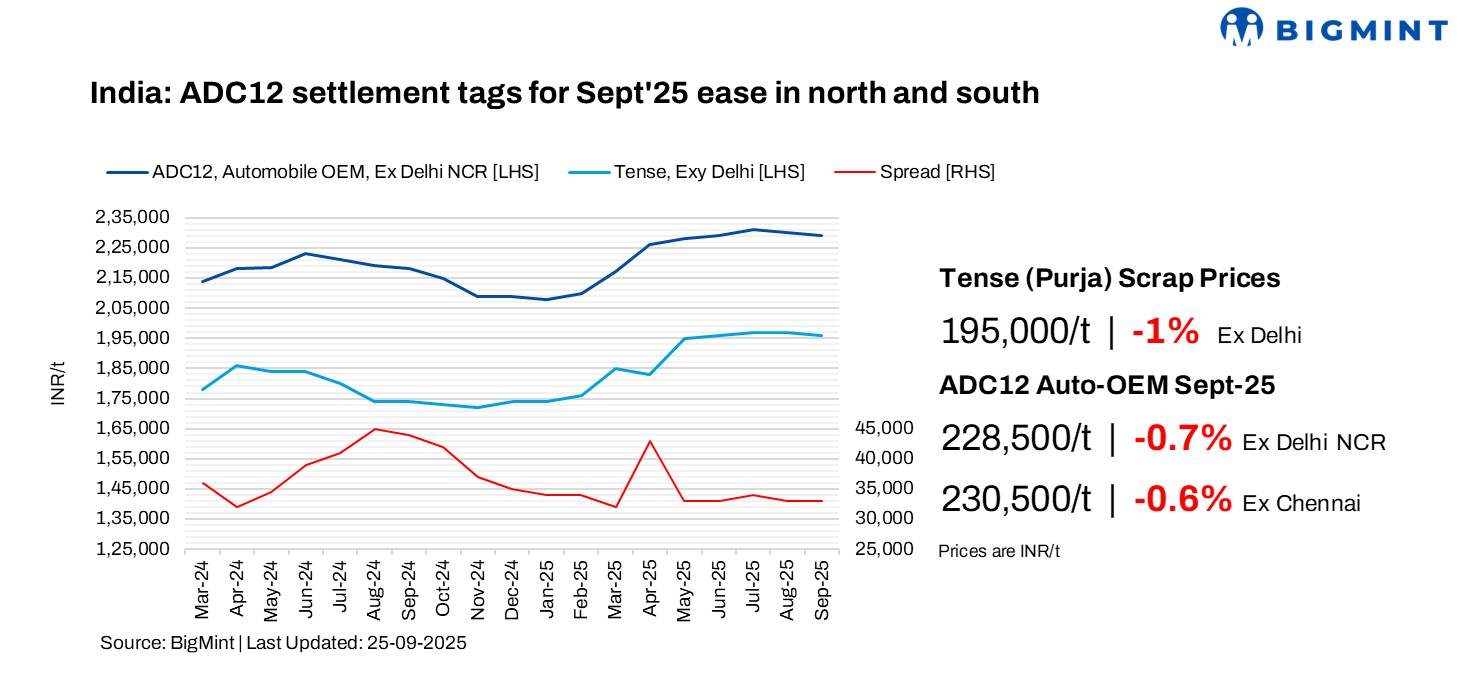

According to BigMint’s assessments, average automobile OEM ADC12 prices for September fell by to INR 1,500/tonne (t) m-o-m to INR 228,500/t in Delhi and INR 230,500/t in Chennai. The scrap-to-semi-finished spread held steady in the INR 34,000-35,000/t range, reflecting the steady cost of sourcing raw materials.

Additionally, a major Indian automaker has slightly reduced its ADC12 settlement price by INR 700/t m-o-m to INR 228,900/t for Oct’25. The marginal dip is attributed to easing raw material costs and anticipated improvement in ADC12 import availability.

Market dynamics in early Oct’25

Offers for ADC12 in both north and south India are seen hovering between INR 228,000-229,000/t in Delhi and INR 230,000-231,000/t in Chennai.

Bids in the north were heard at INR 226,000-227,000/t and in the south at INR 228,000-229,000/t.

Indicative ADC12 prices for 30-day payment terms in the west were heard between INR 227,000-228,000/t ex-Pune.

Raw material trends

In September, imported aluminium scrap prices witnessed an uptrend aligning with a 2.2% gain in LME aluminium, which averaged $2,650/t for the month.

A trader source mentioned, “Depreciating rupee, quality concerns in imports, and cautious buying patterns collectively contributed to the price fluctuations for the imported material. However, major scrap grades remained firm in terms of prices due to a gain in LME levels amid global supply concerns.”

Among key imported grades, US-origin Tense rose by a minor $6/t m-o-m to $1,986/t, while UK-origin Wheels increased by $8/t to $2,578/t.

On the domestic front, Tense scrap prices decreased by INR 1,000/t, with BigMint’s end-September assessment placing prices at INR 195,000/t in Delhi and INR 197,000/t in Chennai, down by INR 2,000/t, as additional supply entered the market with yards offloading stock ahead of the quarter-end.

Additionally, Chinese silicon 553 prices remained stable m-o-m, settling at $1,368/t CFR Mundra.

Tracking India’s scrap, ingot import flow in 8MCY’25

India’s overall aluminium scrap imports increased by 10% to 1.25 mnt in 8MCY’25 from 1.13 mnt in 8MCY’24. Major importers also scaled up procurement amid a shortage of aluminium scrap during the initial months of the year, particularly following the imposition of US tariffs.

Most grades, except for Talk, witnessed an increase in arrivals in 8MCY’25 despite intense price volatility.

While Taint Tabor was the most imported grade in 8MCY’25, the gap between it and Zorba was a slim 1,800 t. Zorba imports totalled around 276,000 t, up 9% from 253,000 t in 8MCY’24.

Among other grades, Extrusion (Tread) witnessed the highest percentage growth of 16% to 220,000 t. Meanwhile, Tense was also up 10% to 171,000 t.

ADC12 imports

India’s ADC12 alloy market continued to witness a sharp contraction in imports during the first eight months of 2025 (8MCY’25), with inbound volumes falling 61% year-on-year. Total ADC12 imports stood at 6,750 t, down significantly from 17,485 tin 8MCY’24.

Auto sector performance

India’s automobile sector showed mixed performance in 8MCY’25 compared to 8MCY’24. As per SIAM OEM data, passenger vehicle sales dipped 1.05% y-o-y to 2.83 million units, while two-wheeler sales remained flat at 12.64 million units. Three-wheeler sales rose 6.52% to 0.49 million units, but commercial (CV) sales declined 1.56% to 0.63 million units. Domestic sales were steady at 16.6 million units, while production climbed up by 5.25% y-o-y to 20.03 million units.

Meanwhile, FADA retail sales data reflected stronger growth. Passenger vehicles surged 5.02% y-o-y to 2.72 million units, two-wheelers inched up 1.19% to 11.9 million units, and three-wheelers gained 3.80% to 0.82 million units. CV sales rose 2.99% to 0.69 million units, and tractors jumped 5.08% to 0.62 million units, pushing total retail sales up 2.13% to 16.75 million units.

The government’s Next Gen GST reforms are already showing strong economic impact, with record-breaking auto sales this festive season. Experts highlight reduced vehicle prices (by 8-10%), faster refunds, and simplified tax structure as key drivers. Major automakers like Maruti, Mahindra, Hyundai, and Tata reported sharp sales spikes, reflecting improved consumer confidence and a stronger market outlook.

Outlook

ADC12 prices are expected to stay range-bound between INR 227,000-230,000/t in both north and south India. A major price drop is unlikely due to steady festive demand. Additionally, the recent GST cut on passenger vehicles, effective from 22 September has triggered a surge in auto sales. With improved buying sentiment in the auto sector, ADC12 prices are likely to remain stable in the near term.

Leave a Reply