- Sluggish economy threatens steel industry growth

- Weak demand, price wars push mills to trim output

- Demand dries up as construction projects stall

Morning Brief: It has been over one year since the July Revolution swept through Bangladesh, plunging the country into deep-set political and economic crises. The steel industry was caught in the crossfire, with real estate and infrastructure projects stalling, crippling steel demand. Mills’ capacity utilisation rates dropped precipitously, while a liquidity crunch hampered trading activity.

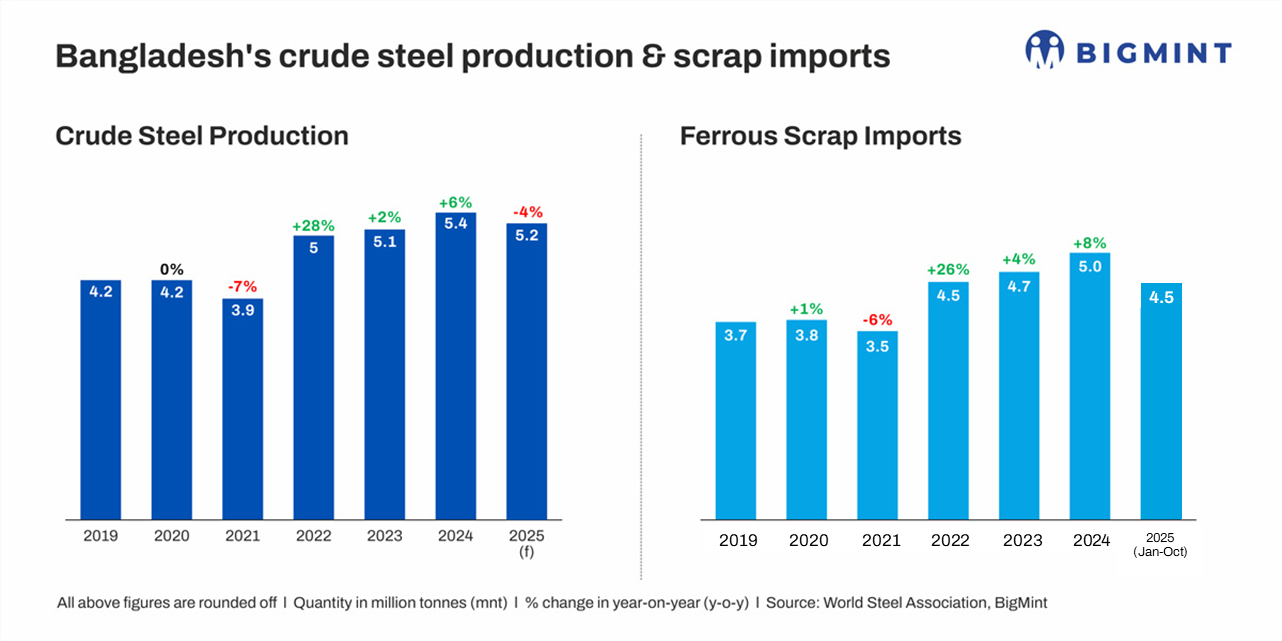

Yet, even though months have passed, Bangladesh remains mired in a prolonged economic slump, with BigMint’s projections pointing to the possibility of a 4% y-o-y drop in crude steel production to 5.1-5.2 million tonnes (mnt) in CY’25. So, what’s ailing the industry? By when would a sustained recovery come about? BigMint goes behind the scenes.

Economic growth to decelerate in FY’26

Once boasting robust GDP growth rates of 6-7%, Bangladesh is expected to see much slower expansion of 4.9% this fiscal year, as per latest forecasts from the International Monetary Fund (IMF). This marks a steep cut from the 5.4% predicted in July and 6.5% in April. The interim government, however, has set an initial target of 5.5%.

In FY’25, Bangladesh’s economy remained weak, logging its slowest growth since FY’20, as per the Bangladesh Bureau of Statistics (BBS). A mid-year recovery was unable to offset the slowdown seen in the first quarter of FY’25, when the nationwide protests occurred.

A subdued investment climate was one of the leading reasons for the weak demand environment last year. Others included elevated inflation rates, tightening of monetary policy, and the banking crisis stemming from an excessively high share of non-performing loans.

Construction sector growth also softened in FY’25, with the government reducing its infrastructure expenditure.

Economic slowdown impacts steel industry

The steel industry remains fragile, mirroring the macroeconomic slowdown. A loss of confidence among individual developers and the larger real estate sector since the July Revolution has weighed on steel demand, and the stagnation of public infrastructure works has exacerbated the negative impact on demand.

A steel mill source observed that following the outbreak of the Russia-Ukraine war, the previous government had curtailed infrastructure expenditure to keep foreign exchange reserves intact. This had also acted as a catalyst for the July Revolution.

Another noted, “During the July mass protests and afterwards, there was a sharp decline in construction material consumption immediately after the previous government fled the country. The y-o-y demand between 2023 and 2024 for the months of August, September, and October declined by almost 40%.”

He added that while market activity was more stable in the last three quarters of FY’25, consumption remained depressed in comparison to previous years, missing industry growth projections.

Notably, Bangladesh’s crude steel output rose 6% y-o-y to 5.4 mnt in CY’24, though a slight decline is anticipated in CY’25.

Political, administrative uncertainties hinder construction activity

Various political, administrative, and regulatory challenges have been impacting steel consumption. Due to political uncertainties, real estate projects have failed to take off. Additionally, a lack of clarity on pricing and profitability is making developers reluctant to invest resources.

In fact, a source highlighted that several foreign contractors fled the country during the time of the protests to ensure their safety. Public sector companies also paused construction work as leadership roles shifted or budgets were reassessed. Relevant design approval authorities faced lack of direction during the leadership transition, resulting in delays to building approval plans.

Moreover, the banking crisis made it difficult for sub-contractors to obtain necessary support. Notably, in the past year, the market has intermittently faced challenges in obtaining letters of credit (LCs) from banks. Meanwhile, infrastructure work has not progressed as rapidly as hoped for under the interim government, though foreign exchange reserves have improved.

Steelmakers struggle as headwinds emerge

Steel mills have been struggling with their own set of problems, with falling steel prices narrowing margins. In the past few months, steel mills have been operating at 30-40% of their capacities, due to a protracted monsoon, LC constraints, and weak finished product demand.

Recently, rebars were being traded at over three-year lows of BDT 73,700/tonne (t) ($603/t) exw in Dhaka, while Chattogram prices were at BDT 77,100/t exw ($631/t).

An industry source also highlighted that mills have had to contend with higher borrowing rates, while indications of a port tariff hike have caused uncertainty. A supply glut has also emerged, leading to unhealthy competition and price wars. Credit-based transactions have increased, leading to liquidity shortfalls for a market that has primarily been cash-based.

Additionally, of the 40 commercial banks supporting industrialisation in Bangladesh, many have been blacklisted by foreign suppliers and rating agencies. However, demand from individual households is said to be resilient.

In early 2024, BigMint had projected that steel consumption would rise to 8.5 mnt in CY’24 compared to 7.6 mnt in CY’23. Consumption ultimately totalled 7.5 mnt in CY’24, as per estimates from a source.

Bangladesh’s ferrous scrap imports rose 10% y-o-y to 4 mnt in 9MCY’25, supported by lower prices. Based on market analysis and previous bookings, imports are projected to increase by another 0.5 mnt in October, indicating a 3% y-o-y rise to 4.5 mnt in 10MCY’25.

Imported bulk scrap prices have approached five-year lows, while containerised scrap followed a similar trend, with UK-origin shredded assessed at $368/t and Europe-origin HMS 80:20 at $349/t, both CFR Chattogram. A sluggish ship-breaking market has likely contributed to stronger demand for imported scrap.

Outlook

Despite the current slump, optimism persists. The World Bank, while projecting a 4.8% economic growth in FY’26, said that the rate may rise to 6.3% in FY’27. This points to Bangladesh’s underlying economic resilience.

Currently, all eyes are on the general elections in February 2026. Several infrastructure projects are in the pipeline, and the steel industry is waiting for execution to start. Stable leadership is likely to restore investor confidence, too. Additionally, foreign direct investment will need to be targeted, along with fiscal relief for ailing industries. Reducing the import tariffs for raw materials will also benefit steelmakers.

In early 2024, BigMint projected Bangladesh’s steel capacity to rise by 13 mnt by FY’27. However, following the July Revolution and ongoing financial challenges, this growth is likely to be delayed by a year. Industry representatives expect an additional 3 mnt of capacity by 2026-2027, taking total capacity to around 15 mnt — far exceeding current market demand of about 7 mnt. Experts caution that without demand alignment, further investment may risk oversupply.

Leave a Reply