- LC opening, processing issues continue to disrupt trade flows

- Mills’ focus on destocking rebar and wire rod inventories

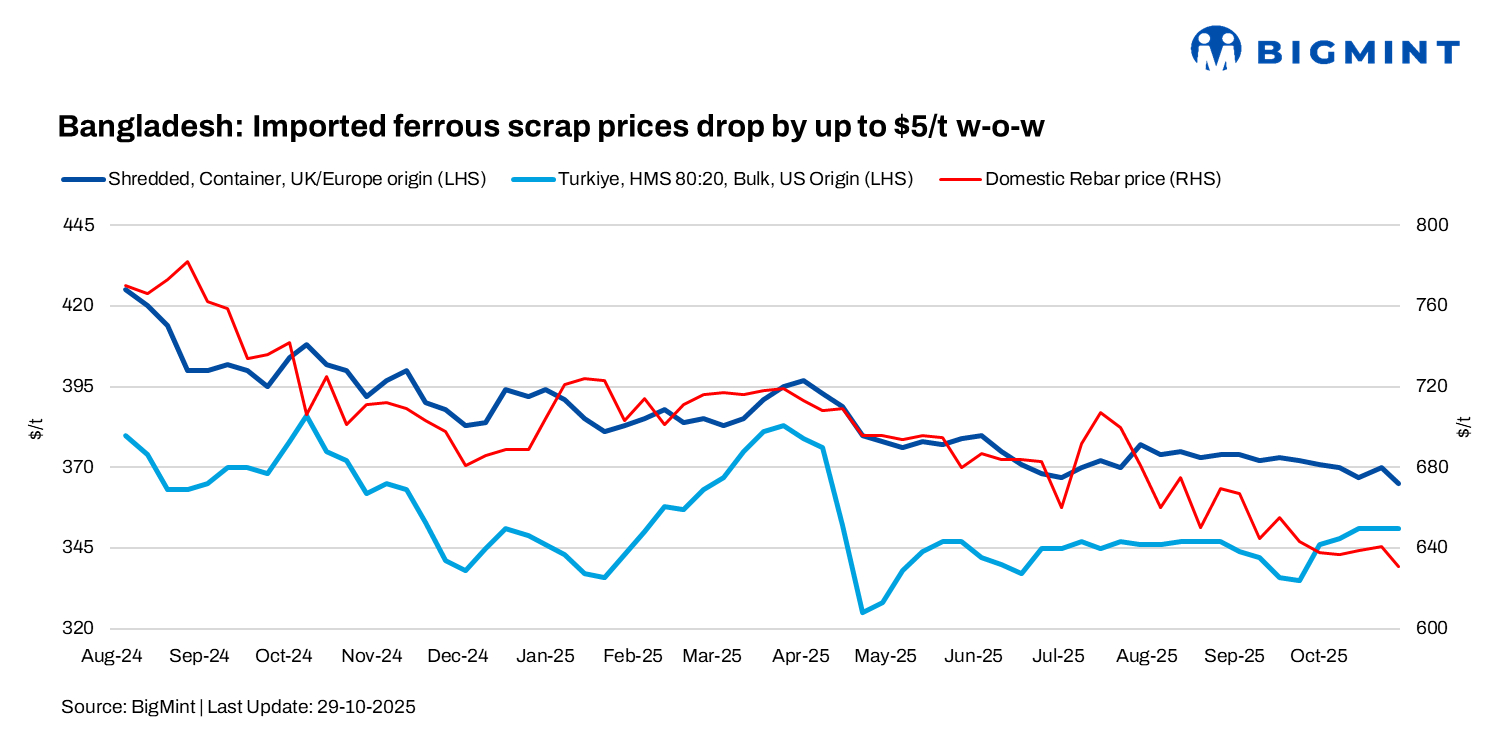

Bangladesh’s imported scrap market remained subdued as mills stayed cautious amid weak finished steel demand and ongoing liquidity constraints. Most producers continued operating at reduced output to manage costs, while high import prices kept scrap purchases limited.

Some Chattogram-based mills showed mild interest in Japanese scrap but focused more on clearing existing inventories of rebar and wire rods before making fresh bookings, as persistent LC opening and processing challenges continued to restrict trade flows and dampen overall market sentiment.

BigMint’s weekly assessments

- European-origin HMS (80:20) prices inched down by $3/t w-o-w to $346/t.

- European-origin containerised shredded inched down by $5/t w-o-w to $365/t.

- Japanese-origin H2 bulk prices stood at $348/t, increasing by $4/t w-o-w.

- US-sourced HMS (80:20) bulk prices inch up by $1/t w-o-w to $354/t

Australia- and New Zealand-origin shredded offers were heard at $365-370/t CFR Chattogram, though buying interest stayed below $360/t. As per a Dhaka-based trader, Australia shredded offers were heard at $362-365/t CFR amid limited buying interest.

Some HMS cargoes were available at $340/t for prompt shipment. From Japan, a Chattogram-based mill was last heard purchasing H2 scrap bulk at $345-350/t, while busheling offers from Japan stood at $370-375/t CFR.

Recent deals

- 1,000 t Brazil-origin HMS 90:10 sold at $330/t CFR Chattogram

- 1,000 t Hong Kong-origin PNS concluded at $373/t CFR Chattogram

- 1,000 t Brazil-origin HMS 2 (bundles) traded at $300/t CFR Chattogram

Domestic market

Domestic market activity remained muted as mills continued to operate at reduced capacity amid sluggish rebar demand and persistent LC issues. Local scrap traded at BDT 45,000-48,000/t ($368-393/t) exy Chattogram, while rebar stood at BDT 74,000-78,000/t ($605-638/t) and billet around BDT 63,000-64,000/t ($515-523/t).

Ship-recycling: Large-vessel deals dominate amid weak sentiment

Chattogram’s ship recycling market stayed volatile, with demand shifting to large vessels like LNG carriers and Capesize bulkers. Smaller LDT units saw limited interest as inflation, new export tariffs, and a weaker Taka dampened sentiment. Political uncertainty ahead of the 2026 elections also slowed activity, with only a few deals heard, including two LNG carriers and Waruna’s MONICA P sold at $380/LDT.

Outlook

Market sentiment is expected to stay fragile as persistent LC constraints continue to hinder trade activity. Mills are likely to maintain a cautious stance in the near term, prioritising destocking over fresh scrap purchases. A meaningful recovery will hinge on improved liquidity conditions and a gradual rebound in construction activity post-monsoon.

Leave a Reply