- Non-coking coal imports fall amid rise in coal production

- Pet coke, met coke imports surge by around 25% y-o-y

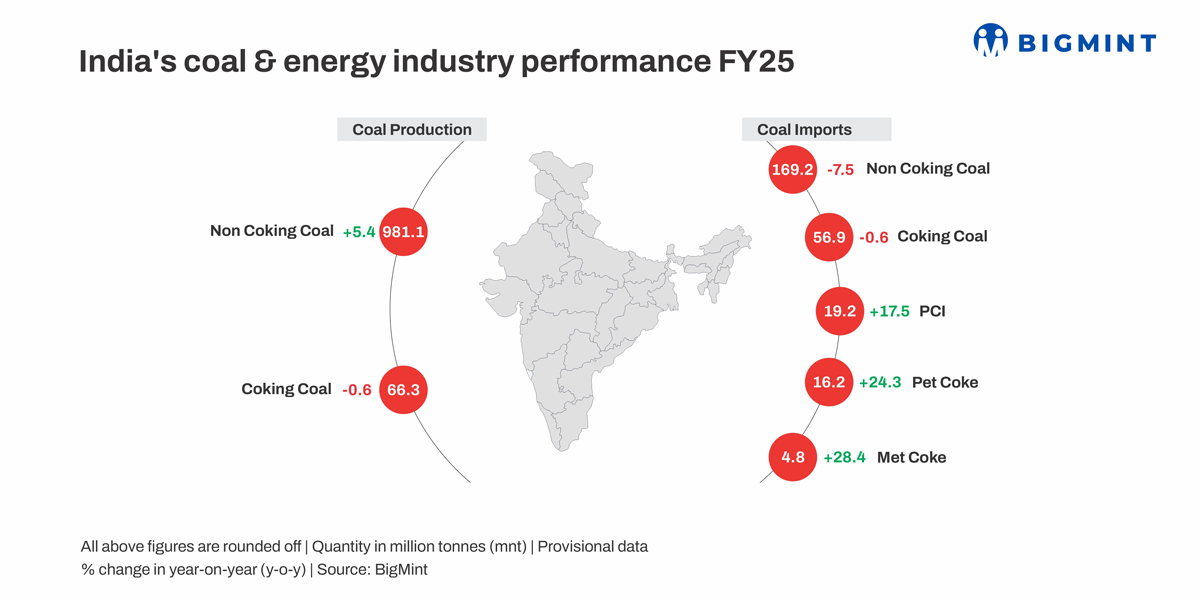

India’s coal and energy industry witnessed significant improvements in FY’25, though certain challenges emerged. Coal production reached a record peak, helping India reduce its import dependency in the power generation segment. However, met coke and pet coke imports surged, reflecting a gap in domestic supply.

Coal production hits all-time high, crosses 1 bnt mark

India’s coal production achieved a record peak in FY’25, increasing by 5% to 1,048 million tonnes (mnt) compared to 998 mnt in FY’24. This helped India increase its reliance on domestic coal, which resulted in a decline in imports. Non-coking coal output rose 5.5% to 981 mnt, led by Coal India Ltd. (CIL) and its subsidiaries, particularly MCL, which posted a 10% y-o-y increase in production. Policy changes such as expanded auction volumes and a lower earnest money deposit (EMD) boosted domestic uptake, leading to a 12% y-o-y drop in non-regulated sector imports.

Non-coking coal imports decline 8% as domestic production rises

India’s non-coking coal imports declined by 8% to 169 mnt in FY’25 from 183 mnt in FY’24, as higher domestic production and improved auction dynamics reduced dependence on imports.

Met coal imports edge up, shipments from Australia decline

India’s metallurgical coal (including PCI) imports rose by around 3% to 76 mnt in FY’25 from 73.6 mnt in FY’24. This included 56.9 mnt of coking coal and 19.2 mnt of PCI. The rise came despite reduced shipments from Australia and the US, as imports from Russia surged, indicating a shift in sourcing strategy.

Met coke arrivals jump 28% y-o-y; govt imposes import quotas

India’s metallurgical coke (met coke) imports rose sharply by 28% to 4.8 mnt in FY’25 from 3.8 mnt in FY’24. The increase was driven by strong demand from the steel sector, leading manufacturers to rely heavily on cost-effective imported met coke.

However, this surge in imports put pressure on domestic producers, who struggled to compete with cheaper overseas material.

In response, the Indian government initiated an anti-dumping investigation into low-ash met coke imports from six key suppliers – Australia, China, Colombia, Indonesia, Japan, and Russia – aiming to curb unfair pricing and protect the domestic industry.

Additionally, the government-imposed country-wise quantitative restrictions for two consecutive quarters in 2025 (January-March and April-June), capping imports at 713,583 tonnes per quarter to balance domestic and foreign supply while the probe is underway.

Pet coke imports surge amid cement sector demand, US supply glut

India’s pet coke imports climbed up by 24.6% y-o-y to 16.2 mnt in FY’25, driven by strong cement sector demand and tighter domestic supply. The US remained the top supplier with 8.2 mnt (+15.5%), while Saudi Arabia shipped 3.5 mnt (+29.6%) amid diverted US cargoes from China.

Ultratech led imports with 4.2 mnt, followed by Ambuja and Reliance Cement. Kandla and Visakhapatnam ports saw strong growth, while Mundra volumes declined.

Power generation in India up 5%

India’s power generation grew 5% to 1,848 billion units, yet the use of coal imports for blending in thermal plants fell nearly 30% following the lapse of the government’s blending mandate. In the industrial segment, crude steel and sponge iron output grew 4.7% and 5%, respectively, with strong demand for South African material continuing due to its high fixed carbon content, essential for coal-based sponge iron production.

Price trends

Imported South African non-coking coal RB3 (4800 NAR) remained stable y-o-y at $80/tonne (t) CNF Gangavaram. Portside RB3 (4800 NAR) prices at Gangavaram also held firm y-o-y at INR 7,720/t, amid balanced demand-supply dynamics.

Australian premium hard coking coal (PHCC) averaged $230/t CFR India in FY’25, up from $220/t in FY’24, driven by supply disruptions and firm demand. However, prices declined sharply in March 2025, with BigMint’s PHCC index at $188/t CNF Paradip on 31 March, down $10/t from mid-March, as global prices hit a four-year low of $166/t FOB before rebounding slightly.

Average US pet coke prices fell to $107-109/t CNF from $123-126/t due to oversupply, while Saudi-origin material remained costlier. Imports are expected to remain firm, though future volumes may hinge on price trends and global demand.

Outlook

The outlook for India’s coal and coke sector in FY’25 remains positive, driven by increased domestic coal production and reduced import dependence. Non-coking coal imports have decreased, while demand for metallurgical and pet coke continues to rise, particularly from the steel and cement sectors. However, factors such as price volatility, global supply shifts, and government intervention to protect domestic producers in the met coke market may influence future trends.

Leave a Reply