- 5% y-o-y production growth supported by infra, housing demand

- Cement consumption up 7% y-o-y despite elections, rains

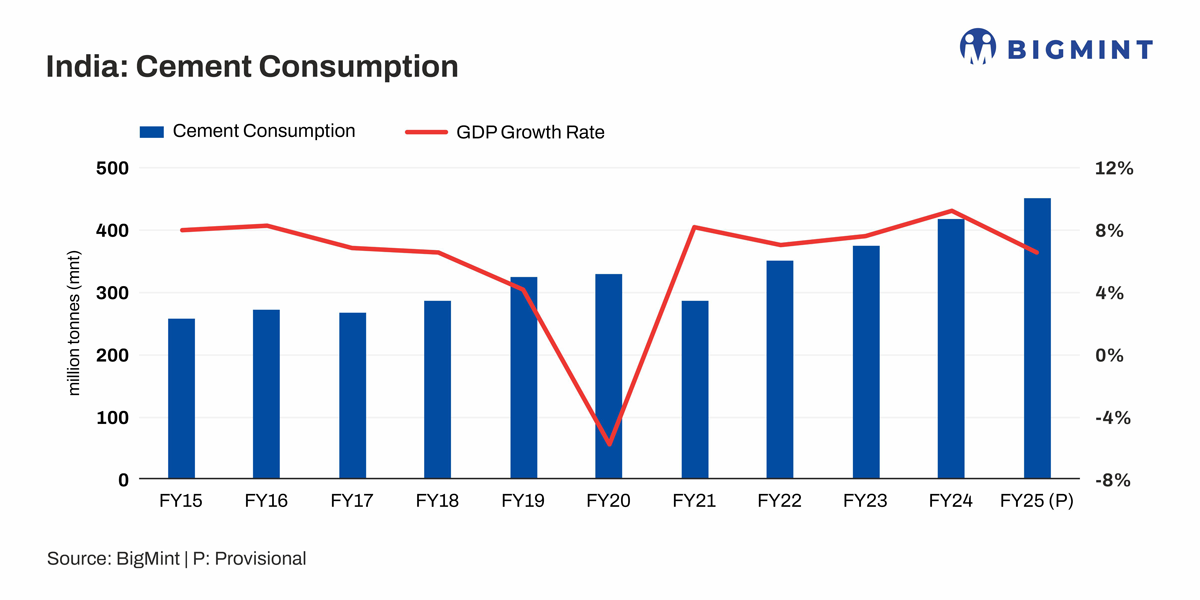

India’s cement production grew by around 5% y-o-y to around 457 million tonnes (mnt) in F’Y25, compared to 436 mnt in FY24. This was supported by sustained infrastructure and housing demand. However, India’s GDP growth rate moderated to 6.5% in FY25, down from 9.2% in the preceding year.

India’s cement consumption increased by around 7% y-o-y to 450 mnt in FY’25 as against 420 mnt in FY24. Consumption grew despite temporary slowdowns due to elections and unseasonal rains.

Cement margins remained under pressure in FY’25 due to pricing competition and input cost volatility. Industry EBITDA margins softened to around 16-17%, compared to higher levels in FY’24, though some recovery was seen in the latter half through cost rationalisation.

Capacity utilisation in the industry improved slightly to an average of 71-72% in FY’25, from around 70% in FY’24.

The industry added around 33-35 mnt of capacity during FY’25. Leading companies like UltraTech, Dalmia Bharat, and Birla Corp continued to invest in expansions, with the sector targeting 700 mtpa capacity by 2030.

Company-wise performance

1. UltraTech Cement delivered a robust performance in FY’25 and Q4FY’25, driven by strong volume growth, improved operational efficiency, and strategic capacity expansions. Consolidated sales volumes reached 135.83 mnt in FY25, up 14% y-o-y from 119 mnt in FY24.

In Q4FY’25, sales volumes increased 31% on the quarter to 41.02 mnt as compared with 31.2 mnt in Q3. Domestic grey cement sales rose 10% y-o-y in Q4, while capacity utilisation improved to 89%.

The company’s EBITDA per tonne stood at INR 1,270/t in FY’25, up INR 305/t or 15% y-o-y against FY’24.

Cost efficiencies were achieved with lower fuel (INR 864/t), power (INR 354/t), and logistics costs (INR 1,167/t) in Q4FY’25.

Capex for the year was at INR 9,428 crore, focused on green power and productivity, with an additional INR 1,500 crore planned over two years.

The company increased its cement capacity to 183.4 mtpa, targeting 210.5 mtpa by FY’27. With housing and infrastructure demand expected to stay strong, the company remains optimistic about sustained growth and margin improvement.

2. Ambuja Cements reported a strong operational performance in FY’25, with annual sales volumes reaching 65.2 mnt, up 10% from 59.2 mnt in FY24, and Q4 volumes at 18.7 mnt, a 13% y-o-y increase as compared with 16.6 mnt in Q4 of the previous year. Capacity utilisation remains strong, aided by efficiency programmes and logistics optimisation.

The company recorded its highest-ever quarterly EBITDA of INR 1,868 crore in Q4FY’25. EBITDA/t at INR 1,001/t, significantly improved from INR 537/t in the previous quarter. In FY’25, EBITDA/t dropped 8% on the year to INR 915/t.

The company’s capex programme is self-funded, with INR 10,125 crore in cash reserves, supporting its expansion from to 140 mtpa by FY’28.

Sales realisation improved, supported by a higher share of premium products and trade segment focus.

Key cost indicators such as logistics and fuel saw declines, with fuel rates dropping 12% y-o-y and logistics costs were down by 5%.

The company expects robust demand to be driven by housing, infrastructure, and smart cities, while continuing its journey of cost leadership and sustainability.

3. Shree Cement’s total cement sales volume increased 13% q-o-q to 9.84 mnt in Q4FY’25, driven by strong infrastructure and real estate demand. The company maintained a trade sales mix of 73% with capacity utilisation at 72%.

In Q4F’Y25 alone, EBITDA per tonnes rose to INR 1,406 from INR 1,088 in the previous quarter. The margin gains were supported by improved realisations and a notable drop in fuel costs to INR 1.48/kcal as against INR 1.82/kcal last year. However, lead distance increased slightly from 435 km to 446 km, affecting logistics costs marginally.

The company incurred a capex of around INR 3,000 crore in FY’25, commissioning grinding units at Etah (UP) and Baloda Bazar (Chhattisgarh), taking total capacity to 62.8 mtpa. With expansions at Jaitaran (Rajasthan) and Kodla (Karnataka) underway, capacity is expected to rise to 68.8 mtpa by FY’26.

4. JK Cement’s total cement volumes rose 6% on the year to around 20.2 mnt in FY’25 with growth led by the grey cement segment, while white cement volumes remained stable.

EBITDA per tonne declined y-o-y to around INR 1,002 in FY’25 due to higher input and branding costs, but rebounded to INR 1,265 in Q4FY’25 on better realisations and a strong trade mix of 71%.

The company incurred INR 1,800-2,000 crore in capex, primarily for a 6-mtpa expansion across Panna, Prayagraj, Hamirpur, and Bihar, slated for completion by December 2025-January 2026. Clinker utilisation stood at around 82% for the year.

On the cost front, lower fuel costs and freight optimisation supported margins, though logistics costs rose slightly due to longer lead distances from entry into newer markets like Bihar. For FY’26, the company has guided for 20 mtpa grey cement sales, backed by rural housing and infrastructure demand, while maintaining its focus on premium products and cost control.

5. Dalmia Bharat reported a modest performance in FY’25, with total cement sales volume edging up 2% y-o-y to 29.4 mnt from 28.8 mnt in FY’24. Despite higher volumes, EBITDA/t declined to INR 820 in FY’25 from INR 917 in FY’24, reflecting pricing pressure and input cost inflation. However, cost efficiencies and improved sales mix helped support margins in H2FY’25.

The company incurred a capex of INR 2,664 crore in FY’25, supporting ongoing capacity expansions. Installed cement capacity rose to 49.5 mtpa from 44.6 mtpa in FY’24, with key additions in Lanka, Kadapa, Ariyalur, and Kalyanpur. Clinker capacity stood at 23.5 mtpa. Clinker utilisation and efficiency remained healthy across regions.

On the cost front, fuel and power costs rose to INR 1,296/t, but logistics optimisation, including improved direct dispatches (57%) and deployment of LNG vehicle helped contain freight expenses. Raw material cost also increased, while the company continued to benefit from high blended cement share (85%) and renewable energy investments.

The company is optimistic, supported by government-led capex, infrastructure growth, and rural housing demand. It has set an ambitious target of 75 mtpa capacity by FY’28.

Note- The figures of sales volumes, EBITDA per tonnes have been rounded off* in the article.

Leave a Reply