- Tight global output boosts India’s pricing power

- Consumption trend rising amid falling acreage

A tight global production scenario is creating a strong opportunity for India in the coriander market in 2026. Stakeholders across the value chain — from farmers at the grassroots to investors in boardrooms — are increasingly betting on the fragrant spice. The crop is sown during December-January and harvested between March and April, and current dynamics are aligning in its favour.

Why are stakeholders bullish on coriander?

1) Declining global availability, especially in 2026:

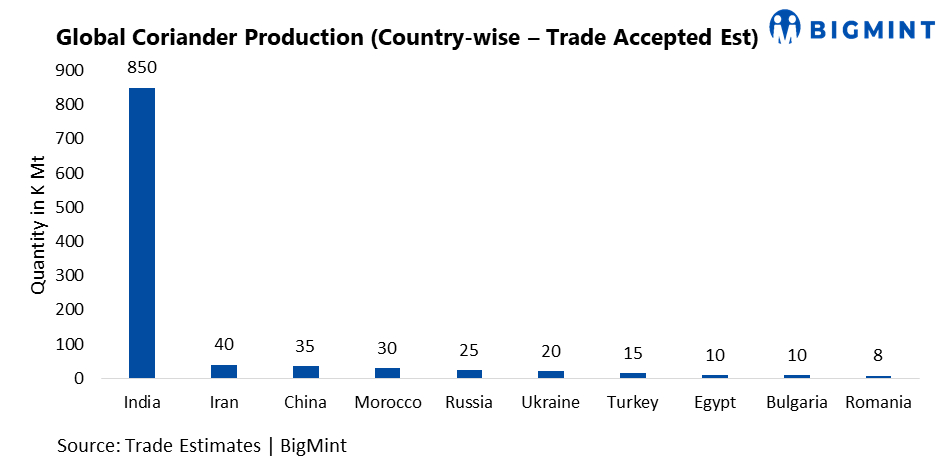

Global coriander output has weakened in recent years. Russia, once a major producer, has seen its production decline amid the ongoing war with Ukraine. Its ranking has slipped to fifth, with output at just 25,000-30,000 tonnes (t) annually and a marginal 2-3% share compared to India’s dominant 60-65%.

Iran, another key producer with 40,000-50,000 t, faces uncertainty due to ongoing geopolitical tensions involving the US and Israel, potentially further tightening global supplies.

India’s production has also been affected. Acreage has declined as farmers shift to more remunerative crops, while erratic weather — particularly unseasonal rains — has impacted both yield and quality, resulting in lower output estimates.

2) Rising consumption amid constrained supply:

The anticipated drop in production is creating room for imports, although many market participants believe domestic output could bridge the gap. Historically, India has imported coriander only in limited volumes, and current geopolitical disruptions are further restricting import opportunities.

Global coriander production has remained in the range of 10.43-11.72 lakh tonnes in recent years, with India as the leading producer. However, India’s output is expected to fall to 8.30 lakh tonnes in 2025-26 from 9 lakh tonnes in 2024-25 due to adverse weather.

Consumption, on the other hand, continues to rise steadily and is projected to reach 6.50 lakh tonnes in 2025-26, up from 6.40 lakh tonnes in the previous year and 5.71 lakh tonnes in 2020-21. The marginal deficit has already led to a gradual increase in imports — from 0.05 lakh tonnes during 2022-24 to 0.06 lakh tonnes in 2024-25.

3) Declining carry-forward stocks: Carry-forward stocks are tightening after several years of build-up. Stocks had risen from 1.1 lakh tonnes in 2020-21 to 1.5 lakh tonnes in 2024-25 but are now expected to decline to 1.2 lakh tonnes in 2025-26.

With most of the domestic production being consumed, the pipeline entering the new crop year remains thin, adding to supply-side pressure.

India’s coriander acreage is also expected to decline to 6.4 lakh hectares in 2025-26 from 7.40 lakh hectares in the previous year, further constraining supply.

4) India in strong position to influence prices: Given the tight global and domestic supply scenario, India is well-positioned to command prices. Coriander spot prices on NCDEX have increased significantly from INR 6,200-6,800/quintal in 2020-21 to INR 9,500-11,200/quintal in 2024-25 — and are projected to rise further to INR 10,500-11,800/quintal, marking an increase of over 70%.

“Except for India, no other country is producing significant volumes of coriander. This gives India a clear edge in price discovery,’ a market participant noted.

Outlook

Exports, particularly to the Middle East, may face near-term headwinds due to disruptions linked to the Strait of Hormuz, including elevated freight rates, higher bunker costs, and vessel delays. However, the underlying tight global supply and firm domestic demand are likely to keep prices supported, reinforcing India’s dominant position in the global coriander market, especially in the near-to-medium term.

Leave a Reply