- Export prices in Brazil increase w-o-w

- Strong mill demand supports US scrap sentiment

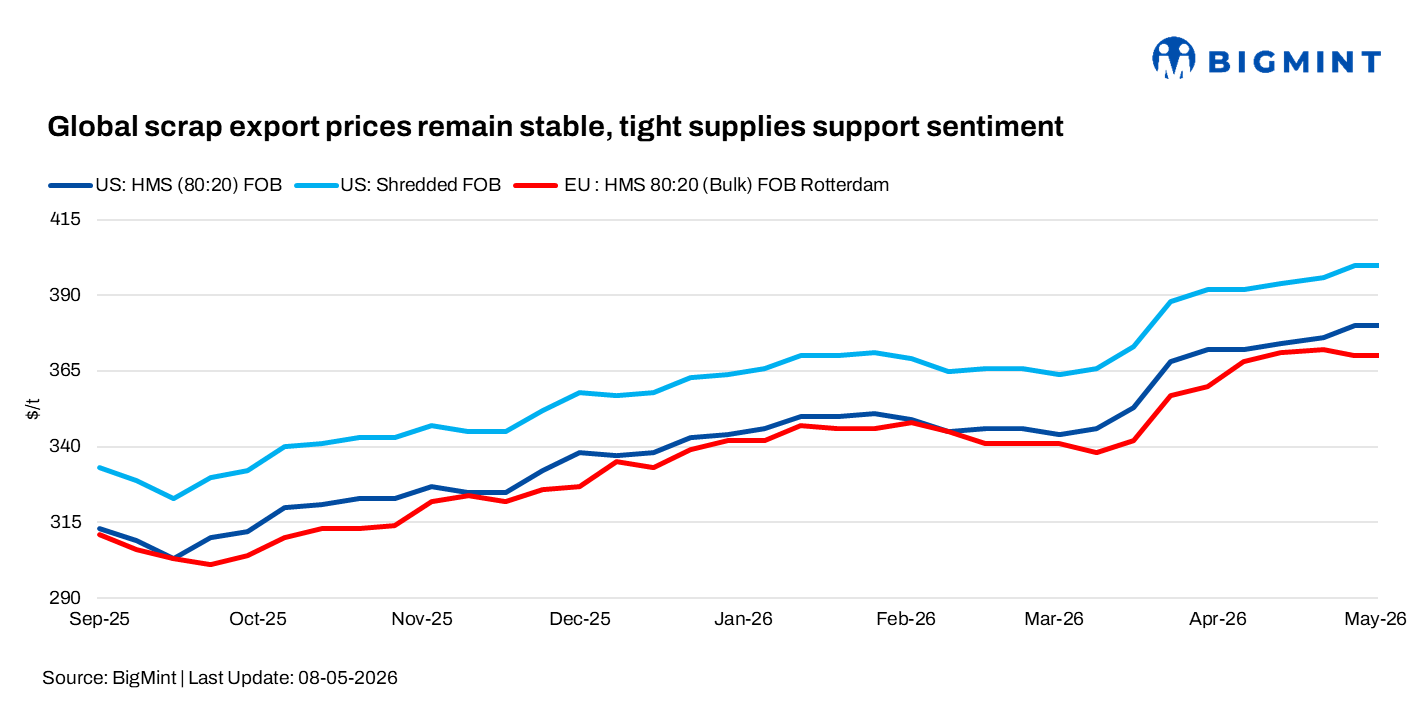

Global ferrous scrap export markets remained largely stable in the week ended 8 May, supported by firm mill demand, tight scrap availability, and elevated freight costs. US export prices stayed steady, EU trading activity remained slow, while Brazil’s market stayed balanced amid mixed buying sentiment and limited price movement.

US export scrap prices remained largely stable w-o-w, with HMS 80:20 at $380/t FOB and shredded scrap at $400/t FOB. Ferrous scrap sentiment stayed firm as May negotiations progressed, supported by steady mill demand.

US-origin HMS 80:20 export prices to Turkiye increased to $414/t CFR, while prices to Vietnam remained stable at $398/t CFR. Bangladesh import prices for US-origin HMS 80:20 decreased by $2/t to $398/t CFR.

Domestic shredded scrap prices stayed around $430/t DAP, while HMS remained near $380/t DAP. Strong bushelling demand continued amid elevated pig iron prices, though ample domestic supply capped sharper price increases.

EU export scrap prices remained range-bound during the week, while trading activity stayed limited due to the mid-week bank holiday in Europe. Higher freight costs and cautious buying also weighed on market activity.

Rotterdam scrap prices remained largely stable w-o-w, with UK HMS 80:20 dock levels rising by Euro 5/t ($6/t) to around Euro 305/t ($359/t).

Brazil’s ferrous scrap market remained largely stable in the week ended 8 May, with mixed sentiment as recyclers pushed for higher prices while mills maintained cautious buying. Trading activity improved slightly for May bookings, though price direction remained unclear.

Domestic prices stayed mostly stable, with HMS 80:20 around BRL 847-850/t ($172-173/t), turnings near BRL 765-770/t ($155-156/t), and clean scrap close to BRL 925-930/t ($188-189/t). Export HMS prices rose by around $10/t w-o-w to nearly $310/t FOB, while shredded scrap was heard near $330/t FOB.

Outlook

Global ferrous scrap export markets are expected to remain largely stable in the coming days, supported by firm mill demand, tight scrap availability, and elevated freight costs. However, weak finished steel demand and cautious buying across key regions may continue to limit stronger price gains.

Leave a Reply