- Domestic prices in Western Europe rise on firm steel demand

- US offers steady as suppliers shift focus to domestic market

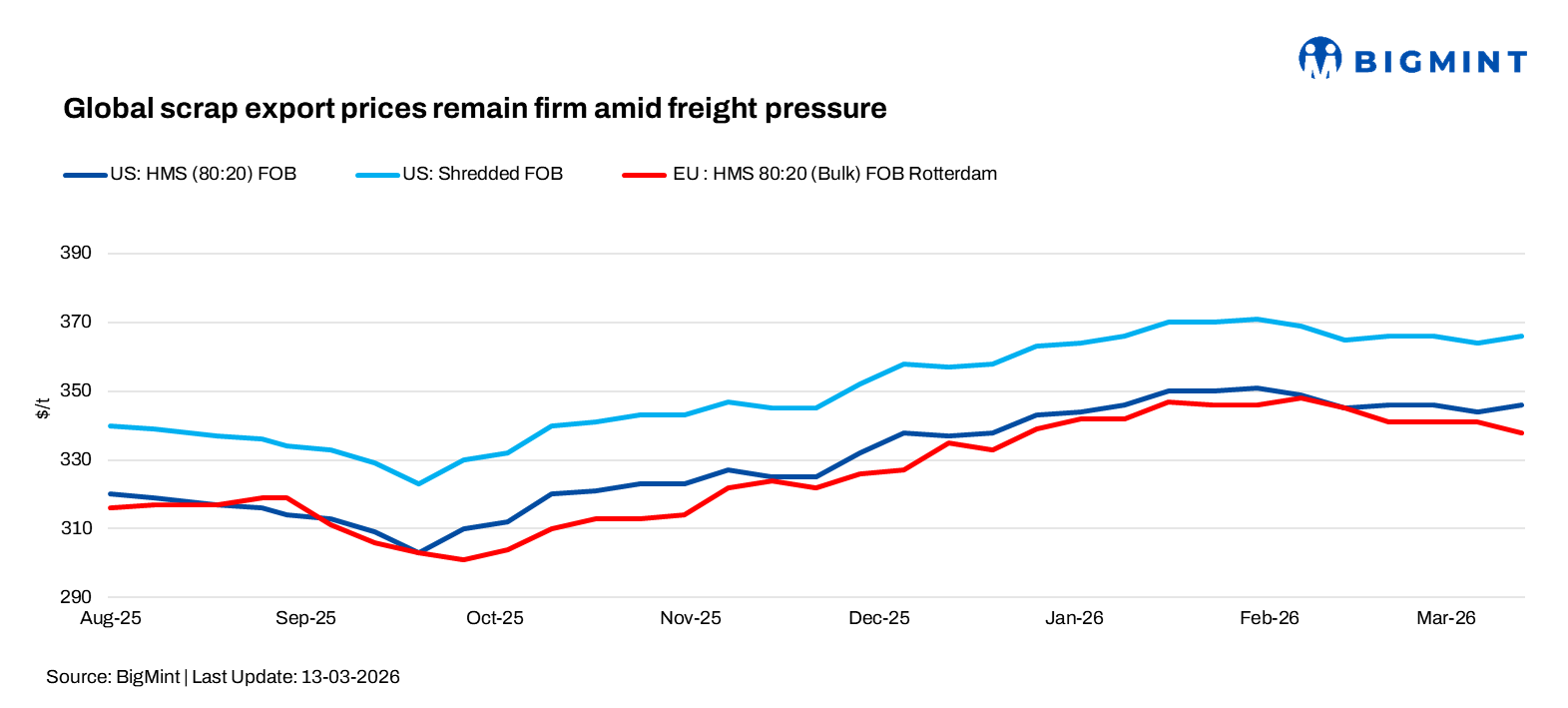

The global ferrous scrap export market showed mixed trends in the week ended 13 March, as rising freight costs and geopolitical uncertainty influenced trade. While US export activity remained largely frozen, Europe and Brazil saw firmer domestic markets, and Mexico stayed relatively stable with slightly slower buying.

US ferrous scrap export activity remained largely subdued in the week ended 13 March, as rising freights and uncertainty over potential war-risk surcharges kept buyers and sellers on the sidelines. Freight from the US East Coast to Turkiye was heard around $60/t, up from $35-40/t, limiting fresh deal activity.

Meanwhile, the US domestic scrap market remained stable in March, with mills rolling over February prices. Busheling held at $445-448/t Midwest and $450-452/t Southeast, while shredded stayed near $450-455/t delivered. Firmer finished steel prices, with Midwest HRC close to $995-1,000/t, supported sentiment and encouraged mills to maintain procurement levels.

As a result, some exporters redirected scrap to the domestic US market due to higher freight costs. In Bangladesh, a bulk cargo was heard at around $372/t CFR Chattogram for HMS (80:20) and $377/t CFR for shredded. Market sources also noted that a major Chattogram-based mill booked two bulk cargoes in the past three to four weeks — one from the US West Coast at $373/t and another from Australia at $374/t — mainly to replenish tight scrap inventories.

Dock scrap prices in Europe were heard at EUR 270-275/t ($308-314/t), up by EUR 5/t ($6/t) w-o-w on a firmer domestic sentiment. Freights from Europe to Port Qasim and other South Asian ports were estimated at $65-70/t, amid higher bunker and oil prices.

Based on these levels, UK-origin shredded scrap offers to Pakistan were heard around $405-410/t CFR Qasim, while buyers indicated bids closer to $400-405/t. Market participants noted the last trade at $405-412/t, though workable levels have since eased to around $400-405/t after the recent price spike, as demand remains cautious.

Meanwhile, the Western European scrap market strengthened, with domestic prices rising EUR 5-15/t ($6-17/t) amid higher energy costs and stronger long steel demand. E40 was heard at EUR 315-320/t ($360-365/t), E3 at EUR 300-310/t ($340-355/t), and E8 around EUR 300-305/t ($340-350/t) delivered.

European steel prices remained largely stable, although rising energy costs could push production costs higher if the trend continues.

In Brazil’s scrap export market, HMS prices held around $285/t FOB, while shredded scrap was heard near $305/t FOB amid freight uncertainty.

Brazil’s domestic ferrous scrap market firmed in the week ended 13 March, with steelmakers raising bids to secure volumes. Most price adjustments were around BRL 50/t ($10/t), though increases of up to BRL 200/t ($38/t) were reported for some grades such as shredded and oxycut scrap.

The rise was partly linked to higher domestic pig iron prices, prompting some mills to increase scrap usage. However, sentiment remained mixed, with several mills reporting adequate inventories and stable consumption.

Mexico’s ferrous scrap market showed mixed sentiment in the week ended 13 March, with demand remaining steady but buying activity slightly slower than in previous weeks. Mills continued to make inquiries but were more cautious with purchases.

Busheling was heard around MXN 8,000-8,500/t ($448-476/t) FOT Northeast, while HMS 90:10 was reported near MXN 7,300-7,500/t ($409-420/t). Some deals for busheling and HMS were also reported around MXN 7,800/t ($437/t), with sellers confirming trades near MXN 8,100-8,200/t ($454-459/t).

Market participants noted that scrap collection is gradually improving, and most expect March market conditions to remain similar to February, supported by balanced supply and steady demand.

Outlook

BigMint expects the US scrap market to face downward pressure in April as scrap flows improve, although strong steel prices may continue to support prime grades. In Europe, scrap prices are likely to remain supported by steady demand, though rising freight costs could limit export deals.

Leave a Reply