- Fire at Valero Port Arthur Refinery disrupts petcoke supply

- Strong Asian demand pushes prices to three-year highs

The global petroleum coke market has entered a period of acute volatility, driven by a confluence of severe supply shocks and relentless demand. A major fire at one of the largest US Gulf Coast (USGC) refineries has forced the suspension of significant petcoke volumes, exacerbating an already tight market characterised by soaring prices and aggressive bidding from key consumers in India and China.

USGC supply shock

The market was rocked on 23 March when an explosion and subsequent fire occurred at Valero’s massive 380,000 barrel-per-day refinery in Port Arthur, Texas. The facility, one of the largest in the United States, is a critical node in the US fuel supply chain and a major producer of high-sulphur fuel-grade coke, with an estimated annual output of approximately 2 million tonnes (mnt).

In the aftermath, Valero issued a stark notice to customers, stating that it would need to “suspend or postpone performance of Petcoke cargoes at Valero Port Arthur in the near term.” All scheduled cargoes without a completed and accepted vessel nomination are considered “postponed until further notice.”

Industry sources expect the refinery could be operating at reduced rates or completely offline for weeks, with some estimates suggesting a potential three-month outage. This immediate removal of a major supply source has injected a significant premium into the market, as traders and end-users scramble to secure replacement tonnes.

A market on the precipice

While the full impact of the Valero outage will be felt in March and beyond, February’s export data from the US Atlantic & Gulf Coast provides a baseline of a market already tightening. Total petcoke exports in February 2026 reached approximately 2.29 mnt.

Texas ports dominated the export landscape, led by the Houston and Sabine River districts. Key export destinations for February included:

- Asia: India and China remained primary destinations, receiving significant volumes.

- Latin America: Mexico, Honduras, Guatemala, and the Dominican Republic were consistent offtakers.

- Europe & Mediterranean: Turkiye, Spain, France, the Netherlands, and Italy received notable volumes, with Turkiye standing out as a major destination.

- Other Regions: Brazil emerged as a significant importer in February, with multiple cargoes loading for Brazilian destinations.

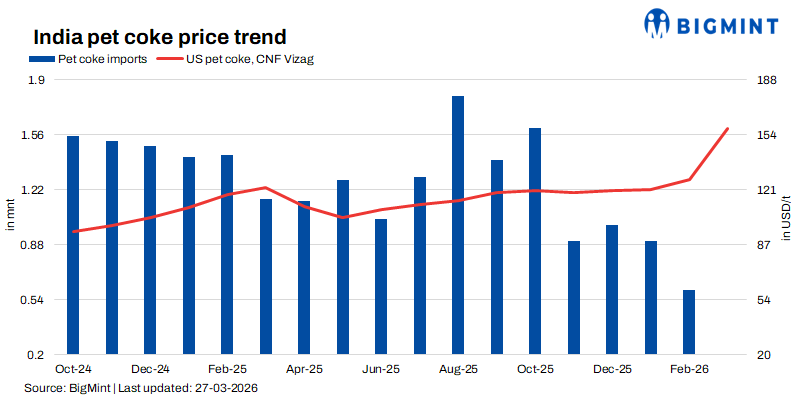

Price dynamics: Surge to 3-year highs

The supply constraints, now compounded by the Valero outage, have sent prices rocketing. The upward trajectory has been most pronounced in key importing regions, with CFR India 6.5% sulphur coke prices reaching fresh three-year highs, supported by firm FOB offers and rising freight costs.

Market feedback confirms that buying activity, particularly from India, remains frantic despite the elevated price levels. Market hearsay indicates that a USGC cargo was purchased by an Indian buyer at $162/t CFR, while another Indian cement producer secured a cargo at a premium $169/t CFR. An Oman tender was awarded to a Chinese trader at $160/t CFR Rizhao, significantly above bids from Indian cement plants, which were in the low to mid-$150s. General trader offers for US-origin material to India were heard in the $160-165/t CFR range.

This buying spree is occurring even as domestic cement producers in India signal pain. One major Indian cement manufacturer reported receiving offers in the $160-170/t range while bidding in the low $150s. The buyer noted that companies without stockpiles are “left with no options other than buying above $160 levels.”

The table below summarizes the latest price assessments for key petroleum coke grades across major markets:

Market outlook: A perfect storm

The current market is a textbook case of a “perfect storm”:

- Production loss: The Valero Port Arthur outage has removed a significant chunk of USGC supply, creating a void that other producers will struggle to fill quickly.

- Geopolitical disruption: The ongoing US-Iran war has effectively closed the Strait of Hormuz, choking off supply from key Middle East producers like Kuwait and Saudi Arabia and rerouting global trade flows, which adds significant freight and logistical complexity.

- Competitive demand: Indian cement makers, who had switched to coal in late 2025, are being forced back into the petcoke market as prices for both fuels surge. Meanwhile, Chinese buyers, including traders and anode-grade consumers, are competing aggressively for the limited available volumes.

With the duration of the Valero outage uncertain and geopolitical tensions showing no sign of abating, the market is expected to remain tight. Cement producers and other consumers without secured inventories face a challenging period of high input costs and intense competition for a dwindling pool of spot cargoes. The only potential relief could come from a faster-than-expected restart in Port Arthur or a sudden de-escalation of the conflict in the Middle East, but neither scenario appears imminent in the near term.

Leave a Reply