- Persistent market uncertainty leads to cautious sentiment

- Lower fixtures, ample vessel supply pressure Capesize freights

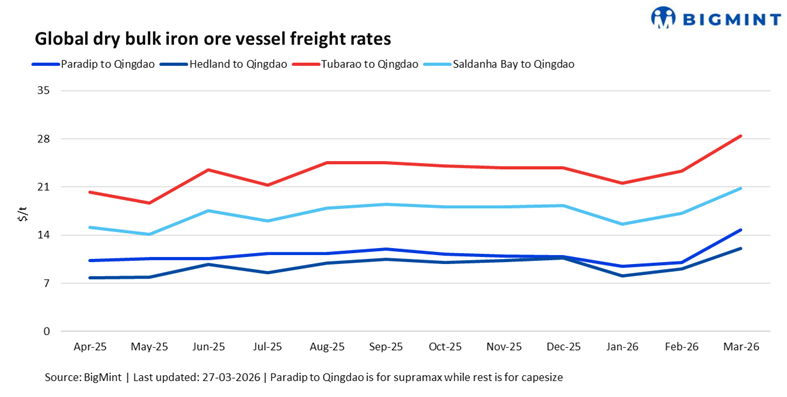

Dry bulk iron ore freights exhibited mixed trends w-o-w. Supramax rates from India increased on the back of steady minor bulk cargo flows and improved regional demand. Meanwhile, Capesize rates on key routes inched lower following recent gains, driven by fixing activity at lower levels, ample vessel availability, and cautious sentiment due to weather disruptions and broader market uncertainty.

Port operations across Western Australia’s Pilbara region were disrupted as Tropical Cyclone Narelle intensified, prompting closures at key export terminals including Dampier and Ashburton. With the system expected to strengthen further and gale-force winds already impacting coastal areas, market participants are closely monitoring developments, as any prolonged disruption could affect iron ore shipment schedules and tighten near-term vessel availability.

Route-wise updates

Market highlights

- DCE iron ore futures drop w-o-w: Iron ore futures on the Dalian Commodity Exchange dropped by around RMB 4.5/t ($0.65/t) w-o-w to RMB 812/t ($117.49/t) on 27 March, primarily due to cautious buying by Chinese mills amid adequate port inventories and subdued steel demand.

- Baltic Index drop w-o-w: The Baltic Index dropped 43 points w-o-w to 2,014 on 26 March. Additionally, Capesize gained 9 points to 2,974 on improved fixtures, driven by increased iron ore shipments, while Supramax fell 24 points to 1,205, pressured by softer minor bulk demand and limited fresh enquiries in key regions.

- Brent crude futures climb up w-o-w: Brent crude oil futures increased by about $2.8/bbl w-o-w to $110/bbl (May 2026 contract) on 27 March. Geopolitical tensions and lower inventory levels in major consuming regions supported bullish market sentiment, pushing prices higher.

- Bunker prices decline w-o-w: Bunker prices declined by $144/t w-o-w to $859/t on 27 March, amid softer crude oil prices, easing demand, and reduced geopolitical risk premiums despite ongoing conflicts.

Outlook

The outlook remains uncertain, with volatility driven by cyclone-related disruptions in key loading regions and ongoing geopolitical tensions continuing to cloud sentiment. Buying interest is likely to remain cautious next week, as participants adopt a wait-and-watch approach amid unclear demand visibility and an uncertain freight rate trajectory.

Leave a Reply