- China witnesses moderate growth of 1.2% y-o-y

- Asian surge offsets declines in Europe and North America

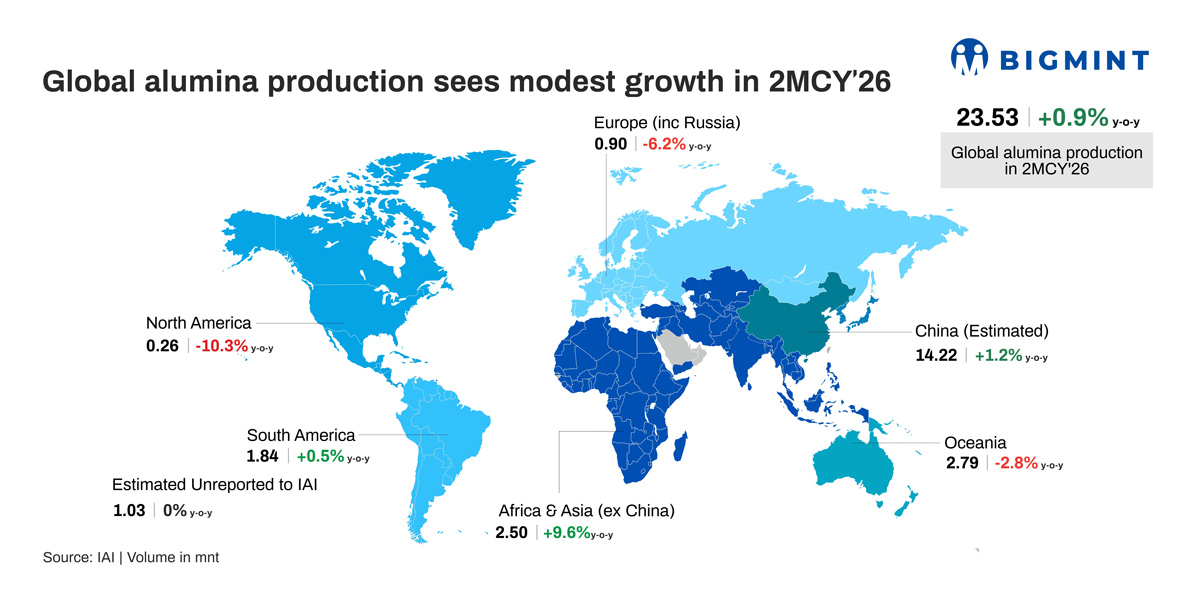

Global metallurgical alumina production stood at 23.53 mnt in 2MCY’26, marking a 0.9% y-o-y increase, reflecting modest growth in global output levels. The moderate rise reflects stable refinery operating conditions across major producing regions, supported by balanced market fundamentals despite regional variations. Continued capacity additions and steady demand from the aluminium sector, along with relatively stable supply dynamics, have helped sustain a measured production outlook.

Regional drivers shaping global metallurgical alumina output

Global metallurgical alumina production in 2MCY’26 exhibited varied regional trends, reflecting a mix of structural constraints and growth drivers across key producing regions.

China, the world’s largest alumina producer, recorded moderate growth of 1.2% y-o-y, supported by high refinery utilisation rates and incremental capacity additions, despite regulatory controls and balanced domestic demand conditions.

In Africa & Asia (excluding China), production increased significantly by 9.6% y-o-y, driven by capacity expansions in Indonesia and improved refinery operations in India and the Middle East, supported by better feedstock availability and operational efficiencies.

South America posted modest growth of 0.5% y-o-y, supported by stable refinery operations in Brazil, although gains remained limited due to operational constraints and cost pressures.

Conversely, Oceania witnessed a 2.8% y-o-y decline, primarily due to maintenance shutdowns and operational disruptions at key Australian refineries, impacting regional output levels.

Europe (including Russia) saw a 6.2% y-o-y decline, as elevated energy costs and geopolitical uncertainties continued to weigh on refinery operations and output stability.

North America recorded the sharpest decline of 10.3% y-o-y, reflecting structural limitations, lower refinery utilisation, and higher production costs, which constrained output.

Finally, estimated unreported production remained stable, indicating consistent output levels from non-reporting regions.

Overall, global alumina production growth remained modest, supported by capacity expansions, steady demand from the aluminium sector, and stable refinery operations, while regional disparities, energy costs, and operational challenges continued to influence output trends.

Factors influencing production trends

Production trends were shaped by the gradual ramp-up of newly commissioned capacities, particularly in Indonesia and other emerging regions, where several projects remain in early commissioning phases and have yet to reach optimal utilisation levels. At the same time, bauxite availability continued to act as a structural constraint, especially in Indonesia, where mining quotas remain limited relative to expanding refining capacity, moderating the pace of output growth.

Despite these constraints, improved refinery utilisation rates and stable feedstock flows across major producing regions, including China and Asia, supported consistent output levels. Ongoing developments—such as capacity expansion in Indonesia, downstream integration in the Middle East, refinery projects in Africa, and investments in the US—are expected to support long-term supply growth while keeping near-term output gains measured.

Outlook

Global metallurgical alumina production is expected to remain stable with moderate growth in the near term, supported by capacity additions and steady aluminium sector demand, although gains are likely to remain measured due to ongoing ramp-up of new refineries.

However, bauxite supply constraints, energy cost pressures, and regional operational challenges may limit sharper output increases. While higher refinery utilisation in China and Asia will support overall output, regional disparities and supply-side constraints are likely to keep production growth gradual and uneven, with trends closely linked to feedstock availability and commissioning timelines.

Leave a Reply