- Vessel shortages limit cargo availability

- Deep-sea scrap prices edge up w-o-w

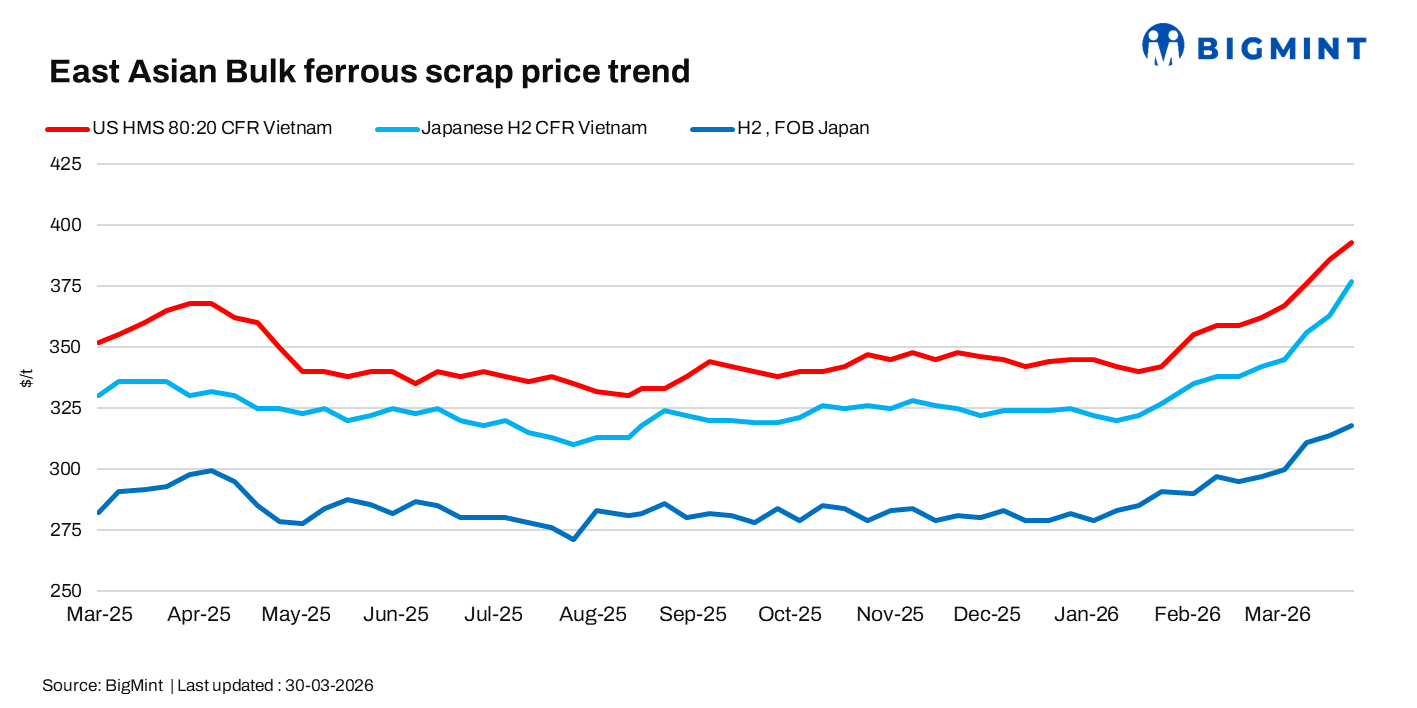

East Asian scrap markets strengthened during the week ended 30 March, supported by firmer Japanese export offers and limited cargo availability due to vessel shortages. Rising freight rates and logistical risks kept offer levels elevated, while buying activity in Vietnam remained cautious as mills relied on existing inventories and avoided high-priced bookings.

Weekly assessments

- Japanese H2 scrap was at $377/t CFR Vietnam, up by $14/t w-o-w.

- H2 scrap was at JPY 50,800/t ($320/t) FOB Tokyo Bay, up by JPY 750/t ($3/t) w-o-w.

- US-origin HMS 80:20 bulk stood at $393/t CFR Vietnam, up by $7/t w-o-w.

Japan: Export scrap prices rise on tight supply

H2 export prices were assessed at JPY 50,800/t ($318/t) FOB Tokyo Bay, up JPY 750/t w-o-w, supported by higher domestic prices after Tokyo Steel raised purchase rates by JPY 1,000/t to JPY 50,000/t across plants. Firm overseas demand, rising freight costs, and ongoing Middle East risks continued to support pricing.

Market participants reported H2 offers at JPY 50,000-52,000/t FOB, with CFR Bangladesh levels at $390-395/t, factoring in freight of $65-70/t.

Japan’s export prices reached a 20-month high, while in Vietnam, limited H2 availability due to vessel shortages pushed offers to $375-380/t CFR, up around $15/t w-o-w, with freight near $55/t further constraining trade.

Vietnam: Limited trades amid high offers

Suppliers showed limited willingness to negotiate amid rising offer levels, while Vietnamese buyers remained cautious. A mill source indicated no firm bids at present, as inventories have already been secured. Indicative bids were heard at $370-375/t CFR Vietnam, with tradable levels around $375-380/t.

In the deep-sea segment, scrap prices edged higher during the week ended March, supported by limited offer availability. US-origin HMS 80:20 (bulk) was offered at around $400/t CFR Vietnam, while workable levels were heard lower at $380-385/t CFR. However, elevated risks and longer lead times continued to weigh on buying interest for deep-sea cargoes.

Outlook

Japanese export prices are expected to remain firm due to tight domestic supply and ongoing vessel constraints. In Vietnam, buying interest may stay cautious in the near term, but limited offer availability and high freight costs are likely to support prices.

Leave a Reply