- Brazil and India pullbacks outweigh resilient Australian exports

- Weak post-holiday freights pressure long-haul shipments

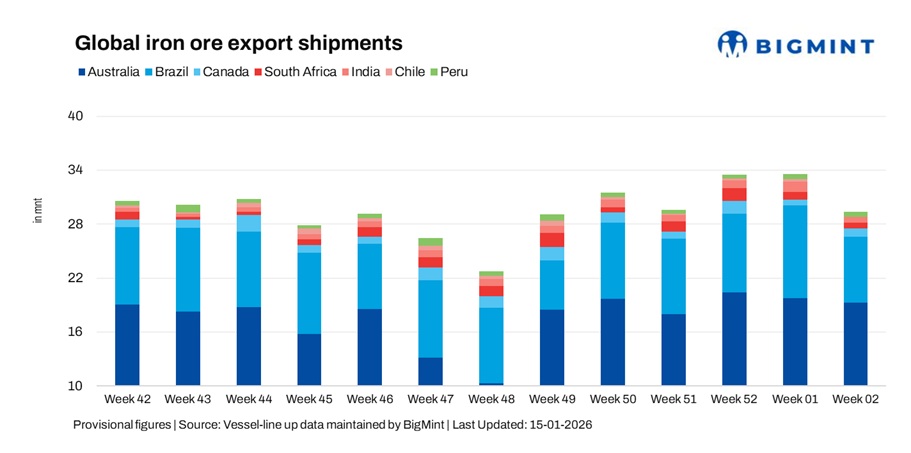

Global seaborne iron ore exports declined 12.6% w-o-w to 29.5 million tonnes (mnt) in the week ended 9 January, down from 33.7 mnt in week 01 (27 December-02 January), according to BigMint’s vessel line-up data. The decline marked a clear post-holiday correction, as cargo nominations slowed across major exporting regions following the release of deferred late-December shipments in the previous week.

The pullback was driven primarily by sharp weekly decline in exports from Brazil and India, alongside weaker flows from South Africa and the absence of shipments from Chile. These reductions more than offset relatively stable volumes from Australia, resulting in a broad-based softening of global shipment levels.

The weaker performance underscored the sensitivity of early-January trade flows to freight market conditions. Subdued spot rates, thin post-holiday fixing activity, and ample vessel availability reduced charterers’ urgency to commit to additional long-haul cargoes, particularly from Atlantic suppliers. As a result, exporters prioritised controlled shipment programs over volume expansion, reinforcing the overall decline in seaborne iron ore exports during the week.

Country-wise trends

Australian exports ease marginally but remain resilient

Australia’s iron ore exports edged down 2.6% w-o-w to 19.3 mnt in week ended 9 January, compared with the previous week, reflecting normalisation after the clearance of late-December cargoes and restrained post-holiday cargo stem issuance. Shipment activity remained steady but subdued, with exporters maintaining disciplined schedules amid muted freight sentiment.

Port Hedland dominated loadings at 12.39 mnt, followed by Walcott (3.09 mnt) and Dampier (2.90 mnt), indicating stable operations across key Western Australian ports despite the softer weekly outcome. BHP led shipments with 6.02 mnt, closely followed by Rio Tinto at 5.99 mnt and FMG at 4.82 mnt, while Roy Hill Infrastructure contributed 1.12 mnt. China remained the primary destination at 16.31 mnt, with Japan and South Korea importing 1.22 mnt and 0.98 mnt, respectively, underscoring Australia’s continued reliance on Asian demand.

Despite weak Capesize sentiment and thin post-holiday fixing, Australia’s proximity to key consuming markets and strong operational reliability, supported by recent moves by major miners such as BHP and Rio Tinto to strengthen long-term Pilbara operations through shared infrastructure and efficiency-driven collaboration, helped limit the downside and keep exports relatively resilient compared with other long-haul suppliers.

Brazil iron ore shipments slide on freight pressure

Brazil’s iron ore exports fell sharply by 29% w-o-w to 7.3 mnt in the week, reversing the strong recovery recorded in the previous week. The decline reflected the exhaustion of deferred cargoes released in late December, alongside softer long-haul fixing interest as freight markets remained under pressure.

Ponta da Madeira remained the leading loading port at 3.15 mnt, followed by Tubarao at 1.58 mnt, while Itaguai and Ilha Guaiba each handled 1.08 mnt, indicating a broad-based slowdown across Brazil’s key export terminals. On the supply side, Vale led shipments with 4.23 mnt, followed by CSN at 2.66 mnt, reflecting reduced cargo nominations after the prior week’s surge.

China continued to absorb the majority of Brazilian volumes at 4.31 mnt, while Oman and Malaysia imported 0.39 mnt and 0.29 mnt, respectively. However, subdued spot rates and price-sensitive chartering constrained fresh long-haul commitments, reinforcing Brazil’s exposure to freight-led corrections during periods of thin demand and weak post-holiday market sentiment, even as expanding production hubs in Minas Gerais and ongoing output plans by major miners continue to underpin Brazil’s long-term export capacity.

Canadian shipments rebound on selective Atlantic demand

Canada’s iron ore exports rose 58% w-o-w to 0.95 mnt in the week, recovering from subdued levels in the previous week. The rebound was driven by improved loadings at Sept-Iles, which handled 0.51 mnt, and Port Cartier at 0.44 mnt, supported by selective European demand and smoother post-holiday scheduling.

On the supply side, AMNS led shipments with 0.44 mnt, followed by IOC at 0.34 mnt and Guinea and Nimba Mines at 0.17 mnt, reflecting a measured return of cargo nominations after the holiday slowdown.

Despite the weekly increase, overall volumes remained modest, constrained by fragile Atlantic freight economics and cautious chartering behaviour. Export flows continued to hinge on long-haul freight viability, keeping shipment momentum uneven despite stable port operations across Canada’s key export terminals.

South Africa iron ore exports soften on weak fixing

South Africa’s iron ore exports declined 20.3% w-o-w to 0.72 mnt in the week, extending the pullback from the previous week. Saldanha Bay remained the sole and primary loading port, handling the entire 0.72 mnt, as cargo availability thinned amid weak freight sentiment and limited long-haul fixing interest.

China was the leading destination, importing 0.35 mnt during the week, while export flows to both Asia and Europe softened as buyers adopted a wait-and-watch approach. Although South Africa’s export base remains structurally resilient, weekly shipment performance continued to be driven by freight economics and cargo timing rather than underlying supply capacity.

Looking ahead, Indian buying may recover gradually, but East Asian demand is expected to remain cautious, making export momentum increasingly dependent on smaller yet consistent markets rather than a single large buyer driving growth.

Indian exports drop sharply as east coast momentum fades

India’s iron ore exports fell sharply by 41.9% w-o-w to 0.64 mnt in the week, down from 1.08 mnt in the previous week. The decline was driven by weaker loadings from east coast ports, with Paradip handling 0.33 mnt and Dhamra 0.17 mnt, as Supramax demand softened and post-holiday chartering activity remained selective.

On the supply side, Rungta Mines emerged as the leading shipper with 0.28 mnt, reflecting reduced cargo nominations amid subdued market conditions. Although regional freight rates remained relatively competitive, lower cargo availability and cautious buying interest weighed on shipment momentum.

China remained the primary destination, importing 0.34 mnt, reinforcing India’s role as a short-haul supplier to Asian markets. However, overall export performance stayed constrained amid weak freight sentiment and stronger domestic market priorities, limiting India’s ability to sustain higher shipment levels during the week.

Chile exports pause after prior-week rebound

Chile recorded no iron ore shipments in week 02, following a sharp percentage rebound in the previous week that was driven by the clearance of delayed cargoes, leaving no fresh stems immediately available during the week. The absence of loadings underscored the lumpy and timing-driven nature of Chile’s export flows, which remain highly sensitive to vessel positioning and cargo readiness, with softer post-holiday freight sentiment further discouraging shipments rather than any change in underlying demand.

Peruvian exports ease on selective fixing

Peru’s iron ore exports declined 6.8% w-o-w to 0.56 mnt in the week ended 9 January, easing from the recovery seen in the previous week. Shipments remained heavily concentrated at San Nicolas, which handled 0.51 mnt, while Matarani contributed 0.05 mnt, reflecting limited cargo availability from other ports.

On the supply side, Shougang Hierro accounted for the bulk of shipments at 0.51 mnt. China remained the sole and dominant destination, importing the entire volume during the week. However, overall export momentum stayed constrained by selective fixing and cautious chartering, keeping Peruvian shipments closely tied to cargo timing and prevailing freight conditions rather than broader market strength.

Freight weakness reinforces shipment pullback

Iron ore freight sentiment weakened during the week as year-end and New Year holidays curtailed fixture activity, keeping charterers largely on the sidelines and intensifying competition among shipowners amid ample vessel availability, particularly in the Pacific. Thin cargo enquiries and delayed procurement decisions reduced fixing volumes, forcing owners to concede on rates across major routes.

Although futures strengthened on restocking expectations, freight markets remained soft as trade flows were viewed as inventory-led rather than demand-driven, limiting urgency to secure vessels. As a result, long-haul Capesize trades came under greater pressure, while short-haul and regionally competitive suppliers fared better, contributing to the uneven and lower shipment profile observed in week 02.

Outlook

Global iron ore shipments are expected to stabilise in the near term as markets gradually move past the holiday period and deferred cargo programmes re-enter the market. Restocking ahead of the Lunar New Year and firmer iron ore prices may support near-term trade flows, particularly from Australia and Brazil.

However, ample vessel availability and still-fragile freight sentiment could cap any sharp recovery, keeping shipment momentum uneven across regions. Until clearer signals emerge on sustained steel demand recovery in China and freight markets regain balance, iron ore exports are likely to remain rangebound through January.

Leave a Reply