- Australian exports slide 16% following record-high Jan volumes

- Chinese New Year holidays, elevated port stocks dampen demand

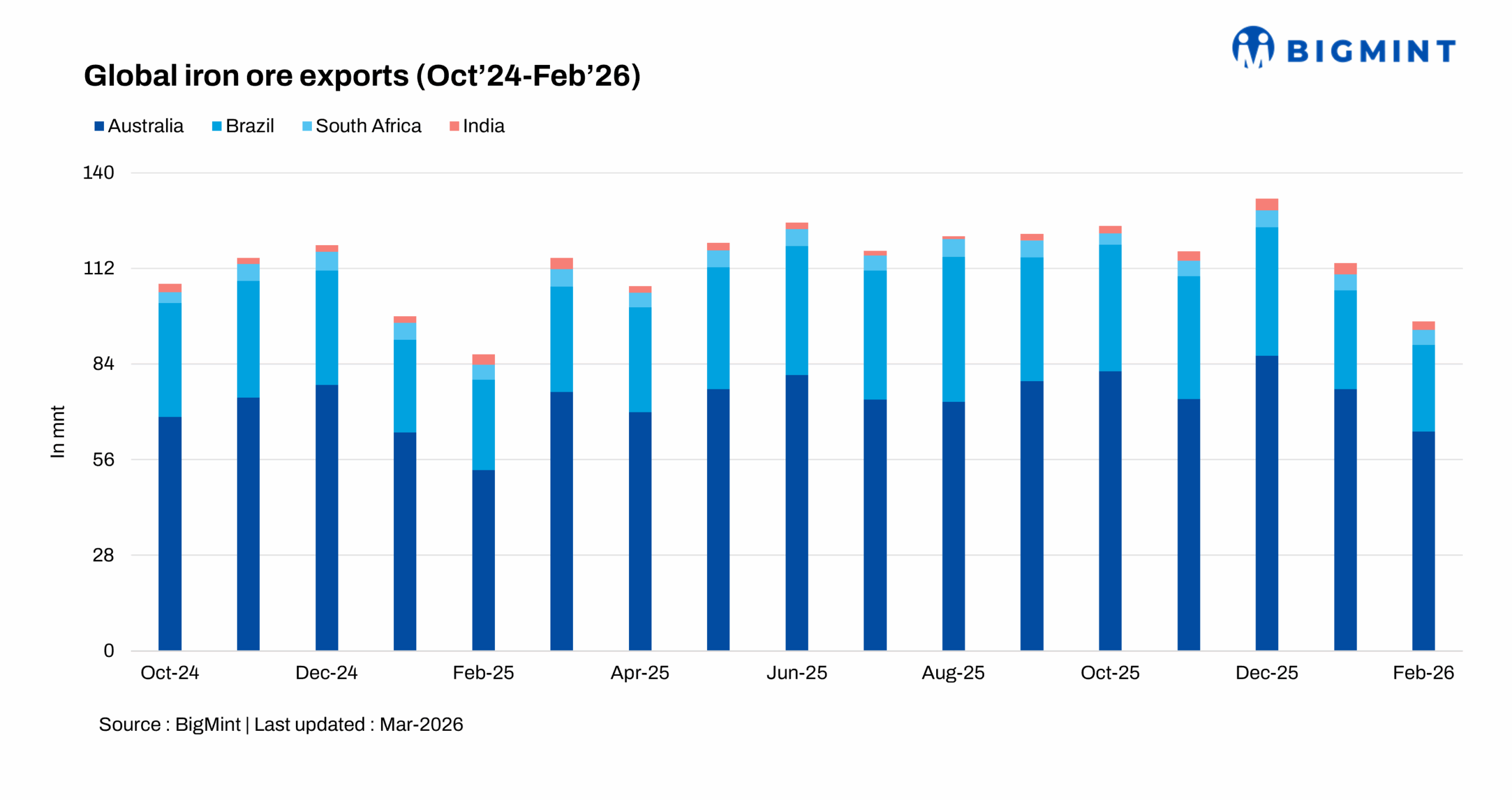

Iron ore (including pellets) exports from key global producers — Australia, Brazil, South Africa, and India — fell m-o-m in February 2026. This was largely driven by sluggish procurement by Chinese buyers amid rising portside inventories, which eased immediate supply concerns, and the nine-day Lunar New Year holiday break (15-23 February). To illustrate, Chinese iron ore and pellet portside inventories rose to 163.39 million tonnes (mnt) in February 2026 against 161.24 mnt in January 2026.

Australian exports drop over 15% m-o-m

Australia’s iron ore and pellet export shipments stood at 64.2 million tonnes (mnt) in February 2026, down 16.2% against 76.6 mnt in January 2026, according to vessel line-up data compiled by BigMint. However, shipments rose 21% y-o-y against 52.9 mnt in February 2025.

China remained the top importer, receiving 53.1 mnt, followed by South Korea at 4.1 mnt and Japan at 4.1 mnt. Rio Tinto was the leading exporter at 22.0 mnt, trailed by BHP at 20.7 mnt and FMG at 14.8 mnt.

Following record-high January shipments supported by operational upgrades at Port Hedland, routine maintenance activities undertaken by miners in February led to a m-o-m decline in export volumes. At the same time, Chinese demand weakened ahead of the Lunar New Year holiday, while elevated port inventories reduced the urgency for mills to book fresh Australian cargoes.

Exports from Brazil drop by 13% m-o-m

Brazil’s iron ore exports dropped by 12.5% m-o-m to 25.37 mnt in February 2026 against 28.99 mnt in the past month. Meanwhile, exports decreased by 4.4% y-o-y from 26.53 mnt in February 2025.

China remained the largest importer, taking in 15.38 mnt, followed by Malaysia at 2.28 mnt and Oman at 1.18 mnt.

Subdued Chinese steel output ahead of the Lunar New Year, elevated port inventories, and Vale’s reduced production outlook sharply curtailed buying appetite and export momentum. Logistical disruptions, including the Carajas rail blockade and port maintenance at key terminals, delayed cargo movement and restricted shipment loading capacity.

South African exports drop by 5% m-o-m

South Africa’s iron ore exports stood at 4.5 mnt in February 2026, a drop of 4.9% m-o-m against 4.73 mnt in January, as per vessel line-up data maintained by BigMint. However, export volumes edged up by 3.4% against 4.35 mnt in February 2025.

China remained the leading importer with 1.32 mnt, followed by the Netherlands at 0.66 mnt.

The decline in iron ore exports was primarily caused by persistent logistics bottlenecks at Transnet, limiting rail shipments to Saldanha Bay. The situation was further pressured by softer global prices due to slowing steel demand in China, additional supply from the Simandou mine in Guinea, and volatility in the South African rand.

India’s exports fall 25% m-o-m

India’s iron ore and pellet exports fell by 24.8% m-o-m to 2.48 mnt in February 2026 from 3.3 mnt in January. Moreover, iron ore and pellet exports decreased by 21.6% y-o-y against 2.04 mnt in the same period last year.

China remained the largest importer with 1.93 mnt, followed by Malaysia with 0.11 mnt.

Export sentiment remained subdued amid intense competition in the seaborne market, largely due to elevated inventories in China and the availability of alternative supply sources. Steel mills in China operated below full capacity, limiting fresh procurement.

Overall market activity was slow, with China largely on the sidelines as falling prices and comparatively better margins in domestic sales reduced the urgency for seaborne purchases.

Outlook

Overall buying sentiment and trade volumes are likely to pick up in March, as Chinese buyers restock material following the Lunar New Year slowdown. However, ore pricing will remain a key factor, as rising freight and insurance costs may prompt shippers to restructure short-term cargo offers to stay profitable.

Leave a Reply