- Prices retreat toward $1,900/t amid cautious sentiment

- MCX lead edges higher; open interest rises sharply

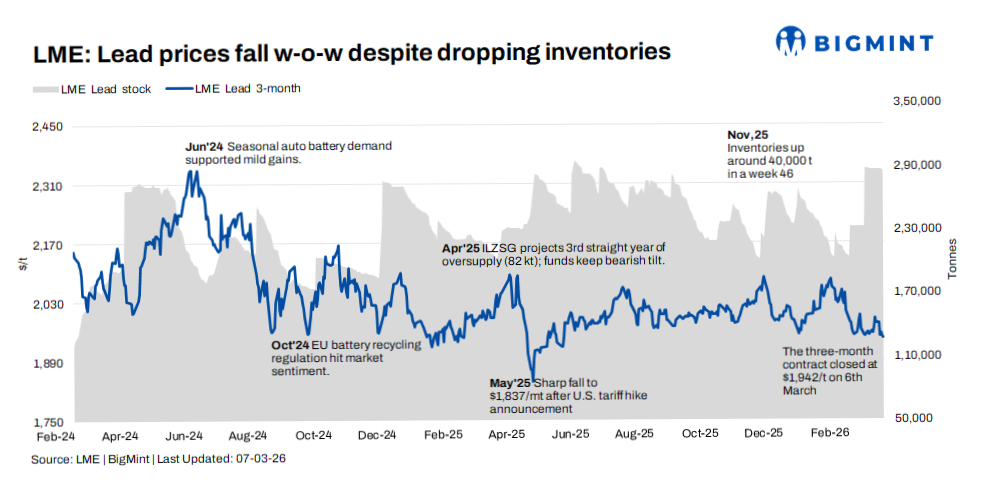

Lead prices on the London Metal Exchange (LME) edged lower in the week ended 6 March 2026, as early stability gave way to selling pressure later in the week. The market briefly held above the $1,930/t level at the start of the week but gradually weakened, with prices retreating toward the $1,900/t mark by Friday.

The three-month contract also softened after failing to sustain momentum above $1,950/t, reflecting cautious sentiment and limited buying interest at higher levels.

Price trends

LME cash lead opened at $1,934/t on 2 March before falling to a weekly low of $1,900/t on 6 March. Prices remained under pressure through the week and settled at $1,900/t, down compared with $1,928/t on 27 February, marking a modest week-on-week decline.

The three-month contract followed a similar trajectory. Prices started the week at $1,978/t, climbed briefly to a weekly high of $1,978/t, and then eased to $1,941.5/t by 6 March.

The inability of the contract to sustain levels above $1,950/t signalled a lack of strong bullish momentum, with sellers emerging during rallies.

Inventory analysis

LME lead inventories remained broadly stable during the week, with only a marginal drawdown.

Stocks stood at 286,100 t at the start of the week and edged lower to 285,900 t by 6 March, indicating a 200 t decline.

The minimal stock movement suggests that visible supply conditions remain largely balanced, offering limited support for sustained price gains. While the modest drawdown indicates some consumption, the absence of a sharper inventory decline continues to cap bullish sentiment.

SHFE lead trends

On the Shanghai Futures Exchange (SHFE), lead prices traded within a narrow range during the week.

Prices stood at $2,406/t on 2 March, slipped to $2,404/t on 3 March, and then recovered slightly to $2,410/t on 5 March before easing back to $2,404/t on 6 March.

The largely sideways movement in Shanghai indicated stable domestic market conditions in China, with neither strong demand recovery nor significant supply disruptions driving prices.

MCX price movements

On the Multi Commodity Exchange of India (MCX), the April 2026 lead contract traded within a narrow range of INR 323,200-332,750/t during the week.

Prices closed at INR 325,900/t on 6 March, slightly higher compared with INR 329,700/t on 2 March, reflecting mild volatility during the week.

Open interest rose sharply from 143 lots at the start of the week to 696 lots by Friday, indicating fresh participation in the market despite the subdued price trend.

Currency movements also played a role, as a relatively weaker Indian rupee against the US dollar kept imported metal costs elevated, offering some support to domestic futures.

Outlook

Lead prices are expected to remain range-bound in the near term, with $1,900/t acting as immediate support and $1,950–2,000/t emerging as a key resistance zone.

Stable LME inventories and muted demand signals from China suggest that strong directional momentum may remain limited. However, any sustained inventory drawdown or improvement in battery sector demand could provide support to prices.

Until clearer demand signals emerge, the market is likely to oscillate within the existing range, with buying interest emerging on dips while rallies encounter resistance near the upper end of the band.

Leave a Reply