- Higher exports from Brazil offset softer flows from South Africa, India

- Australian volumes rally, with improved loadings from Pilbara ports

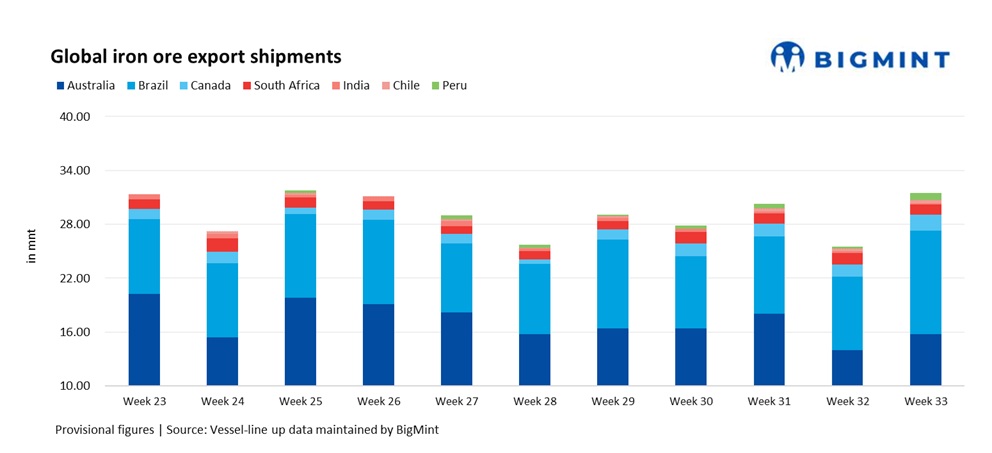

Global iron ore exports staged a strong recovery in Week 33, climbing up by 23% to 31.47 million tonnes (mnt) compared with 25.54 mnt in Week 32. Volumes hit a four-week high, underlining the resilience of supply chains despite seasonal headwinds. The rise was largely supported by increased loadings out of Brazil (+41.7%) and Australia (+12.6%), the two largest seaborne suppliers, which together contributed more than 85% of the week’s total shipments.

On the demand side, the pick-up came against the backdrop of Chinese steelmakers cautiously returning to procurement, even as mill margins remained under pressure. Traders highlighted that recent fluctuations in futures pricing on the Dalian Commodity Exchange (DCE) helped stimulate restocking interest, providing a short-term lift to seaborne cargo absorption. However, market participants remained wary about whether the current pace of exports could be sustained, which would depend on whether downstream steel demand in China improves through late August.

Country-wise exports

Australia, the world’s largest iron ore exporter, registered a strong rebound in Week 33, with shipments rising 12.6% to 15.75 mnt compared with 14 mnt in the prior week. The recovery was driven by smoother vessel clearances at key Pilbara ports, including Port Hedland, which saw shipments of 9.57 mnt, and Dampier, which handled 2.68 mnt, after weather-related disruptions earlier in the month.

Major miners such as Rio Tinto (5.82 mnt), BHP (5.58 mnt), and FMG (3.51 mnt) managed to normalise loading schedules, helping restore supply flows in the Pacific basin.

On the demand side, most shipments were directed to China (13.38 mnt), while smaller volumes were observed heading to Japan (0.80 mnt) and South Korea (0.44 mnt) amid shifting regional buying trends.

Brazil delivered the standout performance in Week 33, with iron ore exports surging 41.7% w-o-w to 11.56 mnt from 8.16 mnt in Week 32. Loadings gained momentum at Port Ponta da Madeira (4.79 mnt) and Itaguai (2.43 mnt), supported by improved operational efficiency and stronger global demand.

According to the mining lobby group Ibram, confidence in the sector has rebounded in recent months, aided by the progress of major projects in China and the resumption of production. Leading exporter Vale contributed 5.60 mnt, ramping up output after mid-year maintenance and earlier weather disruptions, which helped boost Atlantic flows.

The rebound also reflects Brazil’s seasonal export trend, with shipments typically recovering in the second half of the year as weather improves. China (4.03 mnt) remained the dominant buyer, with Brazilian ore’s higher-grade quality continuing to appeal to steelmakers seeking to meet stricter specifications. However, the longer-haul Brazil-China route remains cost-sensitive, and rising freights continue to pose a challenge for traders compared to shorter Australian shipments.

Canadian iron ore exports rose to 1.78 mnt in Week 33 from 1.37 mnt in the previous week, driven by stronger loadings at Sept-Iles (1.04 mnt) and Milne Inlet (0.59 mnt). Despite the seasonal navigation challenges in Canadian waters, the terminals continued to operate steadily, supporting consistent export flows.

This week, the Netherlands was the leading importer with 0.33 mnt, followed by Spain with 0.23 mnt and Germany with 0.20 mnt. The rise aligns with Canada’s recent export pattern, where fluctuations are generally linked to weather conditions or river logistics rather than supply-side constraints.

While Canada’s shipment volumes remain modest compared to Australia and Brazil, the steady w-o-w gains highlight its role in meeting incremental demand. Moreover, Canada’s reputation for supplying high-grade ore provides valuable diversification to global seaborne markets.

South Africa’s iron ore exports slipped to 1.13 mnt in Week 33, from 1.23 mnt in the previous week, as vessel activity through Saldanha Bay — the country’s key export hub — slowed. While volumes remained broadly in line with July averages, ongoing logistical constraints tied to port operations and rail connectivity continued to restrict shipment growth.

China remained the primary destination, taking in 0.36 mnt, followed by the Netherlands with 0.20 mnt, while additional cargoes moved to the Middle East and Europe, providing secondary demand support.

South Africa’s role in the global iron ore market has become increasingly important as buyers diversify supply away from the Brazil-Australia duopoly. However, recurring infrastructure challenges, particularly frequent Transnet railway disruptions, continue to limit the country’s ability to expand exports consistently.

India’s iron ore exports fell sharply to just 0.12 mnt in Week 33, compared with 0.23 mnt in Week 32. Weak buying interest from China, which is India’s primary export destination for low- to mid-grade fines, further weighed on volumes.

As such, India plays more of a supplementary role in seaborne trade, with its shipments tending to rise only when Chinese demand spikes and alternative supply becomes tight. Given the current oversupply from major miners, India’s contribution is expected to stay muted in the near term.

Chile’s iron ore exports inched up to 0.34 mnt in Week 33 from 0.31 mnt in Week 32, supported by steady loadings at Huasco and Totoralillo ports, each handling 0.17 mnt. While Chile’s contribution to global seaborne trade remains comparatively small, the country provides a reliable alternative supply source, particularly for Asian buyers.

Peru, by contrast, registered a sharp rebound with shipments of 0.79 mnt in Week 33, more than tripling from just 0.22 mnt in the previous week. The increase was supported by improved vessel clearances and steady operations at the San Nicolas (0.69 mnt) and Matarani (0.10 mnt) ports. While Peru is still a small player compared with giants such as Brazil and Australia, its ability to ramp up exports quickly provides flexibility in balancing short-term global supply.

Dry bulk iron ore freights recovered this week across major global routes, driven by steady demand and increased chartering activity from key exporters such as Australia and Brazil. Capesize rates strengthened in both the Pacific and Atlantic basins, supported by active fixing and firm shipment requirements, while Supramax freights on the India-China route also showed a positive trend. Market sentiment was further lifted by improved trading activity and stronger paper markets, though concerns lingered over ample vessel supply and falling oil prices, which could limit the sustainability of the uptrend.

Outlook

Looking ahead, global iron ore shipments are expected to remain robust as Brazil and Australia continue to push higher loadings into late August. However, demand-side risks persist, particularly from China, where weak steel margins and uncertainty in property demand continue to cloud the outlook. If Chinese mills curtail production in response to poor profitability, the export momentum could stall.

On the logistics front, vessel availability and freights will remain a critical factor. With Capesize rates in the Pacific and Atlantic basins firming, traders may see higher transport costs passed through to end-users. Additionally, weather risks, particularly in Australia and South America, alongside potential congestion in Asian discharge ports, will be key watch points in the coming weeks.

Leave a Reply