- Indonesia, Australia, Colombia lead rally, amid easing port congestion

- Indian imports slow down due to monsoon disruptions, high stockpiles

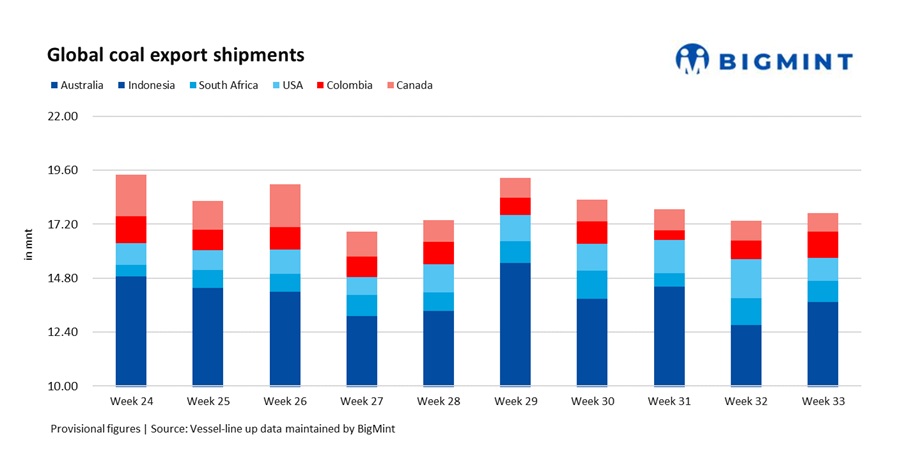

Global coal exports, across the six key origins monitored by BigMint through vessel line-up data, rose by 2% to 17.71 million tonnes (mnt) in Week 33, 2025 (9-15 August) from 17.36 mnt in Week 32 (2-8 August). The rebound was largely propelled by stronger shipments from Indonesia, Australia, and Colombia, which cumulatively exported 2.8 mnt more this week. However, these gains were counterbalanced by significant declines from the US and a moderate pullback from South Africa.

Sources noted that the early monsoon onset in India disrupted port operations, delaying cargo handling and vessel turnaround. On the other hand, cautious procurement by Indian buyers, buoyed by record thermal coal stockpiles at power plants, capped import demand.

Meanwhile, Chinese import volumes remained subdued, owing to persistently strong domestic production and expanded renewable energy generation amid slower industrial demand.

Country-wise exports

Indonesia: Coal shipments rose 7.8% to 7.31 mnt in Week 33 from 6.78 mnt in the previous week. The uptick was supported by improved vessel clearance at East Kalimantan ports, where weather disruptions eased.

However, demand from key Asian buyers, particularly India (1.85 mnt) and China (1.74 mnt), remained soft, reflecting robust domestic output and weaker summer electricity demand. Indian sponge iron producers scaled back imports amid lower prices in the domestic market.

Australia: Coal exports rose to 6.42 mnt in Week 33, an 8% w-o-w increase from 5.94 mnt.

Loadings improved across key ports, led by Newcastle (2.79 mnt), Gladstone (1.27 mnt), and DBCT (1.05 mnt), although weather-related disruptions continued to cap stronger gains.

On the demand side, buying interest from Japan (2.15 mnt) and South Korea (1.01 mnt) remained steady, while Chinese tenders stayed muted at just under 0.7 mnt.

According to BigMint, the recovery was primarily driven by the clearance of previously deferred cargoes rather than fresh demand, as weak steel sector margins in Asia continued to weigh on coking coal flows.

Colombia: Coal shipments rose sharply by 39.6% to 1.17 mnt in Week 33, from 0.84 mnt in Week 32. The increase was largely supported by European utilities boosting high-CV thermal coal procurement for autumn restocking, with the Netherlands taking around 0.17 mnt.

Demand from Asia also contributed, led by South Korea at 0.15 mnt. On the supply side, activity was concentrated at Puerto Nuevo (0.67 mnt) and Puerto Bolivar (0.30 mnt).

Colombian miners continued to benefit from firm interest in high-calorific-value coal, which has remained attractive to buyers amid ongoing volatility in global natural gas prices.

United States: Exports slumped sharply by 39.6% to 1.04 mnt in Week 33, from 1.73 mnt in the previous week, marking the steepest w-o-w decline among major origins.

The drop was largely driven by weaker Indian coking coal bookings, with steel mills in eastern India cutting imports to 0.27 mnt amid compressed margins.

On the supply side, loadings fell significantly at Norfolk (0.43 mnt) and Baltimore (0.26 mnt), while Mobile Port posted moderate volumes of 0.18 mnt. Meanwhile, European utilities scaled back procurement of US thermal coal, opting instead for competitively priced Colombian cargoes to meet autumn restocking needs.

South Africa: Exports slipped 21.4% w-o-w to 0.94 mnt, from 1.19 mnt. Shipments through Richards Bay Coal Terminal (RBCT) were affected by vessel scheduling delays and limited buyer interest.

Indian demand for South African coal, which had shown some recovery in Week 32, softened again amid persistent monsoon disruptions. However, some Atlantic-bound cargoes provided partial support, preventing a steeper drop.

Canada: Shipments fell modestly by 6.3% to 0.83 mnt from 0.88 mnt in the previous week.

Flows were steady to northeast Asia, particularly China (0.25 mnt) and South Korea (0.17 mnt), with minor volumes headed to Indonesia (0.15 mnt).

Vancouver led loadings at 0.25 mnt, followed by Prince Rupert at 0.08 mnt. Spot market activity remained limited, with most volumes tied to long-term contracts.

Freight trends

Dry bulk coal freights to India strengthened w-o-w, with Panamax rates firming on the Australia and South Africa routes and Supramax ones on the Indonesia-India corridor holding steady. The uptick was supported by increased fixing activity, stronger paper market sentiment, and slightly higher bunker costs, even as overall Asian trading remained subdued.

Monsoon rains in India disrupted port operations and vessel turnaround, contributing to tighter availability, while portside thermal coal inventories eased. Futures in China edged higher w-o-w on supply concerns linked to government inspections of coal mines.

Outlook

In the near term, Indonesia and Australia are expected to maintain moderate export strength on improved weather and better port operations, while Colombia is likely to benefit from sustained European demand. By contrast, US and South African exports may remain under pressure due to weaker Indian demand and logistical constraints.

Leave a Reply