- Cargo flow improves in Australia post New Year holidays

- Firmer Capesize sentiment supports selective long-haul fixing

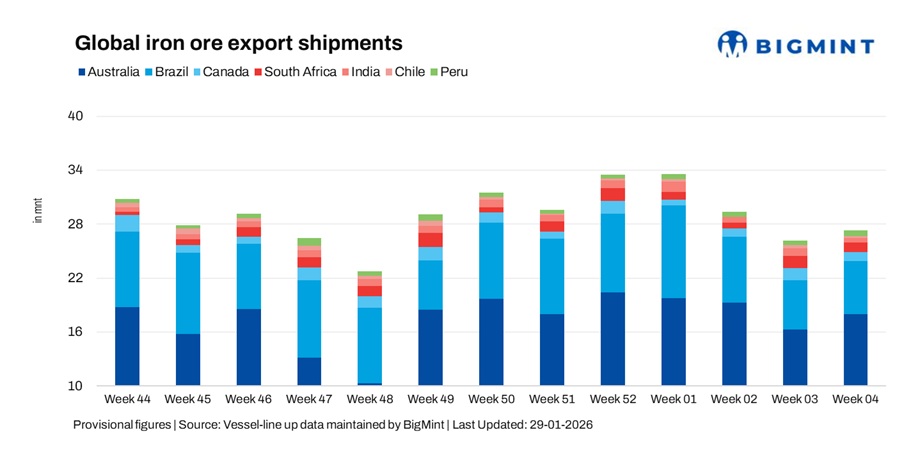

Global seaborne iron ore exports rose 4% w-o-w to 27.2 million tonnes (mnt) in the week ended 23 January 2026, compared with 26.2 mnt in the previous week, as per vessel line-up data. The uptick followed a weak mid-January showing and two straight weekly declines, and it was driven by higher cargo releases from major producers and firmer Capesize freight sentiment. However, overall shipment momentum remained capped by cautious chartering behaviour, uneven demand signals, and ongoing weakness in steel market fundamentals.

The weekly rise was led by higher shipments from Australia and Brazil, which more than offset declines from Canada, South Africa, India, and Chile, while Peru saw a marginal increase. Despite improved fixture flow, exporters continued to manage shipment schedules carefully, preferring selective fixing amid mixed freight signals and subdued buying appetite.

Country-wise trends

Australian shipments rebound on improved cargo flow

Australia’s iron ore exports rose 10.7% w-o-w to 18 mnt, rebounding from a two-month low as fresh cargo releases and improved Capesize sentiment on the West Australia-China route encouraged selective fixing. Post-holiday normalisation of loading schedules also supported the recovery, though overall volumes remained below early-January highs amid cautious buying.

Port Hedland led loadings with 11.9 mnt, followed by Walcott (3.3 mnt) and Dampier (2.5 mnt), reflecting stable operations across Western Australia. On the shipper side, BHP and Rio Tinto led exports with 5.9 mnt and 5.8 mnt, while FMG and Roy Hill Infrastructure shipped 4.6 mnt and 1.2 mnt, respectively.

China continued to dominate as the primary destination with 14.7 mnt, while Japan and South Korea imported 1.5 mnt and 1.1 mnt, respectively. Despite the w-o-w rebound, exporters remained sensitive to freight economics and market timing, keeping shipment growth measured amid softer Chinese steel demand. Australia’s rebound also reflects its structurally dominant role in global iron ore supply, supported by strong export capacity and flexible logistics despite softer prices and cautious Chinese buying.

Brazil’s exports rise modestly as long-haul fixing improves

Brazil’s iron ore shipments rose 6.5% w-o-w to 5.91 mnt, marking a second consecutive week of stabilisation after sharp earlier declines. Improved Capesize freight sentiment on the Brazil-China route supported selective long-haul fixing, while exporters released limited fresh cargoes to test market depth.

Tubarao led port-wise loadings with 2.0 mnt, followed by Itaguai at 1.3 mnt and Ponta da Madeira at 1.0 mnt, reflecting a broad-based but measured pick-up across Brazil’s main export terminals. On the shipper side, CSN together accounted for 3.3 mnt, while Vale shipped 1.8 mnt, highlighting cautious cargo nominations despite firm underlying supply.

China remained the key destination, importing 2.2 mnt, though long-haul economics continued to face pressure from weak steel margins and price-sensitive buying. As a result, exporters stayed cautious, prioritising shipment timing over volume expansion despite Brazil’s strong export capacity. Brazil’s recovery remained limited as long-haul freight costs continued to influence shipment decisions, keeping cargo releases selective despite strong supply capacity.

Canada’s exports ease on reduced Atlantic demand

Canada’s iron ore exports fell 24.3% w-o-w to 0.97 mnt, reversing part of the previous week’s post-holiday rebound. The decline reflected fewer cargo nominations and softer Atlantic demand, rather than any operational disruptions, with shipment decisions remaining closely linked to freight sentiment.

Port Cartier led loadings with 0.5 mnt, followed by Sept-Iles at 0.4 mnt, indicating steady terminal operations despite lower overall volumes. On the shipper side, AM/NS accounted for 0.5 mnt, while Guinea and Nimba Mines and IOC shipped 0.2 mnt each, reflecting selective cargo releases.

On the destination side, the Netherlands received 0.3 mnt, followed by Spain and Vietnam at 0.2 mnt each. While Atlantic demand remained uneven, strategic interest from buyers such as Indian steelmakers testing Canadian ore supplies highlights Canada’s product quality and diversification potential amid shifting global trade dynamics.

South African shipments retreat after previous week’s spike

South Africa’s iron ore exports declined 21.1% w-o-w to 1.11 mnt, following a sharp rebound in the previous week. The pullback was largely attributed to shipment timing, as fewer cargoes were scheduled after earlier clearances.

Saldanha Bay remained the sole loading port, handling the entire 1.1 mnt, reflecting stable terminal operations despite overall lower weekly volumes. Export flows continued to be driven by cargo scheduling rather than any structural change in demand. On the destination side, China and the Netherlands each imported 0.3 mnt, underlining South Africa’s dependence on selective long-haul demand.

Exports remained highly sensitive to freight economics and buyer caution, limiting any sustained recovery despite stable port operations. At the same time, South Africa’s iron ore export infrastructure remains a key factor, with capacity pressures on the Sishen-Saldanha rail line and ongoing efforts to improve logistics likely to influence export efficiency and freight dynamics in the near term.

Indian exports fall on weak Supramax demand

India’s iron ore shipments dropped 35.3% w-o-w to 0.50 mnt, pressured by muted Supramax demand and ample vessel availability in the Indian Ocean. The decline reflected slower east coast loadings and limited spot cargo interest, as exporters faced weak commodity prices and cautious buying from regional markets.

Port-wise shipments were thin and evenly spread, with Krishnapatnam, Mormugao, Paradip, and Dhamra each handling around 0.1 mnt, highlighting fragmented cargo flows and the absence of any dominant loading centre during the week. India’s iron ore export outlook is also being shaped by ongoing debate over potential export duties on low-grade ore, with industry groups warning that new fiscal measures could disrupt mining activity and weigh on export competitiveness.

China remained the primary destination with 0.2 mnt, underscoring India’s role as a short-haul supplier to Asia. However, strong domestic demand and high price sensitivity among buyers kept export volumes constrained, leaving shipments highly exposed to Supramax freight sentiment.

Chile shipments decline after one-off rebound

Chile’s iron ore exports fell 51.5% w-o-w to 0.20 mnt, reversing the sharp rebound seen in the previous week. The decline reflected the absence of deferred cargoes that had supported earlier volumes, with shipments returning to irregular, timing-driven levels.

Huasco remained the sole active loading port, handling the entire 0.2 mnt, indicating stable port operations but limited cargo availability. Export activity continued to hinge on vessel positioning and cargo readiness rather than sustained demand, while broader regulatory uncertainty in Chile’s mining sector has added caution to investment and logistics planning.

On the destination side, China imported 0.2 mnt, accounting for all Chilean shipments during the week. Iron ore remains a small part of Chile’s mineral trade, leaving export volumes highly sensitive to shipment timing and freight conditions.

Peru exports inch up on steady cargo flow

Peru’s iron ore shipments rose 6.4% w-o-w to 0.55 mnt, supported by steady cargo flow and selective fixing. The marginal increase reflected stable port operations and consistent shipment planning, even as overall market sentiment remained cautious.

San Nicolas led port-wise loadings with 0.5 mnt, while Matarani handled 0.1 mnt, indicating continued concentration of exports through a single major terminal. On the shipper side, Shougang Hierro accounted for 0.5 mnt, underscoring its dominant role in Peru’s iron ore export flows. Peru’s broader mining sector continues to face logistical and investment challenges, with slower foreign investment and infrastructure constraints shaping export efficiencies.

China remained the sole destination, importing 0.5 mnt, highlighting Peru’s heavy reliance on Asian demand. Export volumes stayed closely linked to freight timing rather than any material shift in underlying supply or consumption, keeping weekly movements limited.

Freight sentiment remains mixed

Iron ore freight markets showed mixed signals during the week, with firmer Capesize sentiment supporting selective long-haul fixing, while Supramax segments remained under pressure amid ample vessel availability and muted demand. Improved fixture flow and fresh cargo releases helped stabilise shipment volumes, particularly from major Pacific and Atlantic producers.

However, cautious chartering behaviour, weak steel margins, and uncertain near-term demand continued to cap exporters’ willingness to expand shipments aggressively. As a result, global volumes remained largely stable despite improving Capesize fundamentals.

Outlook

Global iron ore shipments are expected to remain broadly stable in the near term, supported by steady cargo flow from major producers but constrained by cautious buying and mixed freight sentiment. While firmer Capesize conditions may continue to support selective long-haul fixing, weak steel margins and uncertain construction demand in China are likely to limit any sharp recovery in export momentum.

Shipment volatility is expected to persist into early February, with exporters prioritising timing and freight economics over aggressive volume expansion. Short-haul suppliers may see intermittent support from regional demand, but long-haul exporters are likely to remain sensitive to freight swings and buyer caution, keeping global trade flows largely steady.

Leave a Reply