- Australian exports gain 14%, while Indian low-grade struggles

- Market resumes post Chinese New Year holidays, inventories rise

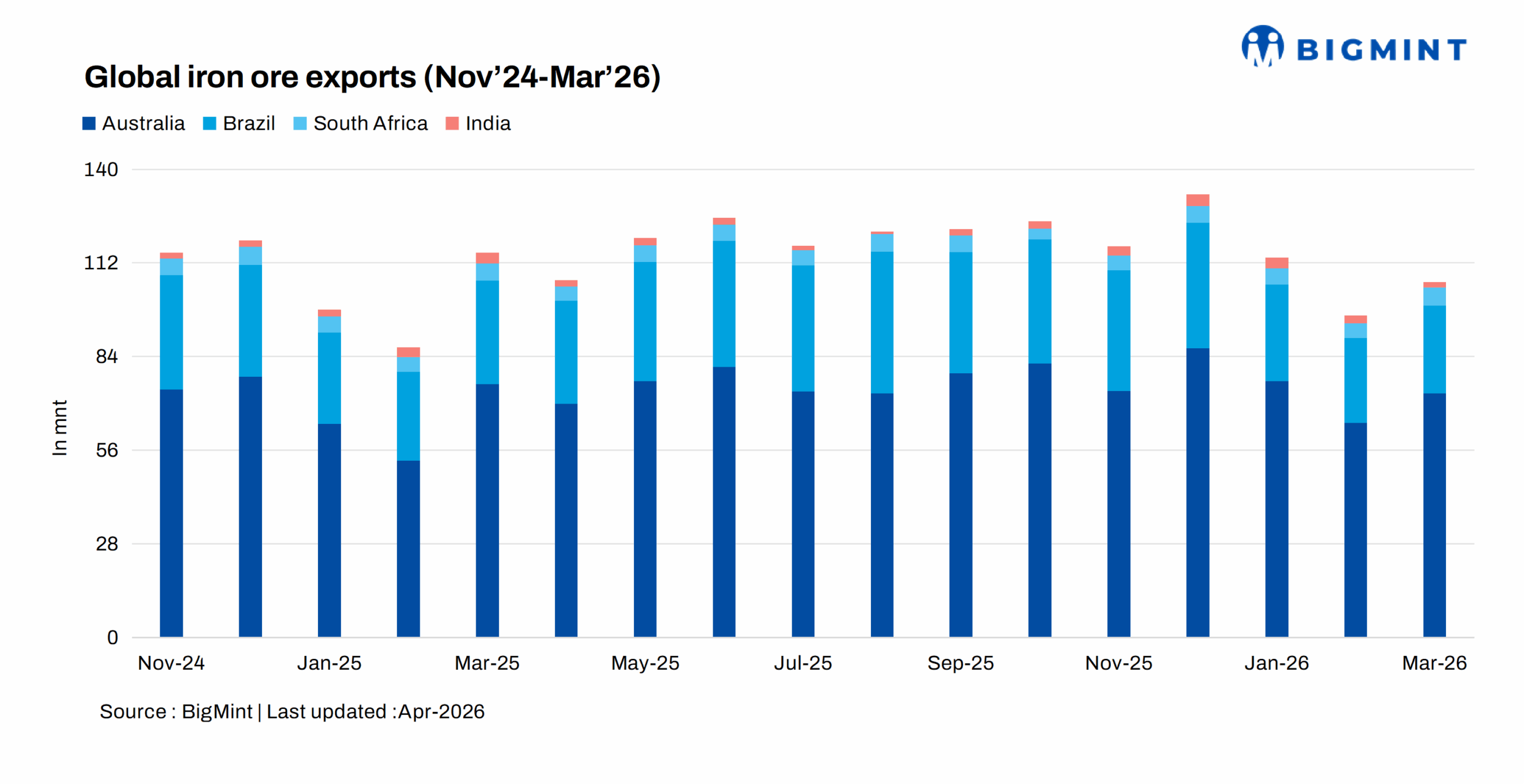

Iron ore (including pellets) exports from key global producers, Australia, Brazil, South Africa, and India, rise m-o-m in March 2026, except India. This was largely driven by enhanced procurement by Chinese buyers, with a consistent effort keeping portside inventories high, followed by Lunar holidays in February which slowed activity. To illustrate, Chinese iron ore and pellet portside inventories rose to 164.46 million tonnes (mnt) in March 2026 (data sourced from 34 major Chinese ports) with consistent buying for fines and pellets.

Australian exports rise by 14% m-o-m

Australia’s iron ore and pellet export shipments stood at 73 million tonnes (mnt) in March 2026, gaining up by 14% against 64.1 mnt in February 2026, according to vessel line-up data compiled by BigMint. However, shipments fell by 4% y-o-y against 75.8 mnt in March 2025.

China remained the top importer, receiving 60.4 mnt, followed by South Korea at 4.6 mnt and Japan at 4.5 mnt. BHP was the leading exporter at 24.2 mnt, trailed by Rio Tinto at 24.3 mnt and FMG at 17.3 mnt.

The rise was largely a seasonal rebound following weather-led disruptions. After a volatile February, impacted by cyclone activity and port closures in the Pilbara, major miners such as Rio Tinto and BHP ramped up shipments to clear backlogs and meet end-of-quarter targets, lifting export volumes.

At the same time, Chinese buyers prioritized higher-grade Australian ore to maintain furnace efficiency amid tightening environmental standards, further supporting shipment flows.

Exports from Brazil inch up by 3% m-o-m

Brazil’s iron ore exports rose by 3% m-o-m to 26.23 mnt in March 2026 against 25.51 mnt in the past month. However, exports still fell short by 15.7% y-o-y from 31.12 mnt in March 2025.

China remained the largest importer, taking in 17.79 mnt, followed by Japan at 1.05 mnt and Malaysia at 0.73 mnt.

Stronger Chinese steel output following the Lunar New Year, along with China maintaining high portside inventories and increased supply from miners, supported a rise in overall traded volumes.

At the same time, improved price realizations driven by a softening global price trend and widening discounts made cargoes more attractive, encouraging healthy buying interest across the market.

South African exports rebound by 25% m-o-m

South Africa’s iron ore exports stood at 5.41 mnt in March 2026, a surge of 25% m-o-m against 4.32 mnt in February, as per vessel line-up data maintained by BigMint. Moreover, export volumes edged up by 5.4% against 5.13 mnt in March 2025.

China remained the leading importer with 1.97 mnt, followed by the Netherlands at 0.78 mnt. March 2026 exports were supported by improved rail and port efficiencies along the Sishen-Saldanha corridor. After logistical constraints in February, efforts to clear backlogs enabled miners like Kumba Iron Ore to ramp up throughput, lifting shipment volumes.

The rebound was further aided by strong demand for South Africa’s premium lumpy ore, preferred for its efficiency. While China remained the top buyer, notable shipments to the Netherlands underscored South Africa’s role in supplying European markets.

India’s exports fall over 30% m-o-m

India’s iron ore and pellet exports fell by 30.5% m-o-m to 1.69 mnt in March 2026 from 2.43 mnt in February. Moreover, iron ore and pellet exports slumped by 46% y-o-y against 3.13 mnt in the same period last year.

China remained the largest importer with 1.2 mnt, followed by Malaysia with 0.28 mnt. Export sentiment remained under pressure, with stiff seaborne competition and high inventories in China keeping exporters cautious. At the same time, rising freight costs and China’s focus on cheaper sourcing options weighed on overall export volumes. Exporters were cautious amid the higher prices of fuels amid recent geopolitical tensions in middle east further keeping the seaborne freight on higher side.

Moreover, the market participants were busy with the fiscal year end closings, along with many Odisha-based miners already utilising their EC limit, which capped material flow into the export market.

Outlook

The April outlook remains mixed, as a likely pickup in demand is being offset by rising geopolitical tensions that have increased freight, fuel, and insurance costs, making seaborne cargoes more expensive. As a result, exporters, particularly from India, are facing margin pressure and scaling back overseas shipments, while buyers remain cautious and price sensitive, keeping global trade flows relatively soft despite post holiday restocking demand.

Leave a Reply