- Australia, Brazil lead gains on stable port activity

- India’s shipments slump amid Chinese pullback

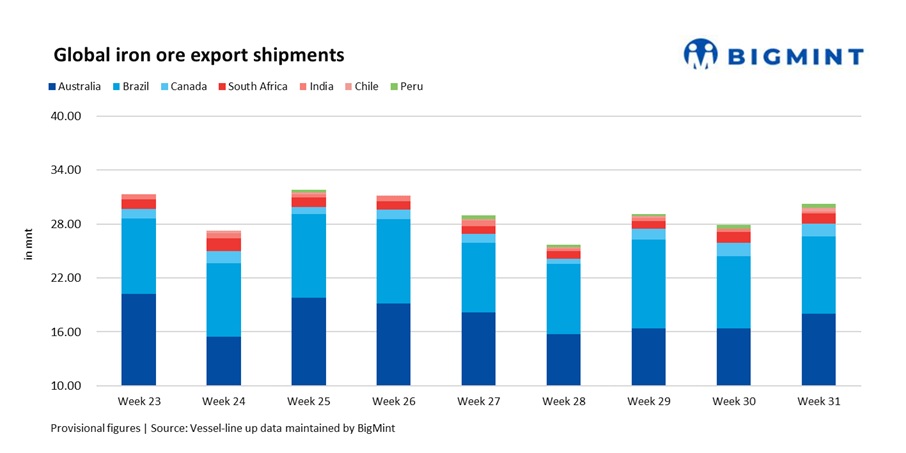

Global seaborne iron ore and pellet exports rose 8.5% week-on-week (w-o-w) in Week 31, 2025 (26 July-1 August) to 30.25 million tonnes (mnt), up from 27.89 mnt in Week 30, according to vessel line-up data from BigMint. The growth was primarily driven by stronger shipments from Australia and Brazil, with consistent support from Canada and a notable rebound in exports from Chile.

However, despite the rise in shipments, Chinese demand remained cautious, weighed down by weak steel mill margins and elevated portside inventories. Buyers continued favouring cost-efficient, mid-grade Australian fines, especially amid slight declines in freight rates and softening benchmark indices.

Australia maintained its leadership position in global exports, shipping 18.02 mnt in Week 31 up nearly 10% w-o-w from 16.41 mnt. This rise reflects stable operational conditions at major ports like Port Hedland and Port Dampier, which continued uninterrupted throughput. Top miners such as Rio Tinto (6.75 mnt), BHP (6.12 mnt), and Fortescue Metals Group (3.81 mnt) remained the key contributors.

China remained the top importer, receiving 15.8 mnt, followed by Japan at 0.8 mnt and South Korea with 0.7 mnt. Chinese mills, despite operating under tight margins, continued to lift mid-grade Australian fines due to their favorable landed cost and consistent availability.

In Brazil, iron ore export volumes improved to 8.63 mnt, in Week 31 compared to 8.01 mnt in Week 30 marking a 7.8% w-o-w increase. Exports benefited from logistical recovery and sustained flows from Vale (4.9 mnt) via port Ponta Da Madeira & port Tubarao.

China remained the largest importer, taking in 3.97 mnt, followed by Malaysia at 0.39 mnt and Oman at 0.38 mnt.

Additionally, the initiation of direct exports from Itaminas’ via Porto Sudeste added momentum, underscoring strategic infrastructure optimization. According to Itaminas’ official website, the company completed its first direct iron ore shipment through the Porto Sudeste terminal in Rio de Janeiro on June 26. The terminal acts as a vital logistics hub, offering direct maritime access to Asia, the Middle East, and Europe.

Canada’s iron ore exports remained stable at 1.42 mnt, marginally lower than the previous week’s 1.47 mnt. However, smoother rail-to-port operations at Sept-Iles and Port Cartier ensured consistent cargo flow.

Canadian exporters like IOC (Iron Ore Company of Canada) continued to serve the Netherlands (0.5 mnt) and China (0.35 mnt), who increasingly sought premium-grade DR (direct-reduction) iron ore for low-emission steelmaking.

South Africa, which had recorded the strongest growth in previous week, Week 30, saw its shipments dip to 1.13 mnt, down from 1.25 mnt.

Although operations at Richards Bay remained efficient, the fall reflects a natural moderation after a surge. China remained the leading importer with 0.65 mnt. Renewed Chinese restocking interest provided some cushion, although volumes were still down w-o-w.

In contrast, India’s iron ore exports declined sharply to 0.22 mnt, a 38% fall from the previous week’s 0.35 mnt.

Indian traders remained on the sidelines as Chinese buyers shifted focus toward more competitively priced Australian and Brazilian fines. In addition, soft global prices and weak spot demand put further pressure on Indian cargoes.

Chile re-entered the export market after a brief pause, posting 0.39 mnt of shipments in Week 31, driven by resumed loading from northern ports.

Peru also saw modest gains, with volumes rising to 0.44 mnt, supported by steady shipments from the Marcona region and moderate demand from Asia.

Dry bulk iron ore freight rates dip down w-o-w on limited fixtures, with subdued activity seen across major routes such as Australia-China and Brazil-China. The slight dip in rates provided marginal relief to Chinese buyers operating under tight steel margins. However, overall market sentiment remained weak amid continued steel production cuts, macroeconomic pressures, and cautious procurement behavior.

Looking ahead, global export volumes may remain elevated in the near term, especially with Australia and Brazil maintaining steady port performance. However, unless Chinese steel margins recover or stimulus measures drive up infrastructure demand, seaborne trade is likely to remain volume-heavy but margin-light.

Leave a Reply