- EU restocking demand instils market positivity

- China policies help in domestic demand revival

- Global demand uptick, seasonal changes to support price uptrend

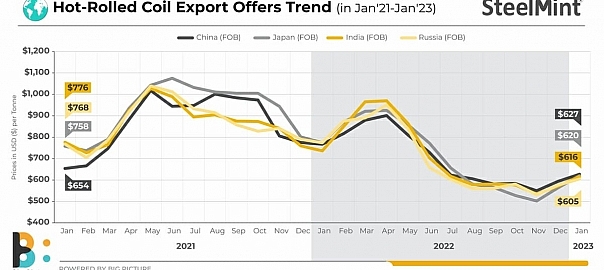

Morning Brief: Global hot rolled coil (HRC) export offers have climbed up in January 2023 to touch six-month highs, shows SteelMint’s data.

FoB prices in China, Japan, Korea and India, the countries which together enjoy around 45% of the seaborne trade, are all nudging levels last seen in July 2022. For instance, China’s current $627/tonne (t) was hovering around $623/t in July. Japan’s $620/t was at $656/t and India’s $616/t ruled at nearabout $617/t six months back.

Overall, these prices, including South Korea’s $650/t, are up by over $50/t FOB m-o-m in January so far.

Global seaborne trade overview

The global seaborne steel export trade fell around 15% y-o-y in 2022 to a little over 288 million tonnes (mnt) from 337 mnt in the preceding year. Globally, the most-traded steel commodity was HRC, which had a share of 15% of total exports, followed by semi-finished at 13%.

The leading exporter in 2022 was undoubtedly China with over 67 mnt, followed by Japan at 28.7 mnt and South Korea with 23 mnt. These three controlled 41% of the seaborne trade last year. India fell back from 7th to 11th position y-o-y in 2022 with 10 mnt.

Factors pulling up HRC export offers

1. Revival in EU demand: It may be recalled that global HRC prices had climbed to record highs with the onset of the Russia-Ukraine war, mainly on account of panic buying from European Union. Thereafter, as EU buyers became well-stocked, demand dried up.

The scenario was aggravated by oil and natural gas supply worries as Russia indulged in energy politics in the face of western sanctions. Oil and natural gas prices spiralled to never-seen before levels, leading to inflation, drop in demand from end-buyers and a subsequent decline in global prices as well. China’s export offers plunged from a peak of $901/t FoB in April 2022 to $550/t in November 2022. Japan’s leapt up to $925/t and then plunged to $502/t and India’s, from $970/t to $534/t, in both months mentioned.

Now, however, the scenario has changed somewhat with governments across the world moving in quickly to tame inflation by hiking interest rates to suck liquidity out of their respective economies.

These measures yielded results. Benchmark WTI crude oil prices, from a historic high of almost $123/barrel and an average closing price of $95/barrel in 2022, have declined. The average closing price in January 2023 is $78/barrel. Gas prices too have dropped off. As per the Henry Hub Natural Gas Spot chart, the average closing price in January has dropped to $3.50 from $6.45 in 2022.

With energy prices dropping, some restocking demand has emerged from Europe. Interest rates too have stabilized and end-users are returning to the market, imbued with positivity.

2. Chinese revival measures: China had been badly bruised by the double whammy of its real estate market crash and Covid surge. However, with the government moving in with measures to revitalize the economy, along with easing of Covid protocols, it is expected that demand in this country will revive too. Even if Chinese mills and traders concentrate more on domestic demand, they set price directions for global markets.

3. Rising raw material prices: Cost push is also raising prices. Australia’s Fe62% fines imported into China, CNF Rizhao Port, are up from $82/t three months ago to $127/t currently. Brazilian Fe62% fines, CNF Qingdao Port, have moved up to $119/t from $84/t in the same period.

Premium HCC coking coal exported from Hay Point, Australia, has crept up from $287/t a month ago to $325/t.

In India, both NMDC and OMC have raised their iron ore prices. The Odisha fines index recently rose to a 7-month high.

Outlook

Global HRC prices may sustain the uptrend in the short to medium term as winter would soon be weakening in many parts of the world after February and the season will support resumption in construction activities.

That apart, the threat of Covid has perceptibly lessened globally, which is further helping to normalize steel demand patterns.

Leave a Reply