- Australian coking coal shipments drop 5% in 9MCY’25

- India records 5% jump in imports, China sees 6% drop

- Supplies may come under serious pressure if prices soften further

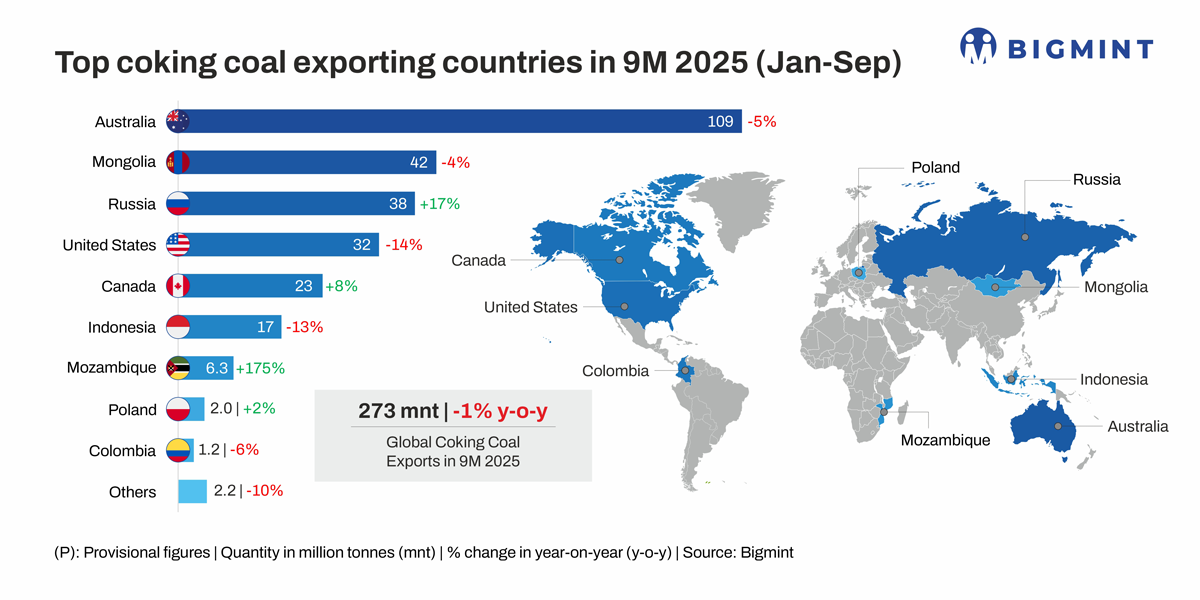

Morning Brief: Global coking coal export volume shrunk marginally in January-September 2025 (9MCY’25) by around 1.4% y-o-y to approximately 273 million tonnes (mnt) compared to 277 mnt in the same period last year, as per provisional data maintained with BigMint.

Geopolitical tensions, US import tariffs, global economic slowdown, and declining steel production weigh on coking coal trade flows and demand. As per WSA, global crude steel production dropped 1.6% on the year to 1.37 billion tonnes (bnt) in 9MCY’25, with all the major countries and regions witnessing a decline in production except India and the US.

Australia remained by far the largest exporter of coking coal, with a share of nearly 40% of global exports and the primary source of premium hard coal; however, total exports by Down Under fell y-o-y in 9MCY’25 on lower shipments to India, Japan and China.

Exports in 2024 had reached 375 mnt, with Australia’s share at 45% and the respective shares of the US, Mongolia and Russia stood at 15%, 14% and 11%. However, Mongolia overtook the US as the second-largest exporter of coking coal in 9MCY’25 despite a marginal drop in overall volumes.

Highlights of trade dynamics in 9MCY’25

Australia’s export share shrinks: Australian exports of the key steelmaking ingredient fell nearly 5% y-o-y on soft demand by the Asian majors as well as weather disruptions. Significant wet weather impacts in the March quarter and operational disruptions at Moranbah North and Appin weighed on export volumes in the June-September quarter. Companies are focusing on unit cost minimisation while maintaining output.

That apart, new steelmaking coal projects in Australia face increasing challenges. Increased costs, stricter regulations and long approval timelines are limiting the pace of development. According to the Minerals Council of Australia, approval timelines have grown by 60% since 2019.

Moreover, the royalty for mines has increased notably since July 2022, reflecting changes to Queensland’s progressive coal royalty regime. Queensland accounts for roughly 90% of Australian exports.

India records 5% jump in imports: The only country to record an increase in imports was India, with total volumes reaching around 46.6 mnt, an increase of nearly 5% y-o-y. India’s crude steel production rose over 10% y-o-y in 9MCY’25. However, Indian BF-based producers are diversifying sources of imports, especially with Russia offering extremely competitive prices due to sanctions, and reducing reliance on Australian PHCC. Some mills are also investing in overseas coking coal mines to secure supplies of this critical resource.

Sources indicate that sourcing different grades and experimenting with newer coal blends are essential to reduce dependency on PHCC. Mills are experimenting with semi-hard, mid-to low-volatile coking coal in different blends to determine their impact on hot metal quality and composition.

That this trend may really have accelerated is borne out by the fact that imports from Australia dropped 4% y-o-y in 9MCY’25 despite overall imports increasing by 5%.

Chinese coking coal demand edges down: In 9MCY’25, Chinese coking coal imports were approximately 83.6 mnt, a decrease of 6% y-o-y, according to the General Administration of Customs. A slight increase in domestic coking coal production and steady pig iron output led to reduced imports. Changes in demand tend to have an outsized impact on Chinese imports as China produces over 80% of its own metallurgical coal needs.

Slowing steel demand has led some steelmakers to draw on inventories rather than import coal, in anticipation of mandated steel output cuts and lower coal prices. Lower steel production also impacted imports from Mongolia – the mainstay of Chinese coking coal importers.

Notably, strong global steel exports, safety-related mine inspections and periodic interventions by the National Energy Administration to check overproduction by some miners may create temporary supply concerns in the Chinese market and lead to higher imports at times. However, overall demand remains dim.

US exports face uncertain future: US exports of coking coal fell by 14% y-o-y as producers faced pressure in a weak price environment, with a significant proportion of mines producing at breakeven cash costs or below. US coal has a higher cost base when factoring freight costs to East Asia than other regions.

China’s reciprocal tariffs on US coal exports weighed on shipments. Some miners resorted to supply rationalisation by idling of high costs mines. These factors pressured exports.

Lower steel production, US tariffs hit Asian majors: Crude steel production in Japan and South Korea, leading coking coal importers, dropped 4.5% and 3.4% respectively in 9MCY’25, which explains lower imports by these countries. The impact of US tariffs on the advanced Asian economies has been lethal, especially in terms of automobile production and exports. This has had a direct bearing on steel production and coking coal demand in these export-dependent economies.

Russia, Canada, Mozambique ramp up exports: Russia increased exports by approximately 16% y-o-y to 38 mnt despite global headwinds, as trade ties with India and China remained strong. However, the price and profit outlook of Russian miners deteriorated considerably under the weight of sanctions. In a weak pricing environment, most Russian miners will be rendered uncompetitive.

On the other hand, Canadian coking coal exports increased by over 7% y-o-y during the review period due to higher exports to China amid US tariffs. Canadian coal is prized for its premium quality. Exports from Mozambique, however, increased solely due to higher shipments to India, with major Indian steel producers acquiring stakes in coking coal mines in the African country.

Outlook

The Russia-Ukraine war and geopolitical crises had triggered massive volatility in the coal and energy sectors in CY’22-23 and apprehensions of continued volatility has instilled an acute price sensitivity in the coking coal market. The sustained weakening of prices since January 2024 amid decline in global steel production and reciprocal tariffs and sanctions is bound to affect supplies.

So much so that the US Senate had to pass an amendment to implement a production tax credit of 2.5% for coking coal and temporarily lower the federal royalty rate for coal from 12.5% to 7% to sustain production and exports. Again, the Russian government has postponed mineral extraction tax payments and insurance obligations until at least December 2025 and targeted financial support, as well as resumption of rail tariff discounts are among other support measures being mulled.

Even some Australian miners have reportedly come under financial stress, with Australian government sources acknowledging that a price below $170/t FOB for a prolonged period poses downside risks to production.

Global prices have remained stable despite a declining global steel outlook due precisely because supply concerns are recurrent in the somewhat niche coking coal market. On the other hand, the delay in transition to less-emission intensive steelmaking methods such as the EAF in the EU as well as in China, and the correspondingly higher profitability of BF-based steelmaking compared to other routes in these key steel-producing regions, means that coking coal demand will not decline as precipitously as expected in the near term.

This may create sustained supply concerns in the global market and make the going tougher for import-reliant Indian steel companies.

Leave a Reply