- Indonesia top supplier with over 560 mnt of coal exports

- Russian exports fall due to sanctions, limited rail capacity

- Coal still preferred choice due to energy inflation, sudden supply shocks

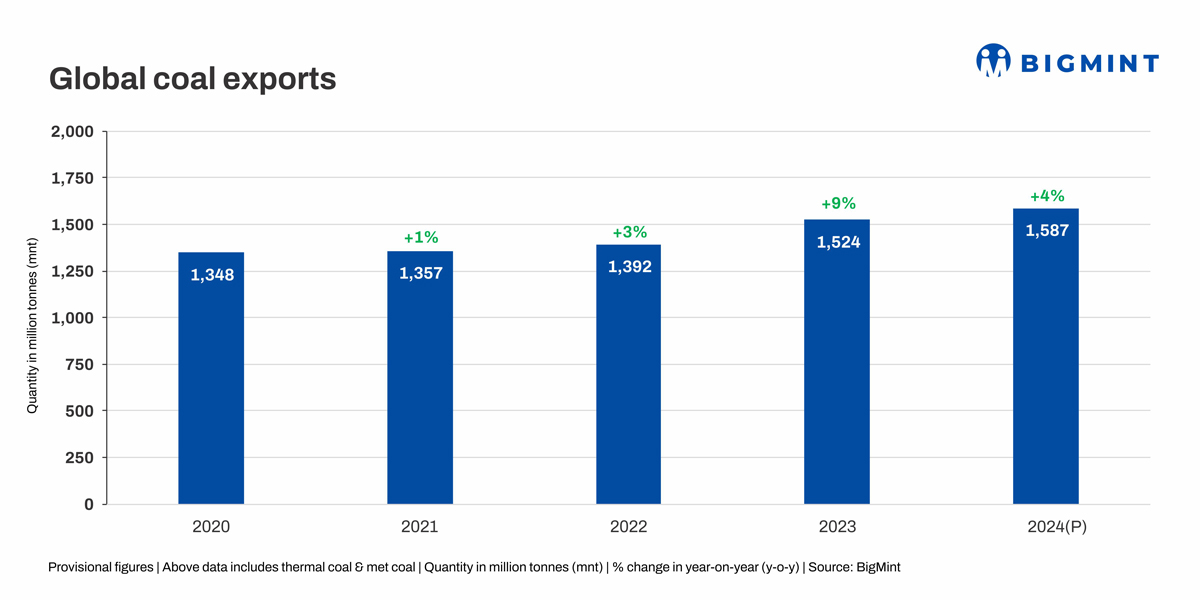

Morning Brief: Amid global energy inflation and intensifying geopolitical crises in different parts of the world, the reliance on coal has actually grown as a cost-competitive and reliable source of energy. Provisional data available with BigMint show that global coal exports (comprising both thermal and metallurgical) in calendar year 2024 (CY’24) posted a growth of over 4% y-o-y to reach 1,587 million tonnes (mnt) – 1.58 bnt – from 1,524 mnt in CY’23.

Higher energy consumption in the post COVID period was the direct offshoot of a global economic rebound which boosted the demand for coal. Coupled with this, trade embargoes and sanctions, as well as soaring energy prices in major economies, directly contributed to the increased reliance on coal to meet energy security goals.

One sure sign of increasing reliance is that global coal exports have increased 15% since the post-pandemic period, as per data.

Major coal exporting countries

Indonesia remains the top global exporter of coal, with total shipments of around 563 mnt in CY’24, a growth of over 7% y-o-y from 524 mnt in CY’23. Due to higher domestic coal production, Indonesia has been able to raise coal exports by nearly 200 mnt since 2022.

Australia emerged as the second-largest coal exporter globally, with total shipments of around 360 mnt in the year gone by. Incidentally, Australian coal shipments have declined marginally from a level of 367 mnt in 2020.

Russia and the US were the other major exporters of coal, with total shipments of around 199 mnt and 138 mnt, respectively, in CY’24. While Russian exports declined around 5% y-o-y, the US posted a gain of over 6% in total coal exports.

Interestingly, landlocked Mongolia raised exports by over 20% in CY’24, while major exporter South Africa saw volumes decreasing by around 4%.

Market dynamics in key exporting nations

Indonesia: Indonesia produced a record 835 mnt of coal in CY’24, nearly 18% above its target of 710 mnt, as per data from the country’s Energy and Mineral Resources Ministry. The country also increased coal production by more than 8% y-o-y from 771 mnt in CY’23. Indonesia also far exceeded its target of 490 mnt of coal exports in CY’24, thanks to increased demand from China and India. Due to sustained growth in domestic production, the country has been able to raise exports through the years despite higher domestic obligation of miners.

Australia: About 75% of Australia’s thermal coal production of roughly 200 mnt in CY’24, and nearly all of its metallurgical coal output of approximately 160 mnt, were exported, as per Australian government data. Australia’s share in total global exports is around 23%, although its share of global met coal exports is much higher at around 46%. On the other hand, Australia accounts for roughly 20% of global trade in thermal coal.

Russia: Russia’s coal exports decreased by over 5% y-o-y to 199 mnt. Russian exports have faced many challenges, including expanding sanctions and reduced access to rail capacity. However, higher-value metallurgical coal is prioritised during rail shortages. China’s imports from Russia also fell as expanded sanctions took effect. Russian production declined, with the largest coal producing region, Kuzbass reducing output due to sanctions, limited rail availability, and increasing costs. However, with China and India continuing to absorb the vast majority, Russian met coal exports actually increased as it continues to trade at a discount due to trade partner limitations.

Mongolia: Mongolian coal exports edged up by over 20% in CY’24 as the country’s coal production rose by roughly 24% y-o-y, as per data. Mongolian exports have been supported by China’s steady steel output and reduced Chinese domestic coal production (linked to tightened mine inspections and safety regulations). Other factors supporting higher exports are the increase in regulatory storage capacity of Ganqimaodu Port and the daily customs clearance volume.

Outlook

Despite record breaking renewables rollouts and increased use of nuclear and gas, unexpected spikes in demand and weather-related shocks to supply have become an ongoing feature of thermal coal markets. These shocks have sustained demand in 2024, and this pattern could continue, as per Australian government forecasts.

While Australian exports may remain stable, Indonesia may see exports declining in the coming years due to higher domestic energy demand and the onus on miners to fulfill domestic supply obligations. Sanctions, infrastructure bottlenecks, and rising costs are expected to impact imports from Russia.

However, according to the International Energy Agency (IEA), global coal trade is expected to experience a reversal of trend, initiated by China and India. In the case of China, flat coal demand with healthy domestic production is set to lower the demand for imports. The imposition of a 15% tariff on US coal imports, on the other hand, may lead to marked trade shifts.

In India the ongoing push for domestic thermal coal production is expected to outpace the growth in demand. While other countries in Southeast Asia are estimated to see growing demand for thermal coal imports, this should be balanced by plans to phase out coal-fired power generation in many Western countries causing their imports to decrease.

In the met coal segment, the outlook for China’s metallurgical coal demand is uncertain given the decline in domestic steel consumption and recent anti-dumping investigations against Chinese steel exports. However, demand from India and the ASEAN is set to increase going forward due to significant expansion in blast furnace steelmaking capacity.

Leave a Reply