- Exports to Japan fall 16%, China drop 34% m-o-m

- DBCT Port sees sharpest drop of 59% m-o-m

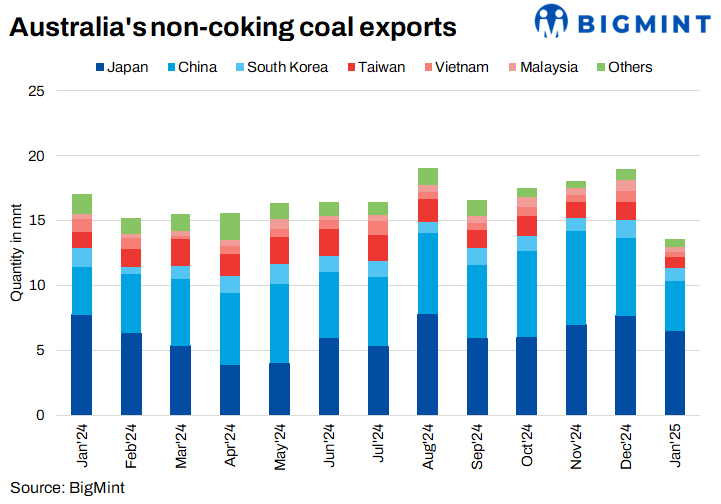

Australia’s non-coking coal exports dropped significantly by 25% in January 2025, to 14.28 million tonnes (mnt), compared to 18.97 mnt in December 2024. This represents a 16% y-o-y decrease from the 17.05 mnt exported in January 2024. The sharp decline highlights reduced demand from key Asian markets, particularly Southeast Asia.

Slower demand across major Asian markets

The slowdown in exports was most noticeable across major Asian markets. Shipments to Japan fell by 16% m-o-m to 6.47 mnt, while exports to China saw a marked 34% m-o-m drop to 3.91 mnt. Additionally, exports to South Korea dropped by 28% m-o-m to 1.01 mnt and to Taiwan decreased by 43% m-o-m to 0.80 mnt.

Southeast Asia showed mixed trends, with Vietnam’s and Malaysia’s imports from Australia both plunging by 54% m-o-m to 0.40 mnt and 0.39 mnt, respectively. However, Thailand’s volumes recorded a notable surge of 97% m-o-m to 0.28 mnt, suggesting that there are some pockets of stronger demand in Asia.

Port-specific export performance

The decline in coal shipments in January 2025 was reflected across Australia’s key export terminals. Dalrymple Bay Coal Terminal (DBCT) recorded a 59% m-o-m drop, with exports at 0.59 mnt, while Gladstone Port saw a 8% decrease to 1.34 mnt. Port Kembla experienced the sharpest drop of 67% m-o-m to 0.1 mnt. However, Abbot Point’s exports increased by 43% m-o-m to 1.62 mnt, and Brisbane port recorded a 23% increase to 0.42 mnt.

Outlook

The outlook for Australia’s non-coking coal exports remains subdued in early 2025, driven by weak demand from key Asian markets. While seasonal factors may contribute, long-term shifts in demand appear likely. Exporters may need to focus on emerging markets and adapt their strategies, while a recovery in demand from China, Japan, and Southeast Asia will be crucial for future performance.

Leave a Reply