- Australia, South Africa lead export rebound amid improved cargo execution

- Firmer freight sentiment supports shipments despite cautious demand

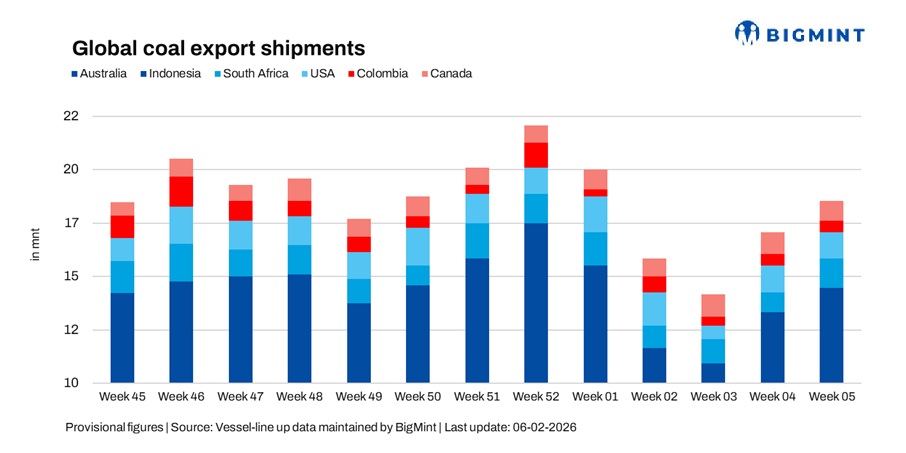

Global seaborne coal exports increased by around 8.5% w-o-w to 18.18 million tonnes (mnt) in the week ended 30 January, from 16.76 mnt in the previous week, as per vessel line-up data. The rise marked a continuation of stronger shipment momentum, supported by improved cargo execution and a rebound in key export origins.

The weekly increase was primarily driven by a sharp recovery in shipments from Australia and South Africa, along with marginal gains from the US, which outweighed declines from Indonesia, Colombia, and Canada. Export activity remained largely schedule-driven, with loading programmes reflecting a mix of improved operational throughput and selective demand from key Asian buyers.

While volumes rose overall, exporters continued to maintain disciplined shipment flows, indicating that the recovery was supported more by planned cargo movement and timing factors rather than a broad-based surge in global coal demand.

Country-wise trends

Australian coal shipments surge

Australia’s coal exports rose 22.4% w-o-w to 7.29 mnt in week 05 from 5.95 mnt in week 04, supported by stronger cargo execution and smoother port operations. Shipment activity was led by Newcastle (2.87 mnt), followed by Gladstone (1.62 mnt) and DBCT (1.32 mnt).

On the supply side, BHP led shipments at 0.56 mnt, followed by Glencore (0.47 mnt). Japan remained the top destination at 2.58 mnt, followed by China (0.67 mnt) and South Korea (0.65 mnt), reflecting steady northeast Asian demand. The rise in Australian coal exports comes against a backdrop of a shrinking trade surplus with China, where weaker import demand for commodities including coal has narrowed overall trade balances and underscored soft Chinese buying conditions.

On the commercial front, miner stocks such as Yancoal have also seen strong gains on domestic markets, supported by relatively firmer sentiment around Australian coal cargo demand.

Indonesian exports ease after strong prior week

Indonesia’s coal exports slipped 3.3% w-o-w to 7 mnt in week 05 from 7.22 mnt in week 04, reflecting a mild correction after last week’s sharp surge. Shipment activity was led by Taboneo (1.76 mnt) and Samarinda (1.12 mnt), followed by Balikpapan (0.56 mnt) and Muara Pantai (0.56 mnt).

On the supply side, Adaro Indonesia led shipments at 0.97 mnt, followed by Bayan Resources (0.56 mnt). On the demand front, India emerged as the largest destination at 1.75 mnt, followed by China (1.53 mnt) and Philippines (0.68 mnt), indicating steady regional offtake despite cautious buying sentiment. The slight weekly easing in Indonesian shipments comes amid ongoing policy uncertainty, as miners have temporarily halted spot exports following proposed production quota cuts for 2026, a move that has weighed on export availability and market timing.

South African exports rebound sharply

South Africa’s coal exports rose 48.2% w-o-w to 1.33 mnt in week 05 from 0.90 mnt in week 04, supported by improved cargo execution and the return of larger scheduled shipments. Export activity was entirely concentrated at Richards Bay (1.33 mnt), reflecting stronger terminal throughput during the week.

On the demand side, India remained the largest destination at 0.7 mnt, highlighting continued buying interest, although procurement remained largely selective and timing-driven. The rebound in South African coal exports coincides with a broader improvement in rail performance, which helped Richards Bay achieve its highest annual export throughput in four years in 2025, although ongoing logistical constraints continue to cap overall export capacity.

Colombian shipments decline

Colombia’s coal exports fell 9.0% w-o-w to 0.48 mnt in week 05 from 0.53 mnt in week 04, reflecting weaker cargo execution and limited shipment availability. Export activity was led by Puerto Nuevo (0.29 mnt), indicating that volumes remained concentrated around key terminals. On the supply side, Prodeco Group emerged as the leading shipper at 0.35 mnt, highlighting the schedule-driven nature of exports.

On the demand front, shipments were spread across smaller destinations, with Mauritius (0.08 mnt), Morocco (0.08 mnt), and The Netherlands (0.08 mnt) emerging as the top buyers, reflecting fragmented Atlantic Basin demand. Colombia’s export growth was further tempered by ongoing infrastructure and logistics delays, as rail and port expansion plans aimed at boosting throughput have been postponed, while subdued Atlantic Basin coal demand continues to cap broader shipment momentum.

US exports edge higher

US coal exports rose marginally by 3% w-o-w to 1.22 mnt in week 05 from 1.18 mnt in week 04, supported by steady shipment execution. Export activity was led by Norfolk (0.37 mnt), followed by Baltimore (0.32 mnt) and Mobile (0.28 mnt), reflecting stable port operations.

On the demand side, India emerged as the largest destination at 0.26 mnt, followed by Turkey (0.17 mnt), indicating selective buying interest across both Asian and Atlantic markets. Despite the rise, exports remained dependent on sporadic cargo programmes, keeping overall momentum limited. The uptick also comes amid improving trade sentiment between the US and India, as ongoing discussions around deeper bilateral trade cooperation may support stronger energy flows and diversify India’s sourcing strategy.

Canadian exports weaken

Canada’s coal exports fell 9.5% w-o-w to 0.9 mnt in week 05 from 0.97 mnt in week 04, reflecting softer cargo scheduling and reduced weekly throughput. Shipment activity was led by Roberts Bank (0.61 mnt), followed by Prince Rupert (0.19 mnt) and Vancouver (0.08 mnt), indicating lower overall loading volumes.

On the supply side, Elk Valley Resources was the leading shipper at 0.08 mnt. On the demand front, Japan remained the largest destination at 0.45 mnt, highlighting continued northeast Asian offtake despite cautious buying sentiment. Canadian coal export momentum also comes amid growing strategic interest from major Asian buyers, with India’s state-run NMDC actively exploring Canadian coal reserves to support its steel production capacity.

Higher bunkers support freights, but gains capped

Coal freight markets to India remained firmer during the week, supported by a sharp rise in bunker prices amid heightened geopolitical tensions and an improvement in dry bulk sentiment ahead of the Chinese New Year. Rising voyage costs encouraged owners to seek higher freight levels, strengthening market tone across key coal routes into India.

However, gains remained capped as charterers largely resisted higher offers, keeping negotiations cautious and widening the bid-offer gap. While the firmer Baltic market supported exporters in executing scheduled cargoes, ample tonnage availability in the Indian Ocean continued to limit aggressive rate upside and kept fixing activity measured.

Outlook

Global coal exports are expected to remain firm but volatile in the near term, with shipment momentum continuing to depend largely on cargo scheduling and operational execution rather than a broad-based demand recovery. Australian exports may stay supported on improved port performance, while South African volumes could remain uneven as logistics constraints continue to influence throughput.

Indonesian shipments are likely to remain stable with a softer bias amid ongoing policy uncertainty around production quota cuts, which may limit spot cargo availability. Freight rates into India are expected to remain range-bound, supported by firmer bunker prices and improved dry bulk sentiment, although ample tonnage availability and cautious chartering are likely to cap any sharp upside.

Leave a Reply