- Improved smelter ops, firm demand boost global output

- Oceania records highest regional growth at 4.5% m-o-m

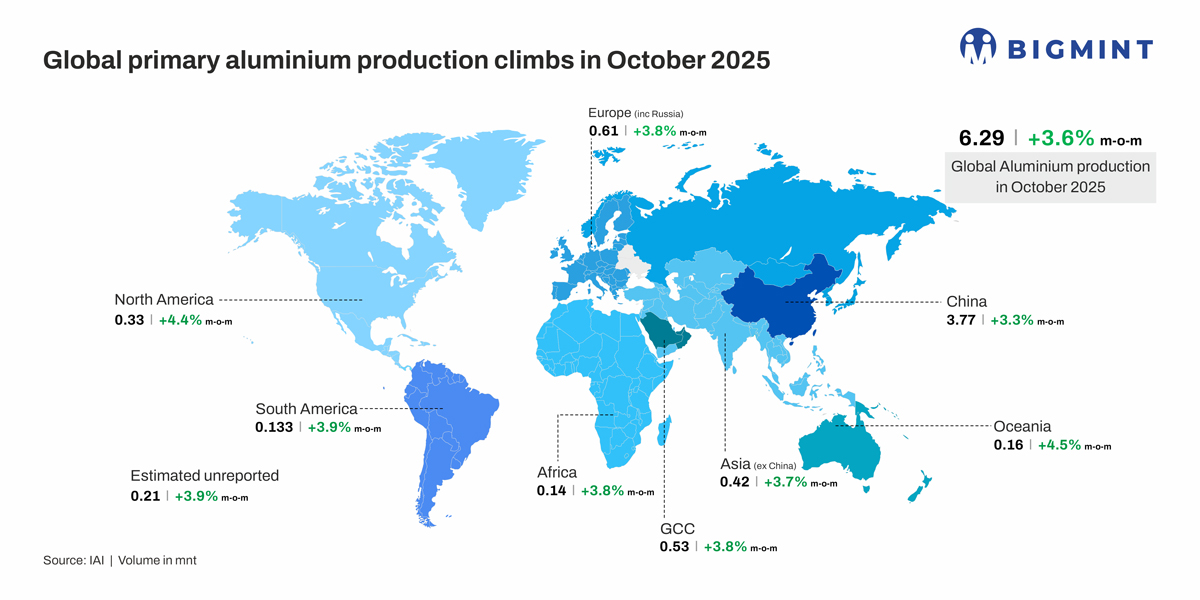

Global primary aluminium production rose 3.6% to 6.29 million tonnes (mnt) in October 2025 from 6.08 mnt in September. The m-o-m rebound reflects improved operating rates across key producing regions, following earlier slowdowns and production adjustments in September. Notably, aluminium production was down by 3% m-o-m in September.

On a y-o-y basis, output in October saw a modest rise of 0.58% compared to 6.26 mnt in October 2024. The slight annual gain indicates broadly stable global supply conditions, with cumulative production holding firm despite periodic fluctuations in market demand and regional smelter performance.

Country-wise breakdown

China, the largest producer, saw output rise 3.3% m-o-m to 3.77 mnt in October, reaffirming its dominant position in global supply. Africa recorded a 3.8% m-o-m increase to 0.14 mnt, while South America’s production grew 3.9% m-o-m to 0.133 mnt.

North American output improved 4.4% m-o-m to 0.33 mnt, and Asia (excluding China) posted a 3.7% m-o-m rise to 0.42 mnt. Europe (including Russia) registered a 3.8% increase to 0.61 mnt, while Oceania recorded the highest regional growth at 4.5% m-o-m, maintaining output at 0.16 mnt. The GCC region also reported a 3.8% m-o-m uptick to 0.53 mnt, and estimated unreported production rose 3.9% m-o-m to 0.21 mnt.

Overall, global aluminium production in October 2025 showed consistent m-o-m growth across all major regions, reflecting improved smelter operations and stabilising market conditions.

Improved smelter ops, firm demand boost global aluminium output

Global primary aluminium production rose across all major regions in October 2025, supported by improved smelter operations, stabilised raw material supply, and firmer demand conditions. China witnessed a 3.3% m-o-m uptick, driven by better alumina availability as metallurgical-grade alumina production increased during the month.

Stronger operating rates, improving demand, and higher aluminium prices also supported China’s output. Ongoing overseas smelting investments by Chinese companies, including capacity additions in Southeast Asia, further contributed to supply stability.

North America also recorded a strong 4.4% m-o-m rise, helped by smelter restarts and new capacity investments. The restart of around 50,000 t of previously idled US capacity boosted regional production, even as smelters continued to face high electricity costs. Gradual revival efforts and supportive industrial policies enabled higher operational utilisation during the period.

The 3.8% m-o-m growth from the GCC region was supported by reliable energy availability and efficient smelter performance.

Overall, October 2025 marked a coordinated global recovery, with every major producing region reporting higher output. Improved alumina supply led to production resumptions after earlier maintenance and cost-related shutdowns, while stronger aluminium prices and stable downstream demand from transport, construction, packaging, and clean energy sectors all contributed to the broad-based rise. This unified increase signals a stabilising global aluminium industry heading into late 2025.

Outlook

Global aluminium output is likely to stay firm in the near term, supported by stable alumina supply, steady smelter utilisation, and healthy demand from transport, construction and clean-energy sectors. With recent capacity restarts and improved operating conditions across major regions, production is expected to remain on a mild upward trend as the industry moves into early 2026.

Leave a Reply