- Smelter activity rebounds after June maintenance cuts

- China’s aluminium imports surge on strong demand

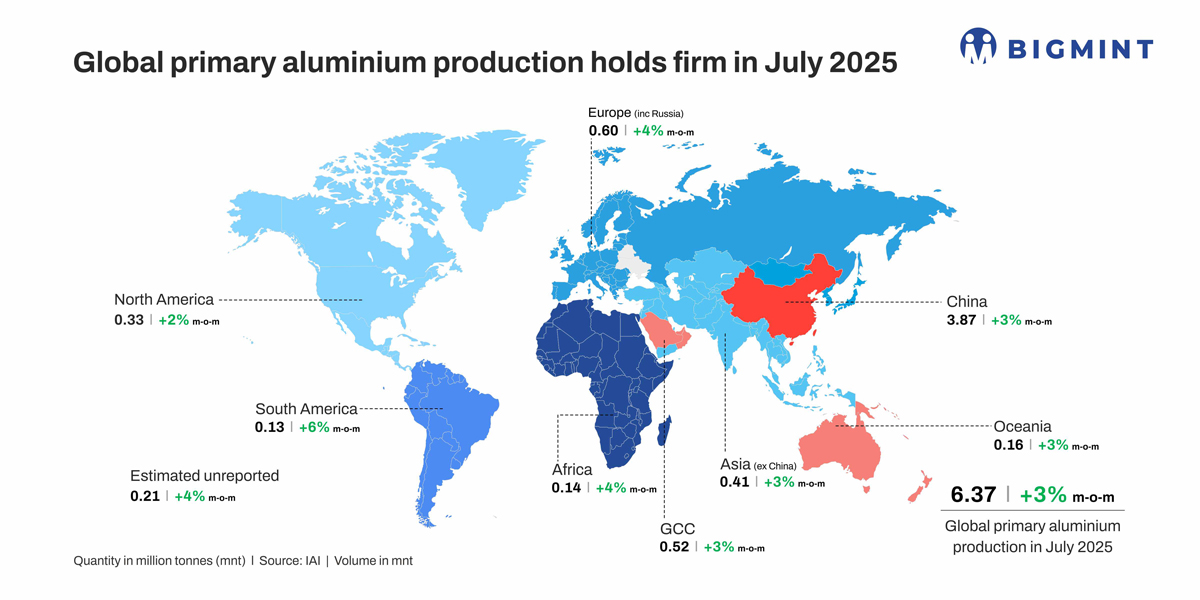

Global primary aluminium production rose to 6.37 mnt in July 2025, up 3% m-o-m from 6.17 mnt in June, according to the International Aluminium Institute (IAI). The rise highlights a consistent recovery trend, supported by higher smelter output across all major producing regions. On a y-o-y basis, output was also higher than 6.32 mnt in July 2024, registering a 0.8% increase y-o-y, underscoring steady growth in global supply.

Global aluminium output rises in July

The rise was mainly supported by a seasonal rebound in smelter activity, as operations typically recover in July following scheduled maintenance and reduced output in June.

In addition, higher LME aluminium prices in recent months incentivised producers to boost operating rates, making output more profitable. The increase was further aided by greater alumina availability, particularly in China, which helped ease raw material constraints and improve smelter utilisation.

Together, these factors contributed to a broad-based recovery across major producing regions, reflecting both market-driven incentives and supply-side improvements.

Country-wise breakdown

China maintained its dominance with 3.87 mnt in July 2025, up 3% from June and accounting for more than half of global supply. South America emerged as the fastest-growing region, producing 0.13 mnt, up 6% m-o-m. Africa and Europe (including Russia) also reported solid gains of 4% each, with output at 0.14 mnt and 0.59 mnt, respectively.

Elsewhere, North America registered a modest 2% rise to 0.33 mnt, while Asia (excluding China), Oceania, and the Gulf Cooperation Council (GCC) each expanded by 3%, producing 0.41 mnt, 0.15 mnt, and 0.52 mnt, respectively. Additionally, unreported estimates stood at 0.21 mnt, up 4% from the previous month.

Overall, the July data reflects broad-based production growth across all regions, with South America showing the strongest momentum, while China remained the dominant contributor to global output.

China boosts aluminium and raw material trade in July

China’s aluminium imports surged in July 2025, reflecting strong demand from construction, transportation, and allied industries amid a capped production capacity of 45 mnt. Imports of unwrought aluminium and products rose 38.2% y-o-y to 360,000 t. This pushed cumulative inflows for January-July to 2.33 mnt, up 1.5% y-o-y.

On the production side, China’s aluminium output grew 1.05% y-o-y and 3.11% m-o-m in July, supported by new Phase II replacement capacity in Shandong–Yunnan. However, alloy output weakened due to subdued end-user demand.

Total aluminium capacity reached 45.69 mnt, with 43.9 mnt operational by end-July, aided by commissioning of replacement projects and resumed output in Chongqing.

China also strengthened its raw material security. Bauxite imports jumped 34.2% y-o-y to 20.06 mnt in July, with cumulative inflows for the first seven months hitting 123.26 mnt, up 33.7% y-o-y. Meanwhile, alumina exports climbed 56.4% y-o-y to 230,000 t in July, taking January-July shipments to 1.57 mnt, a sharp 64.3% increase y-o-y.

Outlook

Looking ahead, global aluminium supply is expected to remain steady through the remainder of 2025, supported by sustained smelter utilisation and easing raw material availability. China’s strong aluminium and bauxite imports signal firm demand despite capped capacity, while rising LME prices should keep smelters incentivised worldwide.

Overall, while supply is expected to stay resilient and diversified, downstream demand fluctuations and macroeconomic uncertainties could temper the pace of recovery, leaving aluminium markets sensitive to both price signals and regional policy interventions.

Leave a Reply