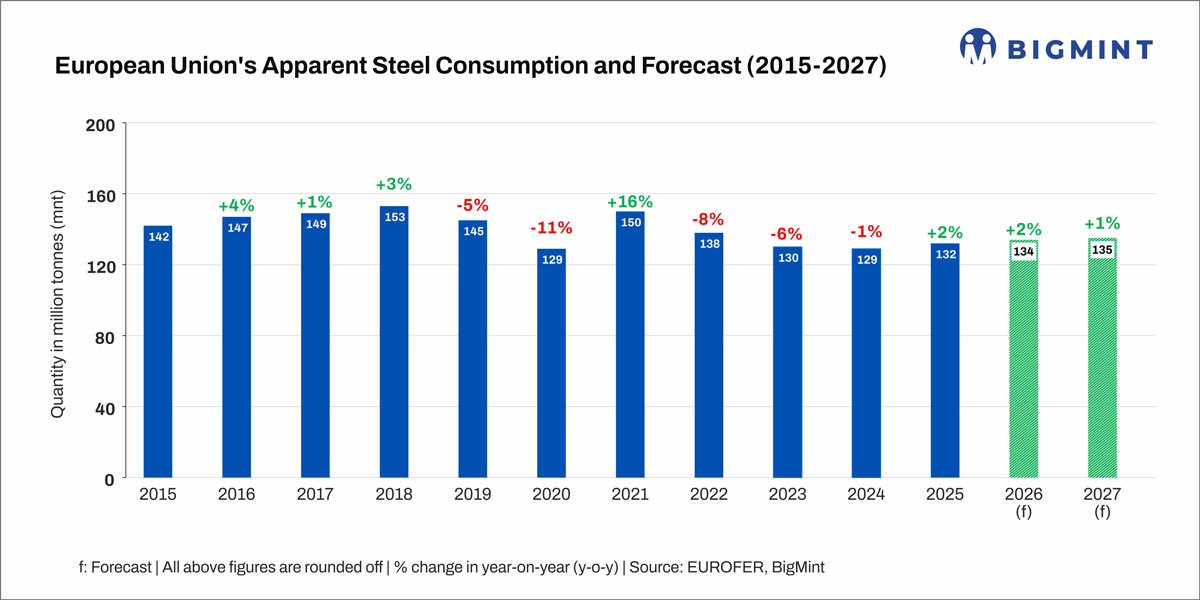

- Apparent consumption to rise 2% in CY’25 after 3-year contraction

- Low base effect, rather than real demand recovery, drives slight growth

- Imports surge 14% y-o-y, market penetration reaches record high in Q3

Morning Brief: The EU’s crude steel production fell 3% y-o-y to a historic low of 125.8 million tonnes (mnt) in CY’25, as per EUROFER’s latest Economic and Steel Market Outlook 2026-2027, First Quarter Report. Pressured by elevated imports, weak consumer confidence, and trade tensions, the steel market down cycle continued, though some signs of recovery emerged.

Notably, a slight improvement in apparent steel consumption took place in CY’25, projected at 2.4%. This was driven by stronger construction activity and a robust government-supported infrastructure pipeline.

Steel demand revives but remains below pre-pandemic levels

Following three consecutive years of contraction, apparent steel consumption climbed higher in CY’25, triggered by a low base effect, an improving industrial outlook, and a stronger-than expected demand in some national markets.

These offset the negative impact of the US’s import tariffs and other geopolitical tensions, the continued Ukraine-Russia war, and uncertainty regarding manufacturing output.

EUROFER has also forecast a 1.3% y-o-y increase in apparent steel demand in CY’26, again stemming from a low base effect rather than a recovery in demand. Bearish expectations persist, given that EUROFER had earlier projected a 3% growth.

Even with the projected rebound, the EU’s steel consumption is estimated to remain well below pre-pandemic levels, by around 11 mnt in CY’26 and 9 mnt in CY’27.

Similarly, the decline in real steel consumption is projected at a minor 0.2% against the earlier forecast -2.1%. Restocking is expected only in late 2026 amid prolonged uncertainty and low confidence in economic and industrial activity.

Imports surge in CY’25, market penetration hits record high

The EU’s steel imports increased 14% y-o-y in CY’25, with finished longs up 17% and flats rising 7%. Q4CY’25 witnessed a sharp 53% surge in total imports, as buyers actively stocked up on cheaper imported material ahead of the phase-in of the definitive period of the Carbon Border Adjustment Mechanism (CBAM), fearing high carbon costs.

Notably, in Q3CY’25, imports accounted for 29% of the EU’s apparent steel consumption – a record high.

Imports increased sharply from Indonesia (+263%), Turkiye (+24%), and China (+31%) but declined from India (-28%) and Taiwan (-15%).

Conversely, the EU’s steel exports to third countries decreased by 12% in CY’25, pointing to a weakening trade balance.

Steel-consuming sectors’ performance rebounds in Q3CY’25

In Q3CY’25, the Steel Weighted Industrial Production index (SWIP) – an indicator of real steel consumption in major end-user segments – increased for the first time since Q4CY’23.

Positive growth in all steel-consuming sectors – construction (1.6%), automotive industry (1%), mechanical engineering (0.6%), and steel tubes (3.8%) – triggered an increase of 1.8% following six consecutive quarters with a decline.

In CY’25, the SWIP is projected to fall 0.3% amid US tariff uncertainties despite a modest recovery in the construction sector.

Construction sentiment improves as investment growth surges: In Q3CY’25, a substantial 15% increase in construction investment led to improved construction output. However, the sector is expected to grow merely 0.7% in CY’25, weighed down by subdued housing demand during H1.

Growth is expected to accelerate in the next two years, aided by easing monetary policies and increased government expenditure. The major pillars of development will be the implementation of NextGenerationEU investment schemes – a post-COVID recovery instrument by the European Commission (EC) – along with increased flexibility in EU fiscal rules for Member States and Germany’s massive EUR 500 billion infrastructure fund announced in CY’25.

Tariff tensions, weak demand keep auto sector in slow lane: Output from the automotive sector is set to remain subpar with a 4.3% fall projected in CY’25.

Mounting trade challenges, especially with the US’s tariffs on EU-manufactured cars and increasing Chinese EV exports to the EU, weighed on automakers’ investment decisions; order delays due to supply chain disruptions (such as over the adequate availability of rare earth elements) also dampened production momentum. Similarly, war-led turmoil, low growth in disposable incomes, and economic uncertainty dragged down consumer confidence.

However, a promising sign is that new car registrations in the EU increased slightly by 1.8% y-o-y in CY’25, driven by a surge in EV sales as petrol- and diesel-powered cars lost ground. Consequently, EUROFER remains optimistic regarding a modest rebound in automotive output in CY’26-27.

Recession in mechanical engineering continues: The mechanical engineering sector is set to close CY’25 with a recession (-0.8%), though modest growth is expected in the next two years as manufacturers’ confidence strengthens.

Demand outlook for tubes segment remains mixed: In CY’25, a marginal 0.2% recovery in steel tubes output is expected. However, while output is expected to grow further in CY’26 and CY’27, the outlook remains mixed. As the EU transitions to LNG shipping, development of pipeline gas infrastructure will gradually stagnate. However, demand from the construction segment will likely increase and that from the automotive and engineering sectors will remain stagnant.

Outlook

GDP growth forecasts for the EU stand at 1.2% in 2026, revised downward from 1.4% previously, suggesting that steel demand will remain weak despite a modest rebound. However, at the moment, the more pressing concern is regarding production. Given the outbreak of the US-Iran conflict and the resultant surge in gas and energy prices, it is uncertain whether EU steelmakers will be able to significantly lift their capacity utilisation rates, which were already at below profitable levels. This is despite protective measures such as the CBAM and reduced import quotas.

Weak demand will continue to pressure steel prices, but with cost pressures rising simultaneously, producers may be forced to slow down operations. This would again weigh on profitability, leading to (borrowing a term from EUROFER’s report) a “continued downsizing of the European steel industry”.

Leave a Reply