- Baltic Capesize Index climbs up by 604 points w-o-w

- India-China freights drop as route sees nil fixtures

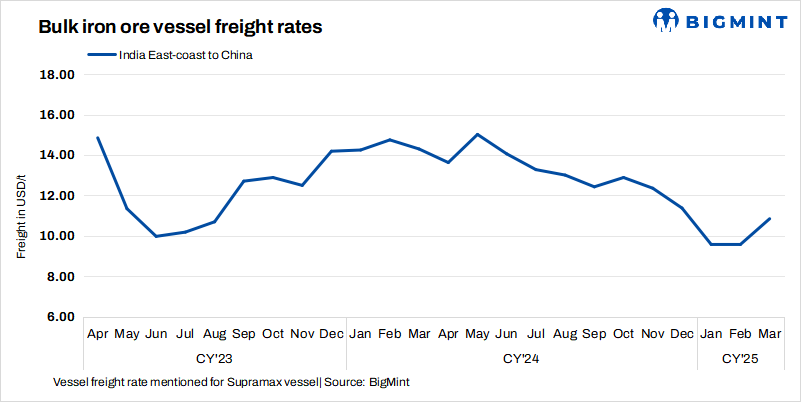

Dry bulk iron ore freights showed mixed movements w-o-w across different routes. Freights from India to China edged down this week following limited inquiries, a surplus of prompt tonnage, and subdued market activity across key regions. In the Indian Ocean, a lack of fresh cargo along the Indian coasts exerted downward pressure on rates, while a lengthy list of available vessels further restricted any potential rate increases.

Additionally, a wait-and-watch approach by market participants, coupled with cautious sentiment in the Asia-Pacific region, contributed to the overall sluggishness in the market, preventing any significant upward movement in freights.

However, Capesize vessel freights increased on some routes. This could be attributed to a combination of factors, including active demand from major Western Australian miners, along with fresh iron ore orders in the Pacific. Additionally, disruptions at key Chinese ports, such as Qingdao and Changjiangkou, due to dense fog could have temporarily constrained vessel availability, creating tighter supply conditions.

While freight derivative (FFA) rates softened towards the end of Asian trading hours, overall demand for Capesize vessels remained steady, supporting freights.

Factors influencing freights

- Baltic indices show mixed trends w-o-w: The Baltic Dry Index (BDI) was recorded at 1,400 points on 10 March, increasing by 171 points w-o-w. Additionally, the Baltic Capesize Index (BCI) stood at 2,422 points, rising by 604 points w-o-w, reflecting positive sentiment. However, the Baltic Supramax Index (BSI) inched down by 31 points w-o-w to 864 points.

- China’s iron ore spot prices remain firm w-o-w: China’s spot prices of iron ore fines (Fe62%) were assessed at $101.95/t CFR on 11 March, unchanged w-o-w amid fresh market activity. Seaborne cargo prices increased d-o-d, though wider discounts were seen on some medium-grade fines as Australian shipments resumed. As per sources, the market has stabilised, with end-user demand favouring premium medium-grade products for better margins.

Route-wise updates

- India-China: Freights from the Indian Ocean to China were recorded at $10.7/t, inching down by $0.3/t w-o-w. Although no new fixtures were finalised, some rumours suggest otherwise.

- Australia-China: Freights for Capesize vessels carrying iron ore from Western Australia to China were assessed at $9.9/t on 12 March, edging down by $0.1/t w-o-w. According to sources, major Australian miners Rio Tinto, BHP and FMG were seen actively booking Capesize vessels from a Western Australia port to Qingdao Port at around $9.90-10.15/t. Shipment is scheduled for 22-28 March.

- Brazil-China: Freights for Capesize vessels from Brazil to China climbed up this week. Rates from Tubarao to Qingdao Port were assessed at $22.7/t on 12 March, up by $2.90/t w-o-w. As per sources, Vale and Oldendorff booked Capesize vessel from Tubarao to Qingdao at around $20.90-22/t, with shipment scheduled for 27 March-10 April.

- South Africa-China: Capesize freights from Saldanha Bay Port to Qingdao Port increased by $1.70/t w-o-w to $16.6/t amid firm demand and tighter vessel availability. Additionally, market participants likely adjusted offers in response to broader freight trends and regional supply dynamics.

Leave a Reply