- Monsoon-led mining disruptions drive up iron ore tags

- Coking coal tags head north on rebound in Chinese market

- Finished steel demand stays weak on monsoon slowdown

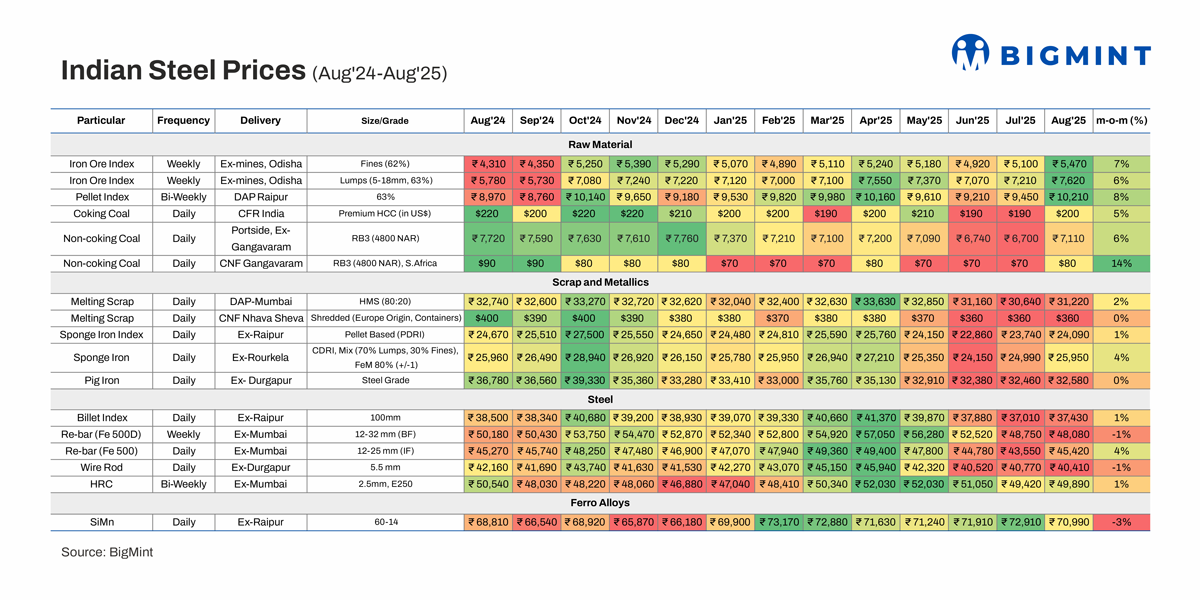

Morning Brief: Indian steel and raw material prices showed mixed trends m-o-m in August 2025.

Prices of iron ore, pellets, and coal, the basic raw materials in the steelmaking process, witnessed moderate growth in the range of 5-14%. However, commodities further downstream, such as sponge iron, pig iron, and billets, remained largely stable m-o-m. This supported finished steel prices, though demand was lacklustre amid a persistent slowdown in construction activity and a spate of festive holidays.

While prices had strengthened in late-July, amid expectations of a post-monsoon demand recovery, the upward momentum could not be sustained. August continued to witness lukewarm finished steel trade.

Price movements of domestic steel, raw materials in Aug’25

Iron ore

Iron ore: The Odisha iron ore fines (Fe 62%) index was up by 7% m-o-m at a monthly average of INR 5,470/tonne (t), while lumps (Fe63%) increased by 6% to INR 7,620/t, both ex-mines. The price gains were driven by material shortages, as the monsoon disrupted mining and logistics operations. Miners made limited offers, while dispatches were irregular. Amid depressed steel prices, procurement was largely to fulfil urgent requirements or maintain operations at plants.

Notably, NMDC increased list prices of iron ore CLO (calibrated lump ore) and fines by INR 450/t and 400/t, respectively, at the beginning of the month. Additionally, in OMC’s iron ore auction on 19 August, fines received premiums of INR 50-700/t, while lumps fetched premiums of up to 26%. Fines bids (weighted average) rose by INR 300/t m-o-m, while lumps remained largely stable.

Pellets: Raipur’s pellet prices (Fe63%) increased 8% m-o-m to INR 10,210/t DAP, keeping pace with the hike in iron ore. The price rise stemmed from higher iron ore procurement costs, limited material availability, and a preference for pellets to lumps – all due to the impact of the monsoon. However, a soft steel market limited demand to immediate needs.

Coal

Coking coal: Premium hard coking coal (PHCC) prices increased by 5% m-o-m to $200/t CFR, with improved market sentiments in China contributing to upward momentum in India. Notably, restrictions on coking coal production in China triggered supply shortages and an uptrend in prices of the same. However, trading activity in India was moderated by wide bid-offer disparities.

Non-coking coal: Portside RB3 (4800 NAR) non-coking coal prices moved up by 6% m-o-m to INR 7,110/t ex-Gangavaram. South African, CNF Gangavaram, prices of the same grade witnessed a sharp 14% uptick to $80/t.

Non-coking coal prices climbed higher due to a decline in portside inventories, which slipped to 13.78 mnt in late August from around 14.27 mnt in the first week. Freight hikes – due to tight vessel supply – also boosted tags in the beginning of the month, and some sponge iron producers booked material, banking on a recovery in demand following the monsoon. Additionally, domestic coal prices, ex-Bilaspur, also increased m-o-m, fuelled by constrained supply due to monsoon-hit operations.

Scrap & metallics

Melting scrap: Domestic HMS (80:20) prices recovered modestly, by 2% m-o-m to INR 31,220/t DAP Mumbai in August. Prices were relatively stable m-o-m amid limited supply due to heavy rains and strength from alternative raw materials. Melting scrap tags surged at the beginning of the month due to an improvement in steel prices, but then weakened and plateaued at higher levels than July. Late-August saw prices returning to late-July levels amid weak trading activity due to torrential rains and subdued steel demand.

Meanwhile, imported European shredded was flat m-o-m at $360/t CNF Nhava Sheva. Trading activity was dampened by subdued steel demand, competitively priced domestic scrap, and currency depreciation. Festive holidays also led to demand slumps at regular intervals, while unviable freights also shrank import appetite.

Sponge iron: Pellet-based direct reduced iron (PDRI) inched up by 1% m-o-m to INR 24,090/t ex-Raipur, while the lump-based variant rose a steeper 4% to INR 25,950/t ex-Rourkela. The marginal rise could be attributed to higher raw material costs, which sellers attempted to pass on to buyers. However, weak demand and sluggish finished steel offtake pressured prices and limited sharper spikes.

Pig iron: Steel-grade pig iron remained firm m-o-m at INR 32,580/t. Cautious sentiment limited trade activity, and prices moved in a narrow band across regions. Auctions saw mixed trends, reflecting market uncertainty amid soft steel demand.

Ferro alloys

Silico manganese: Domestic prices of the 60-14 grade of silico manganese dipped by 3% m-o-m to around INR 71,000/t exw-Raipur in August. Output remained steady, but limited inquiries pushed producers to reduce offers to stay competitive. Mills were cautious amid ample inventories and a subdued steel market, and export trade also failed to offer a cushion to slack domestic demand.

Semi-finished steel

Billet: Domestic billet prices inched up by 1% m-o-m to INR 37,430/t exw-Raipur in August. Firm sponge iron and scrap prices propped up billet tags, but the market was consistently under pressure due to weak downstream demand from secondary mills.

Finished steel

BF-rebar: Blast furnace (BF) route rebar (Fe500D) prices dipped by 1% to average INR 48,080/t exy-Mumbai, driven by subdued demand. Expecting a market rebound, Indian primary mills had increased rebar prices by up to INR 2,000/t for early-August 2025 deliveries, though inventories were higher by over 45% m-o-m.

However, the monsoon-driven slowdown in construction activity continued, and a series of festive holidays further dampened trade activity. Steel mills also trimmed list prices a few times throughout the month to engage buyers, but procurement remained lukewarm.

Meanwhile, prices in the projects segment remained stable at INR 47,400/t FOR Mumbai, with logistics disruptions and heavy rains contributing to project delays.

Notably, rebar inventories with Tier-1 mills remained largely unchanged m-o-m in early September. Sluggish domestic demand prevented any major declines in inventories.

IF-rebar: Induction furnace (IF) rebar (Fe500) prices climbed up by 4% m-o-m to INR 45,420/t ex-Mumbai in August. Sponge iron and billet prices edged up, supporting rebar tags, but again, heavy monsoon rains and festival-related disruptions led to sluggish order bookings. IF-rebar inventory levels increased to around 15-17 days in August from around 10-12 days in July.

Wire rod: The same dull market sentiments were reflected in the wire rod market. Binding and GI wire manufacturers took a guarded approach to bulk procurement due to uncertainty regarding market direction. Consequently, prices dipped by 1% to INR 40,410/t.

HRC: Prices of hot-rolled coils (HRCs) inched up by 1% m-o-m to INR 49,890/t ex-Mumbai. While demand had improved at the beginning of the month, leading primary mills to raise list prices, monsoon-led disruptions and festivals slowed down trade activity. Labour shortages also delayed restocking decisions, while ample market supply and sufficient inventories at buyers reduced urgency for fresh purchases.

Outlook

The market seems to be divided about whether a recovery is in the offing in the coming days. While some Tier-1 mills have increased rebar list prices for early-September, the outlook for HRCs remains clouded. Till mid-September at least, trading momentum may remain depressed. However, most participants are confident that the post-monsoon period will bring a demand pick-up and look forward to pre-festive period restocking activity at the end of September.

Leave a Reply