- Margins pressured by weaker long product prices

- Q2FY26 EBITDA projected to soft q-o-q, up y-o-y

Indian steel mills are projected to report a y-o-y growth in their EBITDA per tonne for September quarter (Q2FY26), although growth rate can come down from the high seen in Q1FY26. Aggregate EBITDA per tonne of the top four steel producers is expected to range between INR 10,300-10,600 during Q2FY26, higher by about 2-4% on y-o-y basis but sequentially lower by 5-8% q-o-q. In Q1FY26, aggregate EBITDA per tonne had risen by about 9% on y-o-y basis.

The performance is affected by subdued steel prices with monsoons leading to lower construction activity. Average prices of hot rolled coils for July and August, stood at about INR 49,700/t, lower by 2% on y-o-y basis and 4% on q-o-q basis. Prices are expected to remain soft during September but pick up after that. Decline in rebar prices was sharper by 6% on y-o-y basis to INR 48,400/t and 13% on sequential basis, whereas galvanised products prices remained unchanged on y-o-y basis but fell by 5.8% to Rs 61,000/t on q-o-q basis.

The mills are expected to get some support from soft coking coal prices with prices being lower by 6% on y-o-y basis, although increasing by 5% on quarterly basis. Yet, the full impact of change in raw material prices would reflect on the company’s financials in the next quarter.

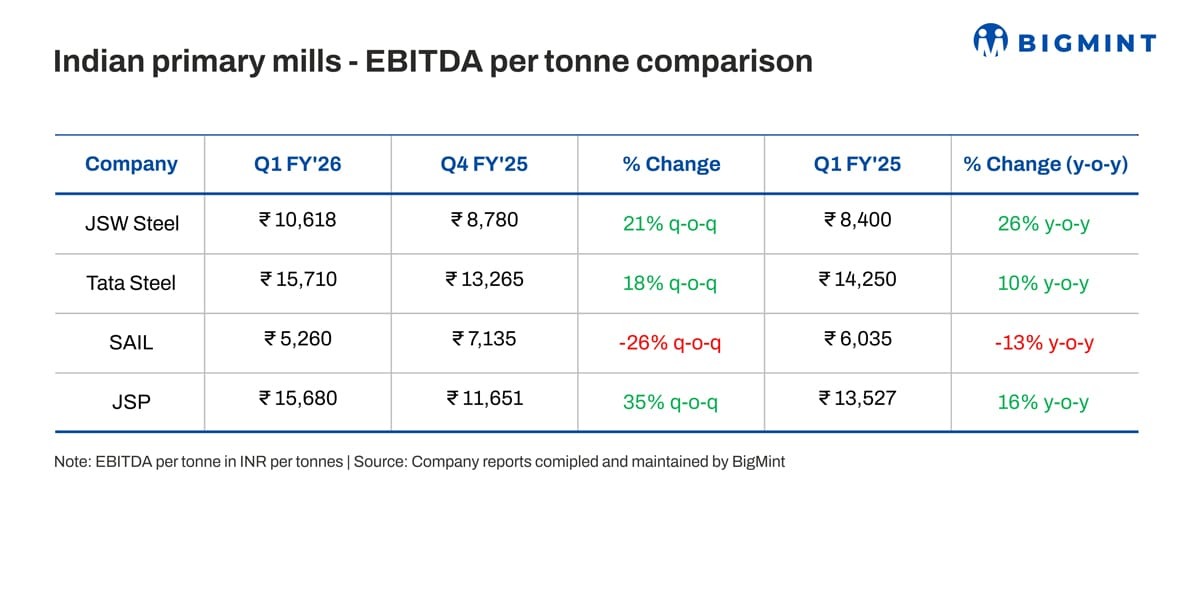

Lower long product prices to weigh on Jindal Steel’s Q2FY26 margins

Among the individual companies, Jindal Steel (earlier, Jindal Steel & Power), Tata Steel and JSW Steel are expected to report EBITDA per tonne growth in the range of 6-12% on yoy basis, Jindal Steel had the best Q1FY26 with its EBITDA per tonne hitting a 10-quarter high of INR 15,680, an increase of 16% and 35% on y-o-y and q-o-q basis. The company may see higher impact of lower construction activity with a higher share of long products at about 60%. As a result, its Ebitda per tonne may decline by 20-30% on q-o-q basis, although still higher marginally on y-o-y basis.

Tata Steel & JSW Steel

Tata Steel also had a strong Q1FY26 with y-o-y and q-o-q growth of 18% and 10% respectively in its EBITDA per tonne to INR 15,700, a six-quarter high. The company had ramped up its capacity in the recent quarters and benefitted from economies of scale. JSW Steel’s EBITDA per tonne also touched a six-quarter high in Q1FY26 to INR 10,618, increase of 26% and 21% on y-o-y and q-o-q basis. The companies gained from firm flat products prices, supported by the safeguard duty, but the advantage has partially diminished in Q2. As a result, while profitability is expected to improve on y-o-y basis, it may not sustain at the level of Q1FY26 and decline sequentially by 7-10%.

SAIL’s EBITDA expected to decline y-o-y in Q2, while rise on q-o-q basis

Steel Authority of India Ltd (SAIL) is projected to be an outlier with EBITDA per tonne expected to decline on y-o-y basis. The company had a dismal Q1FY26, with Ebitda per tonne hitting a 10-quarter low of INR 5,260, decline of 13% and 26% on y-o-y and q-o-q basis. SAIL’s performance was affected by accounting adjustments and inventory revaluation. September quarter is expected to see no more such adjustments, helping the company post better numbers sequentially.

Outlook

Beyond Q2FY26, outlook for the steel mills, especially the flat producers look promising with the recent recommendation of the Directorate General of Trade Remedies (DGTR) to impose final safeguard duty on flat products for three years (at declining rate of 12%, 11.5% and 11%), giving producers greater certainty. The GST rate correction, with most of the consumption products expected to see a decline in GST tax rate, could be another trigger for the companies. GST and other reforms have become more imperative so as to help exports-based industries tide over the crisis induced by imposition of a 50% tariff by USA.

Disclaimer: The data, projections, and opinions contained herein are based on sources considered reliable at the time of publication but are not guaranteed for accuracy or completeness. This content does not constitute investment, trading, or financial advice, nor does it recommend or endorse any specific securities or companies. Bigmint does not assume any liability for decisions made based on this information. Readers and stakeholders are encouraged to conduct their own due diligence and consult qualified advisors for investment decisions.

Leave a Reply