- Japan aluminium premium rises 13% for Q3 shipments

- Global zinc mine output expected to decline 1.8%

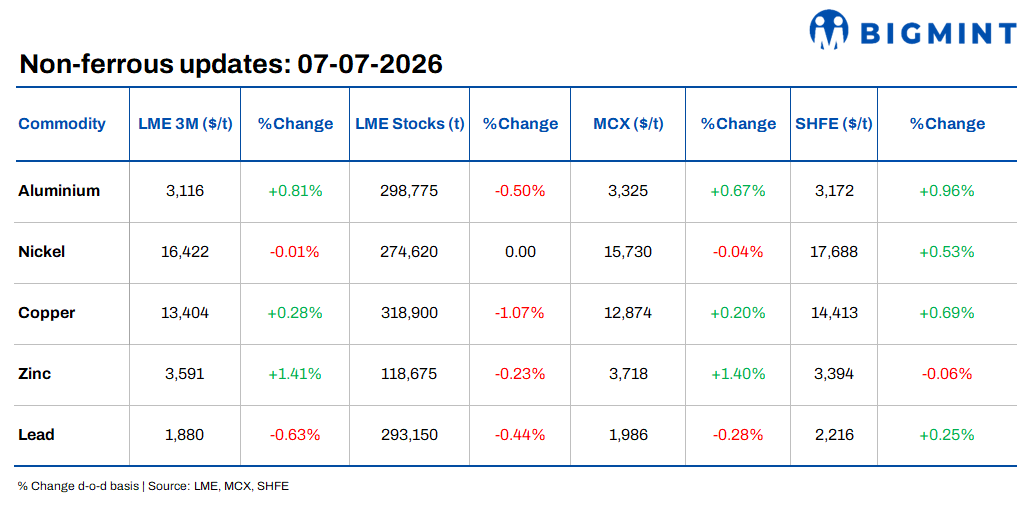

Base metals on the London Metal Exchange (LME) traded mixed on 6 July 2026 as zinc rose 1.41% d-o-d to $3,591/t, followed by aluminium, which increased 0.81% to $3,116/t. Copper also edged higher by 0.28% to $13,404/t, while nickel remained largely unchanged, slipping 0.01% to $16,422/t. Lead was the only major decliner, falling 0.63% to $1,880/t. The gains were supported by continued declines in LME inventories, particularly for copper, which offset cautious macroeconomic sentiment.

On the inventory side, copper stocks recorded the sharpest decline, falling 1.07% d-o-d to 318,900 t, followed by aluminium inventories, which dropped 0.50% to 298,775 t. Lead and zinc inventories also declined 0.44% and 0.23% to 293,150 t and 118,675 t, respectively, while nickel inventories remained unchanged at 274,620 t.

Domestic market overview

India’s non-ferrous scrap market weakened on 6 July amid softer domestic demand. Aluminium tense scrap (loose), ex-Delhi, declined by INR 2,000/t, or 0.74% d-o-d, to INR 270,000/t, while ex-Chennai prices fell by INR 9,000/t, or 3.40%, to INR 256,000/t.

Meanwhile, copper armature scrap (Cu 99%), ex-Delhi, declined by INR 17,000/t, or 1.41% d-o-d, to INR 1,186,000/t, tracking weaker domestic buying activity despite firm LME copper prices.

Oil steadies as Saudi price cuts offset OPEC+ supply concerns

Global crude oil prices were mixed on 7 July 2026, with WTI crude rising 0.39% d-o-d to $68.99/bbl and Brent crude increasing 0.74% to $72.49/bbl. Natural gas gained 1.57% to $3.23/MMBtu.

Market sentiment remained focused on rising global crude supply after OPEC+ approved another 188,000-bpd production increase for August, marking the fifth consecutive monthly output hike. At the same time, Saudi Arabia announced its largest cut in official selling prices for Asian buyers in more than 20 years, reducing the August Arab Light premium by $11/bbl to $1.50 below the Oman-Dubai benchmark in an effort to defend market share amid weakening regional demand.

Improving crude exports through the Strait of Hormuz, higher output from Gulf producers and subdued Chinese demand continued to reinforce expectations of an oversupplied market. However, analysts cautioned that lingering geopolitical risks and elevated shipping costs could still limit further downside in oil prices.

Other updates

Japan’s aluminium premiums hit highest level since 2015

Japanese aluminium buyers have agreed to pay a premium of USD 395/t over the LME benchmark for July-September 2026 shipments, up 12-13% from USD 350-353/t in the previous quarter. The settlement marks the third consecutive quarterly increase and the highest premium since Q1 2015, when it reached USD 425/t. Producers had initially sought premiums well above previous levels, citing tight physical supply, while the agreed price reflects continued strength in the regional market.

The higher premium was driven by geopolitical disruptions, changes in global trade flows and persistently low LME aluminium inventories, which reduced spot metal availability and strengthened producers’ negotiating position. As Japan is Asia’s largest aluminium importer, its quarterly premium settlements serve as a key benchmark for physical aluminium shipments across the region.

Global zinc mine output declines in 2025

Global zinc mine production is expected to decline by 1.8% in 2025 to around 11.8 million tonnes, primarily due to lower output from major producers including Peru, China and Australia, according to the International Lead and Zinc Study Group (ILZSG). In contrast, lead mine production is projected to increase by 1.8% to approximately 4.7 million tonnes, supported by higher output from China, Mexico and Kazakhstan.

Despite weaker zinc mine supply, refined zinc production is expected to remain broadly adequate as inventories improve, while the contrasting outlook highlights diverging supply dynamics across the two base metals.

Leave a Reply