China’s metallurgical coke prices were temporarily steady after the completion of the second round of price cuts last week, but outlook for the near-term price trend was divided as steelmaking margins rebounded.

Bearish sentiment further reduced on expectation of eased price-cut intention of steelmakers following a rebound in their margins after cuts on coke and PCI coal prices as well as rebounds of steel product prices.

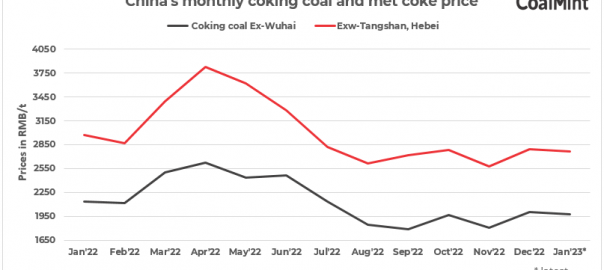

Coke prices fell by two rounds totalling RMB 200-220/t since the start of the month, and PCI coal prices also fell by around RMB 80-90/t during the same period.

The decline of coke and PCI coal prices, coupled with a rebound in steel product prices, had basically outpaced the impact of rise in iron ore prices during the same period, resulting in higher steel margins.

Adding to the enhanced expectation, some speculative purchases of coke emerged in the market and a recent snowfall affected coke supply in northern China.

Stable coking coal prices add cost support

Increasing coking coal miners were expected to hold offer prices unchanged ahead of the upcoming holiday, backed by the continued downside of supply.

Sxcoal’s tracking data showed the holiday breaks of the surveyed mines averaged 11.2 days, rising by 1.4 days from a year ago. Out of that, private mines averagely take 14.1 days, while state-run mines 6.9 days. Increasing miners would take leave in a few days, Sxcoal learned.

Mines still in production tended to maintain prices steady, although coke firms remained cautious in placing orders, and the overall downward room of coking coal settlement was expected to be small, a key factor that may help keep coke prices from further decline.

Note: This article has been exchanged under the article exchange agreement between CoalMint and Sxcoal.

Leave a Reply