- Power plants delay restocking amid high inventories

- Record high port stocks spark aggressive price wars

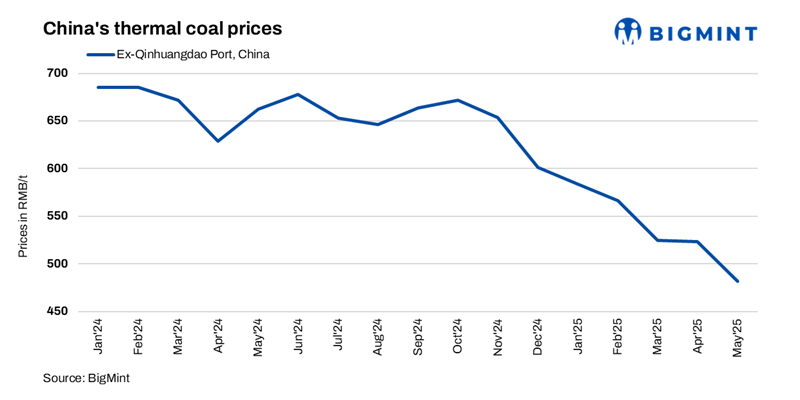

Mysteel Global: China’s thermal coal market extended its downturn for another month through May, with sluggish demand, swelling port inventories, and persistent oversupply plunging spot prices to their lowest levels since March 2021.

Prices of 5,500 kcal/kg thermal coal at northern transfer ports stood at RMB 620/tonne (t) ($86.2/t) by 29 May, down RMB 40/t from earlier in the month and by a staggering RMB 260/t y-o-y, according to Mysteel’s assessment. The price plunge underscores intensifying headwinds in what many had expected would be a summer demand-driven rally.

Market activity remained muted throughout the month, with electric power companies exhibiting a go-slow approach to restocking. Price-sensitive procurement became the norm as utilities capitalised on ample inventory and lacklustre coal burn rates.

The price slide was most acute in the first half of May. By mid-month, the price of benchmark 5,500 kcal/kg NAR portside coal had shed RMB 35/t. The retreat was triggered by ongoing maintenance at thermal power units and unusually heavy rains across South China, both of which suppressed electricity loads and left plant stockpiles bloated.

Data from Mysteel showed that as of 16 May, coal inventories at the 462 sampled power plants remained at elevated levels, with coverage adequate for 25 days. Similarly, the six key coastal power plants in East and South China had 19.3 days’ worth of coal on hand on the same day, up from 18.3 days at the beginning of the month, sources revealed.

Portside inventories surged to record highs, putting additional downward pressure on prices. The eight major ports tracked by Mysteel in the Bohai Bay region held a combined stockpile of a record 30.66 million tonnes (mnt) as of 14 May, sparking a renewed wave of aggressive undercutting as sellers raced to offload cargo. The resulting “involution-style” price war, a term used by Chinese traders to describe self-cannibalising competition, sent ripples through the market.

In the latter half of the month, prices showed tentative signs of stabilising. During 15-29 May, benchmark coal dipped by just RMB 5/t. Warmer weather across eastern, northern, and parts of southern China pushed up air-conditioning loads, prompting marginal increases in coal consumption. Power plant inventories saw a slight drawdown, with the coastal six’s coverage days slipping lower to 18 by 29 May.

At the same time, major coal-producing regions maintained steady output, intensifying the oversupply issue in the portside market, Mysteel Global noted. Data from Mysteel revealed that daily output at the 462 mines it regularly surveys had held steady at a high of 5.7-5.8 mnt, as compared with 5.6-5.7 mnt in April and 5.4-5.5 mnt in May 2024. The trend signals that producers are doubling down on output to offset shrinking margins, opting to “make up in volume what we lose in price”.

Regulatory factors have had a limited impact on output. A coal mine roof collapse in southwestern China’s Sichuan province on 17 May, which killed four workers, prompted safety reviews across core producing areas, but production remained largely unaffected. Some marginal reductions occurred at month-end, as a handful of mines hit their production targets, but these were insufficient to dent overall supply volumes.

Looking ahead, analysts expect continued softness in coal prices for the rest of this year. The China National Coal Association predicts 2025 domestic coal output to rise by 5%, outpacing expected demand growth of just 1.5%-2%. With profitability in the coal mining sector down 48.9% in the January-April period, many producers appear increasingly willing to flood the market in a bid to stay afloat, a strategy that could entrench the current oversupply and drive prices even lower.

Utilities are also likely to maintain high inventory levels as a hedge against summer volatility, muting any price gains from seasonal demand spikes. Rising output from renewables and continued adherence to long-term contracts may further undercut the spot market, leaving little room for a price rebound.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply