- Demand seen tripping by 2% in this calendar

- Iron ore oversupply may dampen Chinese appetite

- Will US tariffs force down exports from June?

China is not likely to opt for crude steel production cuts in 2025 amid macro compulsions, while demand will be 1.5-2% lower this year. Such issues, along with steel and iron ore supply-demand dynamics as well the tariff impacts were discussed at a recent webinar on “Tariffs and Turbulence: Impacts on Chinese Steel Production and Iron Ore Imports,” jointly hosted by BigMint and Horizon Insights — China’s largest independent investment research house.

Speaking as a panellist, Jiang Mengtian, Chief Ferrous Metal Analyst at Horizon Insights, said rumours are rampant, especially since February-March, that NDRC will implement production cuts of 20-50 million tonnes (mnt). So far, NDRC has not made any official announcement to that effect. All it has said is that production cut is in line with the expectations from the market.

But, to understand the situation better, one needs to take a look back at 2021 and 2023, two years when cuts had been implemented. However, it was only in 2021 that the Chinese government had officially declared output reductions. In 2023, despite rumours, the government did not announce nationwide production cuts. Result? Hot metal output in the second half of the year did not go up and production margins of steel mills were very low. “This year is very similar to 2023. The demand side is facing a lot of pressure, especially because of the escalation of the trade war. As a result, China will possibly not implement production cuts in 2025. Because, such a move may further lower economic activities,” Jiang informed.

“Even if production cuts do happens, a mere 20 mnt is not going to improve prices of steel, because the decrease in output is exactly matching the decrease in demand. If the cut is at 50 mnt, it will be a very different story. But, at this juncture, the economic situation in China is unlikely to allow production cuts,” Jiang stressed.

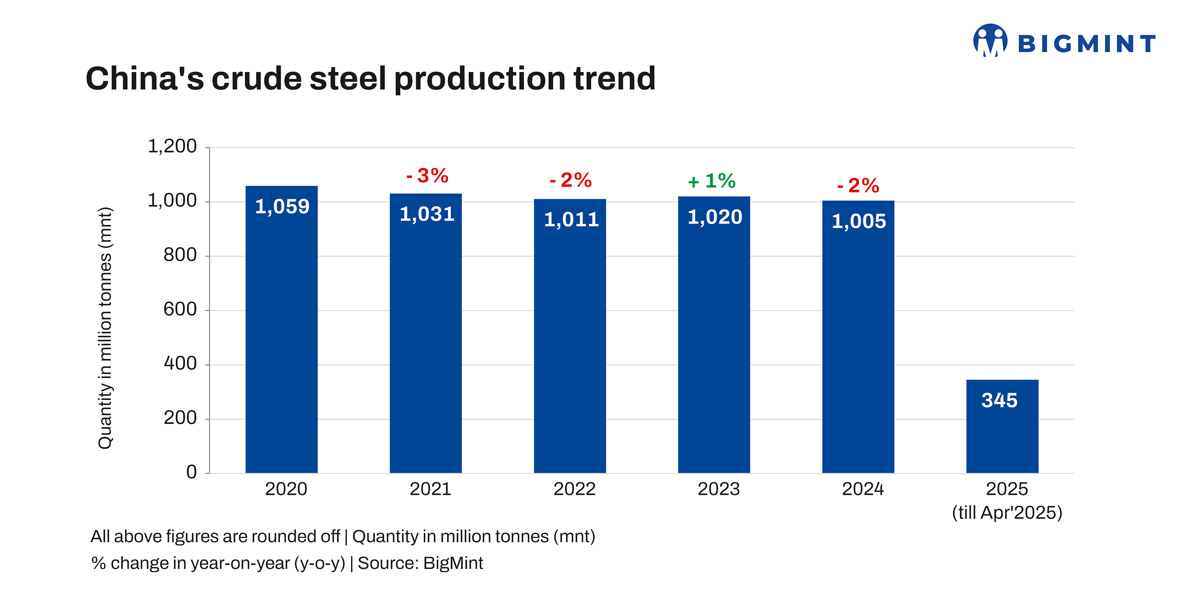

Over January-April, China’s crude steel production was up a negligible 0.4% to 345.40 mnt. In 2024, output totalled 1005.10 mnt, down 1.7% y-o-y, as per worldsteel data.

Hot metal output to dip from June

China’s hot metal output will remain at 2.45 mnt per month and start declining from June, Jiang observed. Not only in exports, domestically, China’s construction will enter the off-season so the demand will be lower which in turn will drag down hot metal output.

Demand-side bearish, despite govt support

Demand in 2025 will be 1.5-2% lower compared to 2024, despite government support. Investment data for April showed a decrease of 12%. The newly started real estate projects, a segment closely linked to demand for rebar, also decreased more than 22%. “From the decreasing investment in the real estate sector, we can see there is no support for rebar to rebound,” said Jiang.

In 2025, construction downstream demand is expected to dip by 1% and real estate by a steep 15%.

Iron ore supply to rise on lower freight

Based on the overall increase in iron ore supply and also the ratio of shipments to China, the increase in the same to China will be around 20-22 mnt in 2025. Other countries are price elastic but for this year, the bunker price decrease has lowered the cost of exports, it is learnt. “So we can expect supplies from India to China to remain supported due to the lower shipment fee,” Jiang indicated.

Where iron ore pricing is concerned, co-panelist Qin Cui, Director of the Jianfa Steel Industry Research Institute, said, currently, she does not see Chinese steel mills very active in iron ore purchase because there will be a lot of supply especially in the second half of this year and also over 2026-27. “Thus, mills are not so active in ore purchase because port inventory is pretty high. So, they will do hand-to-mouth or need-based purchases. If the price drops to below $90/t, may be, they will do more procuring but currently we don’t see any active current purchasing from here,” she emphasized.

EAF capacity increase hindered by scrap

Qin Cui also said China is not expecting to see an increase in electric arc furnace (EAF) capacity as the government wants to implement more environment-friendly production methods. “Our EAF capacity has been increasing but slowly. Since supply of scrap as a raw material currently is not in plenty, EAF capacity cannot be quickly increased. So EAF margins have been in the negative since last year. Because profit margins are not good, EAF production cannot be increased faster than BOF production. Thus, although a very big EAF capacity is in the plan, we are not optimistic on the production for the next 10-30 years,” Qin informed, taking a long-term view.

US tariffs to impact exports

Exports may start declining June onwards. “After the 90 days tariff pause, if the total demand of Chinese steel, domestic and exports, does not improve, which is likely, exports are expected to be impacted from the second half of the year, Jiang said. In fact, net exports may end the year with a 3.5% decline.

Qin informed that, with eased China-US tariff tensions, “black” commodity prices did rise generally. Valuation-wise, finished steel, under weak expectations, remained at the lower end, and coking coal hit new lows.

Prices likely to fall further

Average prices of steel in the next two quarters, if there is no production cut, will come down to around RMB 3,000/t ($417/t).

Iron ore will gradually come down from $100/t to $95-90/t over the next three quarters.

Seasonal demand is weakening for both construction steel and flats, though export resilience and hot metal schedules suggest limited downside in the short-term. In the medium-to-long term, iron ore shipments are expected to increase while sustained coking coal oversupply may intensify raw material surplus. “When iron ore fundamentals eventually weaken, significant price corrections could occur, erasing finished steel margins,” Qin observed.

Leave a Reply