- High stocks offset impact of output cuts

- ZCE future prices inch up by $10/t w-o-w

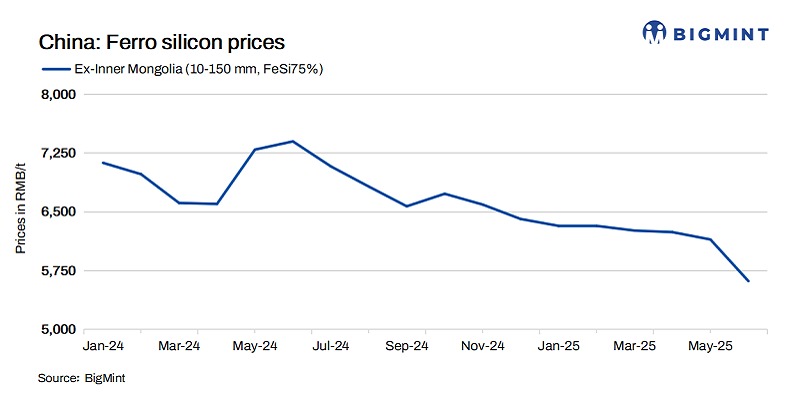

CBC: China’s ferro silicon prices recorded marginal hikes w-o-w, though the market was subdued. Despite minor output cuts, high inventory levels continued to pressure the market. Weak demand from the steel and magnesium sectors persisted, and cost support was minimal. Market sentiment was cautious, with trading driven by urgent needs only.

Grade 72% silicon: Prices edged up by RMB 10/tonne (t) ($1/t) w-o-w to RMB 5,240-5,400/t ($730-752/t) ex-factory, inclusive of taxes.

Grade 75% silicon: Prices inched up by RMB 50/t ($7/t) w-o-w to RMB 5,620-5,760/t ($783-803/t).

Market updates

Output cuts offset by high inventories: The ferro silicon market remained stable but reflected a clear supply-demand stalemate. Although some producers in Ningxia announced output reductions due to losses and daily production declined slightly, overall supply remained elevated. Inventory drawdown was also slow.

Elevated inventories at delivery warehouses continued to pose pressure, indicating that the issue of oversupply has not been fundamentally resolved, keeping the market in a state of cautious observation.

Weak demand continues amid limited cost support: On the demand front, market activity remained subdued. Mills replenished stocks at a slow pace amid the seasonal lull in downstream steel demand.

Additionally, demand was pressured by falling molten iron output and weak magnesium metal consumption. As a result, trading was largely driven by need-based purchases, with limited momentum for a broader market recovery in the near term.

Raw material prices, including semi-coke, remained weak, providing limited cost support. Market sentiment was subdued, with traders showing low restocking interest.

ZCE futures inch up w-o-w: On 26 June, ferro silicon prices on the Zhengzhou Commodity Exchange (ZCE) for September 2025 delivery inched up by RMB 74/t ($10/t) w-o-w to RMB 5,384/t ($750/t) from RMB 5,310/t ($740/t).

Outlook

In the short term, ferro silicon prices are likely to stay range-bound amid persistent oversupply and sluggish demand. Output cuts have had limited impact due to high inventories, while weak cost support and subdued procurement from steel mills suggest continued cautious sentiment.

Leave a Reply