- Market quiet ahead of Eid and budget

- Falling rebar prices weighing on scrap demand

Bangladesh’s imported ferrous scrap market remains subdued heading into June 2025, with trading activity slowing due to multiple factors. The Eid vacation, scheduled from 5-15 June, is expected to dampen market momentum, with subdued activity likely to persist until at least 20 June. Mills are holding back major purchases ahead of the national budget announcement in June, while ongoing freight challenges from Hong Kong have added further pressure on scrap imports.

BigMint’s weekly assessments

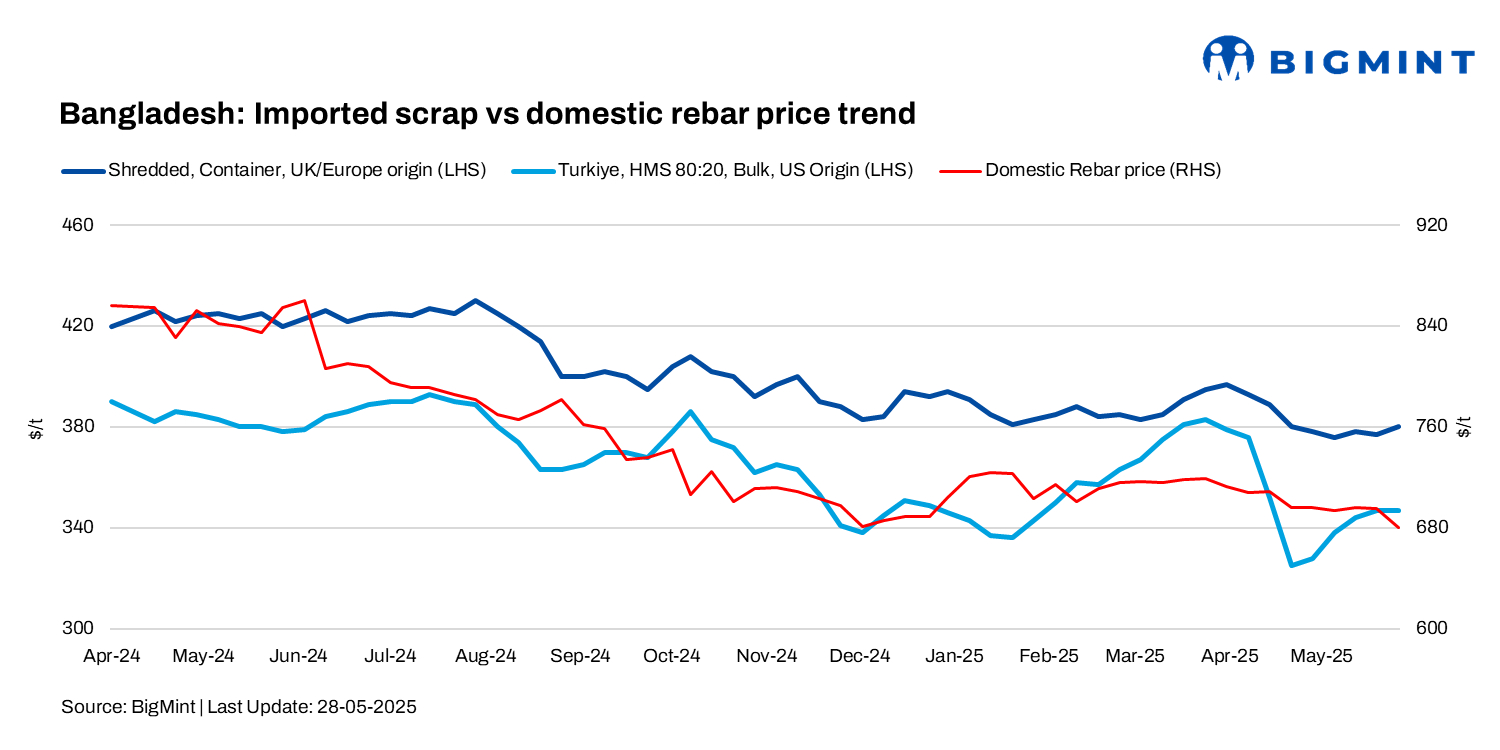

- European-origin HMS (80:20) prices inched up by $2/t w-o-w to $362/t.

- European-origin containerised shredded up by $1/t w-o-w to $378/t.

- Japanese-origin H2 bulk prices stood at $362/t CFR Chattogram, up by $2/t w-o-w

- US-sourced HMS (80:20) bulk prices stood at $376/t inched up by $3/t w-o-w.

Recent deals

- 3,000 t of PNS scrap from Singapore and Malaysia was sold at $381/t CFR Chattogram.

- 1,000 t of shredded scrap from Brazil was sold at $370/t CFR Chattogram.

- 1,000 t of PNS scrap from Singapore was earlier sold at $385/t CFR Chattogram.

- 1,000 t of shredded scrap sold at $378/t CFR Chattogram (Australia origin)

- 1,000 t of HMS 90:10 scrap sold at $362/t CFR Chattogram (Australia origin)

- 1,000 t of HMS 80:20 scrap sold at $352/t CFR Chattogram (Australia origin)

Current offer levels

- PNS scrap from Hong Kong is being offered at $395/t CFR Chattogram.

- Recent PNS offers from both Hong Kong and Singapore are in the range of $390-392/t CFR.

- Shredded scrap from Australia and New Zealand is being offered at $385/t CFR, with some recent offers from Australia at $380-382/t.

- Bulk cargo offers from the US are around $365-370/t CFR, though buyer interest is limited to around $355-360/t.

Market commentary

According to a market participant, “Freight rates from Hong Kong to Bangladesh have surged to an all-time high of $1,700/container, significantly raising the landed cost for importers. These elevated freight costs are making some otherwise viable deals unworkable, especially for high-density cargoes like PNS.”

Domestic market

While domestic scrap trades are still happening, importers are cautious due to high freights, weak steel prices, and upcoming holidays. Rebar sales continue in the local market, but only with discounts to stimulate demand. Mills in Chattogram are generally quiet, reportedly holding sufficient inventories.

Rebar prices in the domestic market have also softened significantly, falling by BDT 3,000-4,000/t since early May. Rebar that was selling at BDT 85,000-86,000/t in early May is now changing hands for BDT 82,000-83,000/t. With limited end-user demand and no new government infrastructure projects, steel consumption remains weak, pushing several mills to operate cautiously on reduced buying interest.

Bulk scrap market still inactive

Bangladesh has exhibited weak demand in the bulk market for the past six months. A sluggish economy, lack of government spending, and stalled infrastructure activity have all contributed to this inactivity. Consequently, volumes that would typically go to Bangladesh are now being redirected to India, especially from East Asia.

Outlook

With the Eid holidays approaching and the national budget announcement pending, Bangladesh’s ferrous scrap market is expected to stay quiet in the near term. Activity may pick up post June if government infrastructure spending resumes and freight markets stabilise. For now, most buyers remain on the sidelines, focusing on managing inventory.

![]()

Leave a Reply