- Vietnam’s imports surge by 35% m-o-m in Oct’25

- Exports drop 5% in Jan-Oct on weak steel demand

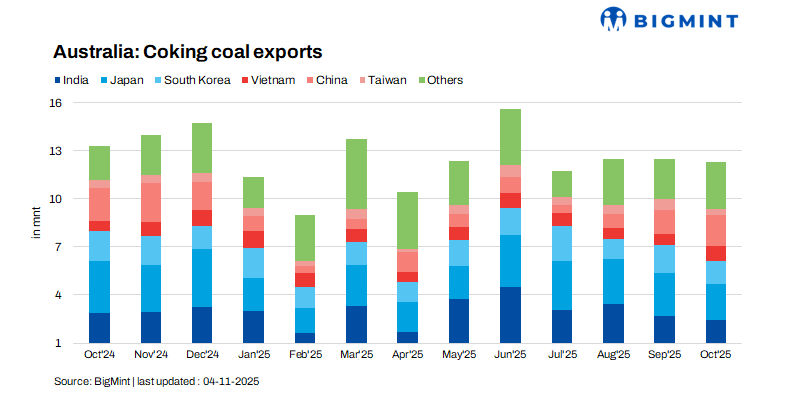

Australia’s coking coal exports remained largely stable in October, totalling 12.27 million tonnes (mnt), a marginal 1% m-o-m decline from 12.46 mnt recorded in September.

The export stability reflects a brief pause in global coal trade volatility, driven by strategic shipment adjustments and balanced supply management amid fluctuating Asian steel demand.

Cumulative exports reflect persistent weakness in steel demand

During January-October 2025, Australia’s coking coal exports totalled 121.4 mnt, down 5% from 127.6 mnt in 2024, reflecting persistent weakness in global steel demand. Cautious buying amid economic uncertainty and subdued steel output in India and Japan curbed imports, while select Southeast Asian markets maintained moderate demand on stronger production margins.

Divergent buying patterns across Asian markets

October export data revealed a clear divergence in procurement trends among major Asian importers. India’s imports fell 10% m-o-m to 2.43 mnt, constrained by declining steel output and sufficient stock levels at ports and plants. Japan’s intake also decreased by 15% to 2.27 mnt, reflecting ongoing production cuts in the steel sector amid subdued domestic demand.

Conversely, Vietnam’s imports surged 35% m-o-m to 0.93 mnt, supported by robust production levels, favourable coke margins, and increased mill utilisation rates. China, which has been a key stabilising factor in recent months, recorded a 24% m-o-m increase to 1.89 mnt in October, as stronger mill operations and rising coke margins encouraged restocking.

Meanwhile, imports from South Korea and Taiwan dropped sharply, by 47% and 16%, respectively, amid cautious purchasing and ample inventories.

The divergence underscores how varying steel output trends and profitability levels continue to shape buying behaviour across Asia.

Port-wise performance reflects mixed trade dynamics

Export activity across Australian coal terminals in October 2025 mirrored the mixed trade sentiment. Dalrymple Bay Coal Terminal (DBCT) reported a 5% rise in m-o-m shipments to 4.24 mnt, supported by stable vessel arrivals and firm Chinese demand. In contrast, Hay Point witnessed an 8% drop to 2.70 mnt, largely due to reduced loadings bound for India and Japan.

Gladstone Port exports declined 6% to 3.68 mnt, primarily reflecting weaker demand from northeast Asian buyers. However, Abbot Point registered a strong 11% increase to 1.27 mnt, attributed to improved scheduling, steady throughput, and consistent buyer engagement.

Among the smaller ports, Port Kembla saw a notable 22% m-o-m rise in shipments to 0.39 mnt, supported by metallurgical coal sales to niche Asian buyers. Meanwhile, Newcastle Port recorded no coking coal exports in October. The variation across terminals highlights the flexibility of Australian miners and port operators in realigning exports to meet shifting regional demand.

Prices edge higher on renewed buying interest

Australian coking coal prices rose by about $4/t m-o-m in October amid renewed buying from select Asian markets and tighter spot availability. Restocking by China and South Korea, supported by improved mill margins, aided the uptick, while minor port delays further tightened supply. However, sentiment remains cautious as buyers largely favoured contractual volumes over spot purchases.

Structural shifts in trade flows

The shifting pattern of Australian coking coal exports signals a structural realignment in Asian trade. With India and Japan reducing imports amid weak steel demand, Southeast Asian buyers are expanding their share through rising production and export-led growth. Steady Chinese demand continues to anchor trade flows, reinforcing Australia’s role as a reliable supplier in a volatile market.

Outlook

Australia’s coking coal outlook remains cautiously positive, with Chinese restocking supporting near-term stability. However, weak steel demand and macroeconomic headwinds may cap gains, keeping exports steady through 2025 as Australia maintains its position as a reliable global supplier.

Leave a Reply