- Expiry of anti-dumping duty pressures domestic prices

- China’s firm coking coal market supports global coke prices

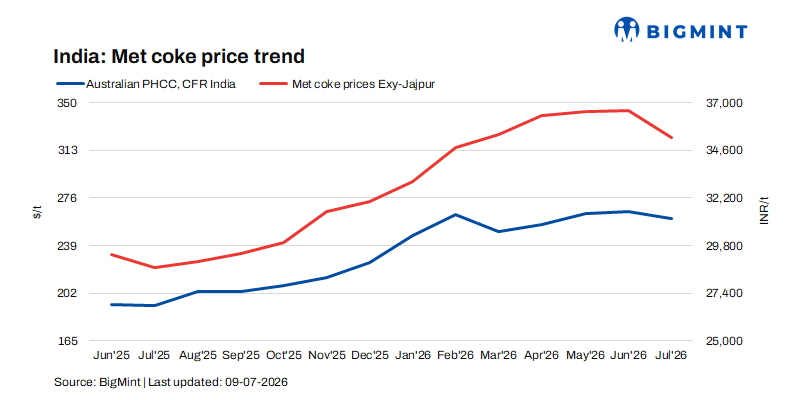

India’s domestic metallurgical coke market witnessed mixed trends during the assessment week ended 9 July 2026, with prices declining in the eastern region while remaining stable in the west. The correction was primarily driven by cautious procurement, weak spot liquidity, and uncertainty surrounding the continuation of the anti-dumping duty (ADD) on imported metallurgical coke.

A market participant noted, “The expiry of the existing duty has encouraged buyers to seek lower-priced material, including imports, resulting in increased pricing pressure, particularly in eastern India.”

BF-grade metallurgical coke prices in eastern India fell sharply by around INR 750/t w-o-w to approximately INR 35,250/t ex-Jajpur, reflecting sluggish demand and limited transactional activity. In contrast, western India remained relatively resilient, with BF-grade coke prices holding steady at around INR 34,000/t ex-Gandhidham, supported by comparatively healthier regional demand.

Foundry-grade coke prices also remained stable at nearly INR 36,400/t ex-Rajkot, aided by consistent consumption from the foundry industry.

Premium hard coking coal prices, CFR Paradip, fell by $5/t w-o-w to $258/t on 9 July 2026, reducing cost support.

Imported trade remains subdued despite firm global offers

India’s imported met coke market remained largely inactive during the week even as buyers sought low-priced material. Continued uncertainty over the government’s decision on anti-dumping duties pushed buyers to defer fresh bookings. Although international prices stayed broadly firm due to elevated coking coal costs, trading activity remained muted.

BigMint’s assessment for Indonesian-origin BF-grade metallurgical coke (65/63 CSR) edged up by $1/t w-o-w to around $319/t CFR India.

Market participants indicated that “concerns over the anti-dumping duty’s implementation continue to discourage import commitments, despite firm overseas offers.”

There is no update yet on the continuation/discontinuation of the anti-dumping duty, which was effective till the end of June. Industry sources also highlighted that imports made under India’s Advance Authorisation Scheme remain exempt from anti-dumping duties when the imported raw material is used for manufacturing export-oriented steel products, allowing eligible buyers to continue imports without additional duty burden.

China’s firm coking coal market supports global coke fundamentals

China’s coking coal and coke markets remained broadly stable w-o-w, providing continued support to international coke pricing. Tight coking coal availability, resulting from slow mine production recovery and stringent safety inspections, kept raw material prices elevated despite slower downstream procurement.

On the coke side, the successful implementation of the ninth round of coke price increases improved coking plant profitability and supported stable production levels. However, weaker steel prices, narrowing steel mill margins, and planned maintenance shutdowns are expected to reduce pig iron production and soften coke demand. Meanwhile, the proposed tenth round of coke price hikes is facing strong resistance from steel mills, indicating that negotiations between producers and consumers are likely to continue in the near term.

Pig iron prices decline amid subdued buying activity

India’s steel-grade pig iron prices in Durgapur declined by around INR 300/t w-o-w to approximately INR 37,500/t ex-works during the assessment week. The correction was primarily driven by subdued procurement from foundries and engineering industries, coupled with cautious buying sentiment and adequate material availability, which prompted suppliers to lower offers to stimulate transactions.

Outlook

India’s domestic met coke prices are expected to remain range-bound to slightly weak in the near term as cautious buying sentiment, subdued steel demand and uncertainty over the government’s anti-dumping duty decision continue to weigh on market activity.

However, the downside may remain limited due to firm international coke prices, elevated coking coal costs and constrained global supply. Clarity on the ADD policy, along with trends in Chinese coke negotiations and domestic steel production, will be key factors determining the market’s direction in the coming weeks.

Leave a Reply