- Coal inventories at ports increase by 1.6% w-o-w

- Pellet-based sponge iron prices drop w-o-w

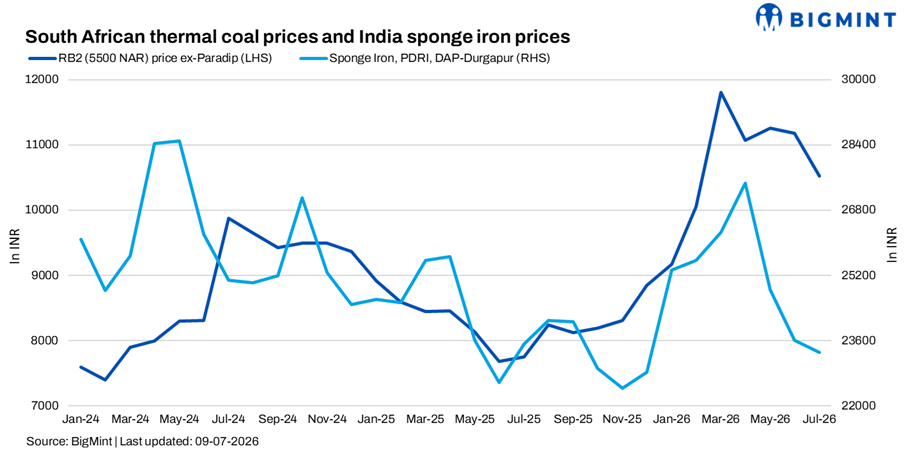

South African thermal coal prices extended their decline during the week as weak sponge iron demand, sluggish steel market activity and comfortable domestic coal availability continued to weigh on imported coal sentiment. Despite softer offers across Indian ports, buying interest remained muted, with most consumers limiting purchases to immediate requirements. Market participants reported negligible enquiries, while traders continued facing difficulty liquidating existing inventories amid limited spot demand.

As per BigMint’s assessment as on 9 July 2026, ex-Paradip RB2 (5,500 NAR) declined by INR 150/t w-o-w to INR 10,450/t, while RB3 (4,800 NAR) dropped by INR 400/t to INR 9,000/t. At Vizag, RB2 fell by INR 200/t to INR 10,250/t, while RB3 declined by INR 300/t to INR 9,000/t.

India’s thermal coal inventories at major ports increased by 1.6% w-o-w to 15.07 mnt in week 27 from 14.83 mnt in week 26. The increase was mainly driven by slower cargo offtake as consumers relied on adequate inventories and restricted purchases to immediate requirements. Regular Coal India supplies and the ongoing monsoon further reduced dependence on imported cargoes.

Softer offers fail to generate buying interest

Market participants indicated that the imported coal market remained extremely weak despite continued price corrections. Enquiries were largely absent, with only a few routine enquiries reported during the week. Several traders stated that they had temporarily stopped trading South African coal due to the lack of demand, while others avoided booking fresh cargoes as existing stocks remained difficult to liquidate.

FOB RBCT indications for 5,500 NAR coal were heard around $86-87/t, while 4,800 NAR coal was indicated at $71-73/t FOB. On a CFR India basis, 5,500 NAR coal was heard around $104-105/t, while 4,800 NAR material was offered near $85/t, supported by freight of around $17-18/t.

Spot market activity remained limited. RB3 offers were heard around INR 8,500-9,000/t ex-Mangalore, while RB2 offers ranged between INR 9,700-10,200/t across southern ports and around INR 10,800-11,000/t at Paradip, Ennore and Dhamra. One deal for around 8,000 t of RB2 was reportedly concluded at INR 10,300/t, although market participants described pricing as highly volatile on a d-o-d basis.

Domestic coal preference weakens imports

Domestic coal continued to provide the strongest competition to imported coal. BigMint assessed 5,000 GCV coal stable at INR 5,500/t, while 4,500 GCV coal remained unchanged at INR 4,050/t w-o-w. Comfortable domestic availability, regular Coal India supplies and competitive pricing continued to encourage consumers to procure domestically rather than import.

The sponge iron market weakened further during the week, with PDRI DAP-Durgapur prices declining by INR 250/t w-o-w to INR 23,250/t. Producers continued facing margin pressure, while weak finished steel demand restricted buying to immediate requirements. Although higher pellet prices supported seller sentiment, trading volumes remained subdued as buyers stayed cautious and avoided inventory build-up. Market participants noted that the weak sponge iron market continued to weigh heavily on imported coal consumption.

Outlook

Market participants expect imported South African coal demand to remain subdued throughout the monsoon season. Comfortable domestic coal availability, weak sponge iron margins and sluggish steel demand are likely to keep enquiries and fresh bookings limited. Traders indicated that a meaningful recovery is unlikely before post-monsoon, when improved steel production and sponge iron activity could revive procurement interest. Until then, buying is expected to remain strictly need-based, with sellers continuing to face pressure to clear existing inventories.

Leave a Reply