- Weak booking activity weighs on freights in key trade lanes

- Peak-season demand supports broader freight indicators

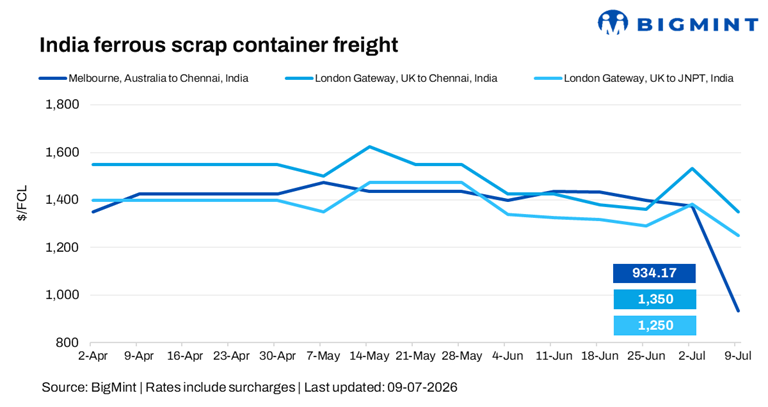

India-bound ferrous scrap container freight rates remained under pressure in the week ended 9 July. Imported ferrous scrap sentiment remained bearish as weak domestic steel demand and unfavourable import economics continued to discourage buying. Mills limited procurement to immediate requirements, while the absence of firm bids and trades reflected cautious purchasing amid poor import viability.

Australia-India scrap freight rates fell sharply this week as weaker scrap buying interest from Indian importers coincided with increased vessel availability. Softer cargo enquiries and a balanced supply of bulk carriers led to heightened competition among shipowners, resulting in lower freight rates on the route.

An Australia-based shipbroker stated, “Australian-origin scrap container freight to India and Pakistan have moved lower as subdued demand and unfavourable import economics continue to weigh on market sentiment.”

Freight rates on the UK-India trade lane remain subdued, as competitive domestic scrap prices in India have curtailed import demand, leading to lower scrap exports from the UK. Improved vessel availability and weak booking activity continue to weigh on freight levels, while carriers remain open to rate negotiations to secure cargo.

A shipbroker informed, “Compared to last week, the container freight market has softened across key trade lanes, primarily due to improved vessel space availability and weaker booking activity. Carriers have adjusted freight rates to maintain healthy vessel utilisation amid easing demand, resulting in more competitive pricing. However, rates remain vulnerable to fluctuations, with further changes likely depending on cargo demand, capacity management, and carrier pricing strategies.”

Another shipowner stated, “Current market rates remain flexible, as negotiations with carriers and freight forwarders can typically yield savings of around $50-75 per container.”

Route-wise update

Market highlights

- CFI gains w-o-w on peak-season demand: The Container Freight Index (CFI) increased by 87.23 points w-o-w to 3,326.87 points on 3 July 2026, up from 3,239.64 points on 26 June, extending its upward momentum as freight rates remained firm across major east-west trade lanes amid peak-season cargo demand, front-loading of shipments ahead of tariff deadlines, and continued capacity constraints caused by ongoing Red Sea rerouting.

- Bunker prices rise w-o-w: Bunker prices stood at $666/tonne (t) on 9 July, an increase of $6/t w-o-w supported by firmer crude oil prices and improved bunker demand across key Asian bunkering hubs. Market sentiment strengthened as stable marine fuel consumption and tighter regional fuel oil availability offset ample global supply.

Outlook

India-bound ferrous scrap container freight rates are expected to remain under pressure in the near term, as weak steel demand, competitive domestic scrap prices, and unfavorable import economics continue to curb buying interest.

While peak-season exports, higher bunker prices, and Red Sea rerouting may support global container markets, ample vessel availability and subdued booking activity are likely to keep freight rates stable to soft.

Leave a Reply